It’s fair to say that legal operations in Australia has evolved differently to the US, where businesses typically have much larger legal functions with many more lawyers in the organisation. There’s quite a sophisticated supporting structure around all of that which has effectively been brought into the legal operations umbrella. Australia is a little different.

The Corporate Legal Operations Consortium (CLOC) in Australia evolved out of a desire to bring together a group of legal staff working at some of the larger companies who had an interest in sharing things that we were learning through our operational improvement initiatives. That included technology but it also included other less tech-focused initiatives aimed at just improving our efficiency and service delivery.

CLOC, particularly in the US, also has quite an extensive array of online resources and online collaboration tools, including some active chat forums where people ask information about what’s happening, and seek insights from other CLOC members that might help them with particular problems that they’re facing or issues they need to solve. In the last year or so, CLOC has also put in place a law firm membership so that external legal service providers can share what they’re doing from an operational improvement perspective.

Sheldon Renkema, general legal manager, Wesfarmers

Legal operational enhancement can be a real challenge if you’re starting entirely from the ground up. One of the great things about CLOC is that you can very easily learn from what others are doing, so that you’re not reinventing the wheel. You are learning from others’ experiences, which makes it a really good forum for embarking on that journey, connecting with people who’ve been through similar experiences and being able to benefit from their experience of the things that have gone well or not gone well in that context.

It’s very difficult to actually objectively assess whether what legal tech providers are saying their product or service delivers is actually what it delivers. Being able to leverage the experience of people who have used those products and services to see what the actual output is helpful.

In my own in-house legal department, we were using an array of technology from the very basic, starting out at the bottom end in terms of core functionality, things like an internal matter management system, which generates data about what the team is doing and feeds into reporting on what we’re up to. We also have a document management system as well, that allows for ready storage of documents.

We’ve built a number of these tools, for example, a self-serve non-disclosure agreement tool that allows people in our businesses – without having contact with a lawyer – to be able to generate and execute a compliant confidentiality agreement. There’s also marketing review tools and a contract review tool that we’ve built and are continuing to evolve. Our objective is to identify processes that our lawyers would otherwise do that are not particularly complex and not particularly strategically significant. And where we can, making use of a tool so that can be done within the business in a user-friendly way that manages the risk.

Going forward, we are exploring the use of more sophisticated tools, particularly more advanced document review technology. The idea is to do an 80/20 review of incoming contracts so that against some key parameters that we’ve identified so that it really helps the lawyers to narrow down their focus on what’s really important in terms of those contract reviews.

We are fortunate in our business that we are relatively free to look at using technology ourselves, although there is some formality in the process. We have to ensure the software we are interested in complies with our data security frameworks, so everything needs to be reviewed by our cybersecurity team to make sure that it is compliant with our standards. The other – perhaps obvious – issue is fitting it into our budget. Aside from these issues, though, there is a fair bit of freedom for us to explore and test different offerings.

I would make the observation that lawyers increasingly need to be at least attuned to technologies and what they do. There’s an open argument as to whether lawyers need to be capable in skills like coding et cetera, my view is that this is probably not necessary but that they at least they need to be familiar with the technologies that are available, and need to be comfortable living with these.

Lawyers who are beginning their careers now are going to be looking at a very different way of practicing in 10 or 20 years’ time, and they need to be adaptable to that. Some have said that what is really important for lawyers is perhaps not so much blackletter expertise but around building empathy and their soft skills development. I think there’s certainly some wisdom in that.

Lawyers across the world like to talk about rubber stamping things, even though few who qualified in the last 15 years will have seen a rubber stamp let alone used one to certify a document. But, as we found out speaking to GCs across Asia Pacific for this special report, when a lawyer in that region talks about rubber stamping something, they often mean it literally.

‘Most documents I deal with require physically stamping,’ lamented one Indian GC. ‘Even if you want to automate some part of that process in the end you will need to get a stamp. That means a trip to another office, a taxi ride somewhere else in the city, a long wait in a queue. All to get that piece of paper stamped.’

India may be notoriously bureaucratic, but the problem was far from unique to that country. GCs from Japan, Korea, Indonesia, and even ultra-efficient Singapore told us of cultures rooted in face-to-face contact, deference to senior decision makers and established hierarchies. As a result, even that simplest of legal technologies, the electronic signature, had failed to take root.

The obstacles facing GCs who wanted to introduce technology felt unmovable. Until a pandemic hit. After nearly a year of lockdown, businesses across Asia have embraced new ways of working.

To understand just how much lawyers have adapted to tech in these strange times, GC magazine teamed up with World Services Group to survey over 100 of Asia Pacific’s leading general counsel. We asked them about everything from the impact of Covid-19 on the legal team’s efficiency to their use of AI, how they find the right software (and the money to buy it), and their expectations of outside counsel when it comes to technology.

We found evidence of a region that is almost uniformly embracing technology, a region where even the most entrenched cultural habits may be coming to an end. But let us not get carried away.

Any discussion of how GCs in the Asia Pacific region are using legal tech is liable to fall into the trap of focusing on culture first. Certainly, this special edition shows much evidence of country-specific traits that are restricting or encouraging the use of technology, but it also shows that GCs the world over are facing the same issues when it comes to technology.

Broadly, there are three steps involved in the acquisition of legal tech, all of which are things lawyers have historically struggled with: Knowing what’s out there; understanding and benchmarking the capabilities vs the cost, and convincing the business that it is going to save time and money. Until GCs get to grips with these procurement-driven approaches to buying technology their successes in finding suitable platforms is likely to remain limited.

On behalf of all of World Services Group, I am delighted to welcome you to the third edition of our GC special reports, looking at the importance and impact of technology on the legal profession.

This issue of the report is indeed a timely one, as at no point in our professional lives has the profound effect of technology been more evident. Since the onset of the pandemic, private practice and in-house counsel alike have universally transitioned to new ways of working largely driven by technology, demonstrating on one hand the adaptability of the profession, while on the other, dispelling tired notions of lawyers as technological luddites.

As the legal leaders featured throughout the report illustrate, innovation – particularly as it pertains to technology – is apparent in every corner of the profession. Just as we saw in the first two editions, neither budget nor business size need to be obstacles to innovating, with much of the counsel-driven development originating from little more than an idea and an opportunity.

Yet as we celebrate the shared successes seen across the legal industry, we must remain cognizant that innovation is a journey on which we will never reach a final destination. And with evolution emerging from every corner, it would be all too easy to rest on our collective laurels instead of continuing to build on the progress made. So, while we look on at the innovators and their accomplishments detailed throughout the report, we should also consider what we can do to foster and facilitate the emergence of the next wave of visionaries, set to take the profession further still.

Here at World Services Group, we want to embody the change that we advocate for. As an organization, we have seen that investing in technology, talent and corporate sustainability best practices that foster social and economic development are essential elements for ongoing business success – all of which represent key commitments I have made for my tenure as Chairman in 2020-21. By taking a strategic approach to our proprietary digital platform, empowering emerging leaders across our network, as well as improving training and accessibility to technology for all our membership, World Services Group is committed to ensuring that we are properly prepared to capitalize on the growing wave of technological innovation, for the benefit of both our members and clients.

In closing, I’d like to thank all of those in the legal community who contributed their thoughts and insights as part of the research for this report. By sharing your own lived experiences along this journey, I have no doubt you will help to shape and inspire the coming generation of leaders and innovators, set to once again disrupt the idea of what it means to be a lawyer.

Legal tech is becoming big business in the Asia Pacific region, so much so that the Singapore Academy of Law (SAL) has opened a legal tech accelerator. But much of the industry’s focus remains on selling to law firms. For GCs and in-house legal teams, making sense of the myriad systems can be a daunting task.

It is no surprise then that GCs would like to see law firms doing more to help them make sense of the market. While more than half of respondents to our survey (62%) said their external firms were using technology to deliver legal services, under a quarter (23%) said their firms had offered to share information on how technology might benefit their legal team’s operations.

‘Law firms need to demonstrate the value to in-house teams of adopting technological solutions’, noted one respondent, a Hong Kong-based legal manager at an international consumer goods company. ‘Right now, I think the focus of law firms is using technology to improve their bottom line rather than creating value for clients.’

Another respondent, an Indonesia-based head of legal at a large insurance provider, added: ‘It would be great if the external firm could also offer the service of helping in-house teams find the right legal tech solution for their team. They are often far more aware of the trends and services being used in the market so this would really help us understand things.’

Given the clear client demand, it is surprising that law firms are not seeing the opportunity here. Then again, law firms themselves may have a lot to learn. Just 22% of respondents were satisfied with the technology being used by their external firms.

Law firms should take this dissatisfaction seriously – 94% of respondents said it was important for law firms to keep up with new technologies, while 59% said they had started assessing their firms’ use of technology as part of their formal panel review process.

The incentive for law firms is clear. While legal tech is often seen as a disintermediator, disruptor or challenger to the established order, it does not have to be treated as a zero-sum game. As Susan Cattell, senior legal operations manager at Australian financial services company AMP, notes: ‘Clients and law firms have to work together to ensure the right tech solutions have been put into place and that they benefit both parties.’

Seemingly unable to move on from damaging #MeToo allegations; suggestions of an inappropriate drinking culture; an incomplete UK move to Bishopsgate; and a succession of high-profile departures culminating in Skadden’s poaching of Bruce Embley on the eve of Dawson’s appointment; all have contributed to keeping Freshfields in the press for the wrong reasons.

At the same time, and perhaps most important of all, there is the reputational elephant in the room: namely, the cum-ex scandal in Germany. This involves aggressive tax strategies that were championed by a former Freshfields partner so as to take advantage of apparent loopholes in German dividends tax law. (See ‘Der Freshfields-Skandal‘ for detailed analysis.)

What seems striking to outsiders is that other prominent (and respected) law firm tax departments in Germany – notably Linklaters and Hengeler Mueller – said no to their clients on these trades and refused to sign off legal opinion letters. So it seems that what Freshfields was doing was not common market practice (in other words, it cannot be said that every other law firm was doing the same, which is the usual excuse when a tax ploy proves to have been ill-conceived).

The consequences have been enormous. Firstly, it is estimated that cum-ex claims in Germany amount to €11bn (obviously, not all were signed off by Freshfields). Secondly, the Freshfields partner, along with a more junior colleague (also a partner at Freshfields), has since been arrested and faces criminal prosecution. Thirdly, Freshfields has settled a claim from the aggrieved administrators of Maple Bank (a cum-ex client of the firm that reclaimed €380m in tax that was never paid – and which has since gone bust) for €50m.

The two Freshfields partners involved have resigned. But the concern must be that there are potentially other cum-ex clients who might be minded to bring a claim against the firm, if only because German tax authorities now take such a dim view of such tactics. No doubt Freshfields has sufficient professional indemnity cover to meet claims that might be made, although it’s reasonable to suppose that partners in London (and other non-German locations) might be unhappy at having to make contributions.

Meanwhile reputational damage is already obvious – the German government has distanced itself from Freshfields and made clear it will not instruct the firm (when asked whether firms like Freshfields or others should be excluded from receiving future instructions, the German finance minister replied: ‘I cannot imagine that new assignments will be placed there’ – which is a nice way of saying they will not get any work). Might other EU governments follow its lead?

Similarly, in the corporate sector, German semiconductor manufacturer Infineon (market cap of $30bn) was forced to justify retaining Freshfields as legal counsel after one of its shareholders challenged the firm’s ethical standards. GCs we surveyed for The Legal 500 Deutschland voiced their anxiety about being ‘thrown into the same pot’ by continuing to instruct a firm associated with ethically suspect advice. And with peer firms in Germany already grumbling about the impact of the scandal on recruitment into their tax departments, how can Freshfields hope to safeguard its own longer-term position in the market?

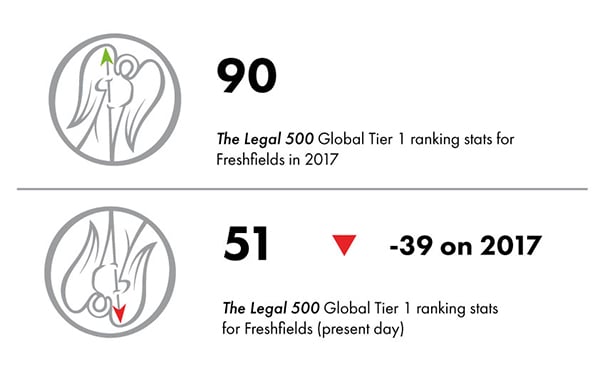

There are indications that this is not a one-year problem, and that there are more deep-seated causes for concern. At The Legal 500 it is noticeable to me that in recent years there has been a sharp decline in the number of Legal 500 top-tier recommendations globally for Freshfields (compare 90 in 2017 and 51 this year). Perhaps that is due to the firm being less open and transparent about its work, but I suspect it runs deeper than that – and it reflects less enthusiastic recommendations from clients and peers, as well as a change in the culture of the firm.

Global law firms build their practices on the basis of global expertise (which Freshfields has in abundance), but also on a global reputation. In effect, global clients want to be associated with the best and they want to be associated with legal brands that enhance their own corporate values. The danger for Freshfields is that cum-ex makes it a target of global activism (for instance, by tax-transparency campaigners in the UK) which might escalate into further bad PR. And that may then lead some major clients to question whether there are other law firm brands that they might prefer to be associated with.

That is the big unknown for Freshfields. With good fortune this will remain a localised (German) crisis. With bad luck it could turn into an international embarrassment.

The future reputation of Freshfields will be decided in the medium to long term. In the short term, I note the firm’s decline in our rankings. I note the negative comments from German GCs. I note some significant departures. I note a culture that seems to be more inward-looking and less transparent than it was a few years go. And I worry that the firm may have become over-aggressive in its pursuit of profits.

Above all else, it is client perceptions that matter. On that basis, if Freshfields was quoted stock, my buy/hold/sell recommendation would be: ‘Sell’.

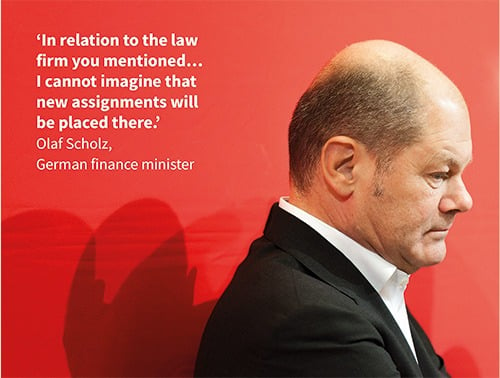

It’s 9 September in the German parliament. Stefan Liebich of the democratic socialist party, Die Linke, stands up to quiz finance minister Olaf Scholz, a member of the Social Democrat Party. His question: ‘Have there been any thoughts on your part whether firms like Freshfields or others should be excluded from receiving future instructions?’

Scholz responds: ‘In relation to the law firm you mentioned… I cannot imagine that new assignments will be placed there’.

For any normal law firm that would be a body blow. For an international firm with 27 offices in 17 jurisdictions, representing financial institutions and governments, as well as national and multinational corporations, it is a humiliation. How did the oldest international law firm in the world end up with such a public slap-down? And what prompted Scholz, one of the candidates to succeed Angela Merkel, to suggest the German government should stop instructing Freshfields?

The answer lies in the cum-ex tax fraud scheme, widely acknowledged as the biggest tax scandal in Germany’s history, in which Freshfields Bruckhaus Deringer has been identified as a major player. Since its offices were first raided in the autumn of 2017, Freshfields has been hit with a steady stream of bad press for its involvement in the scheme. In August 2019, liquidators of the now defunct Frankfurt-based lender and Freshfields client, Maple Bank, which conducted cum-ex trades, sued the firm for damages. Freshfields agreed to a €50m settlement.

Cum-Ex: What is it?

The cum-ex scandal involves a controversial dividend arbitrage trading practice, which took advantage of a loophole in German tax law. It involved banks and stockbrokers rapidly exchanging shares with (cum) and then without (ex) dividends between three parties, in a way that enabled them to hide the identity of the actual owner. At least two of these parties then claimed rebates on capital gains tax that had only been paid once. These trades were executed between 2001 and 2011, and were formally prohibited in Germany in 2012. Because of these deals, billions in tax went uncollected by the German state. Other countries beyond Germany have also been affected by the cum-ex tax fraud scheme. Across Europe, cum-ex trading is said to have cost taxpayers up to €55bn.

Reporting has largely focused on investigations surrounding the departure and subsequent arrest of partner Ulf Johannemann, the firm’s former international head of tax, in November 2019. More recently, in June 2020, another tax partner, who was the firm’s last specialist for tax products in Germany and an alleged adviser on cum-ex products, also left Freshfields and was charged with aiding and abetting serious tax evasion.

Freshfields’ direct response to the whole matter has appeared subdued. The fact that the firm created a German ethics committee, with a code of ethical principles and rules of conduct, in May 2020, perhaps was a belated acknowledgement of the need for change but was unable in practical terms to extricate the firm from the scandal.

What is clear is that the cum-ex scandal has shaken the entire tax sector and in turn inspired reflection on the professional and social responsibilities of major actors such as Freshfields. As a result, law firms’ approach to the circuitous issue of ethics now has greater impact on law firm selection decisions.

We spoke to top general counsel (GCs) in Germany to gauge their reaction: to what extent will ethical standards play a role in choosing a law firm? Should a law firm’s work be not only legally but also ethically and morally sound? Will GCs be content to work with Freshfields (and other firms) implicated in the cum-ex scandal? And what reputational damage – if any – will those firms suffer?

Legal or illegal? Moral or immoral?

Structured finance in tax law is not new, departments for tax-optimised products at financial institutions are not new and, indeed, tax arbitrage and dividend stripping is neither new nor criminal. To the frustration of tax lawyers, some falsely lump together cum-cum and cum-ex deals – two different types of dividend stripping – and most would agree that the illegality of cum-ex is not as straightforward and quite as obvious as, say, the carbon trading tax fraud (which has similarly been dubbed the ‘fraud of the century’).

Nonetheless, to many tax lawyers, cum-ex deals, which essentially involve claiming tax credit twice on taxes only paid once, simply didn’t feel right. The market quickly divided into those who gave legal opinions and those who didn’t. Freshfields positioned itself in favour of these trades and their approval was key to banks going ahead with the transactions. Importantly and – in retrospect – embarrassingly for Freshfields, two of its leading competitors, Linklaters and Hengeler Mueller, both took a more conservative approach – and did not provide the necessary legal opinions to make cum-ex deals viable. So it appears that Freshfields was the outlier – albeit in a highly profitable sector of the tax market.

Looking back, tax lawyers agree that attitudes to tax avoidance have changed since the 2007/08 financial crash. Advice on tax reduction was previously very much the primary focus for many tax departments, and aggressive tax planning was not out of the norm. While this may still be the case for some, the cum-ex scandal has no doubt contributed towards a shift in attitudes. These days, the new key theme is risk minimisation. Clients’ appetite for risk has decreased dramatically and, as one tax partner at a large international firm points out, there are now even sustainability reports in tax law. Today, there is a completely different kind of awareness than there was ten years ago – and that new approach goes hand in hand with a call for transparency.

One might still argue that the tax adviser’s job is to assist the client with paying only those taxes that are required, and the point of tax advice is to arrange fiscal relations in order to pay the least taxes necessary. At the same time, however, as a GC and managing director at a major software company points out: ‘As an independent body responsible for the administration of justice, the lawyer also has obligations to society that exclude representing unethical practices’. While this latter commitment might have limitations, for instance in relation to representation in criminal proceedings, the ethical component of legal advice is actively influencing companies‘ choice of law firm.

Traditionally, ethics and law go hand in hand. Law firm partners should have an innate moral compass. On that basis no distinction should be necessary between legally sound and morally or ethically justifiable advice, and for corporate counsel this distinction should not play a role either when mandating a firm. Ethics committees and supervisors should therefore – in theory – be superfluous. But that traditional approach is now seen as old-fashioned and incompatible with some aggressive profit-driven clients demanding aggressive profit-driven solutions. The danger for any law firm is that it is obliged to adopt the moral compass of its important (high-profit) clients and place money-making over traditional ethics. That is a problem that faces all major firms, not just Freshfields, although it is Freshfields that is providing a case study in how high-profit work can come at a reputational cost.

What is significant from our conversations with German corporate counsel is the indication that client prerequisites are changing. While ethics were ‘taken for granted as an unwritten law’ (in the words of the GC at a major German manufacturer), that is seemingly going to change, with a greater expectation on firms to take responsibility for clear ethical policies and positions.

Today, nobody would deny that the cum-ex scheme is a crime against the taxpayer, so how is it that some tax lawyers and some firms – not just Freshfields – committed to approving these deals? Several GCs have commented on corporate law firm culture and what they perceive to be changes in law firm behaviour: ‘These institutions change people’, according to the head of legal at a multinational financial services company, adding that they believe there is ‘an attitude that everything which is not legally prohibited is allowed.’

‘Two rotten apples discredit the entire firm’

So, who should take the blame for overstepping ethical boundaries and getting involved in what later transpired to be a huge tax evasion scheme at the taxpayers’ expense? From the GCs’ point of view, some maintain that the focus should remain on individual lawyers or, at most, specific legal teams.

Possible misconduct by individuals does not automatically mean misconduct by everyone else. But the cum-ex scandal has shown that an individual’s actions may lead not only to that individual’s reputation being damaged but that of an entire department will likely suffer as well. By extension it is entirely feasible that repercussions could end up being firm-wide. As a senior regional counsel at a medical technology company puts it: ‘Two rotten apples discredit the entire law firm… the behaviour of individual representatives of a law firm suggests the approval of unethical behaviour by other colleagues.’

Whether flawed culture has afflicted Freshfields is uncertain, but the danger for the firm is one of perception: whether those two malefactors are seen (fairly or unfairly) to indicate a deeper-seated problem in the larger organisation. At the very least, the crisis poses questions over internal checks and balances. The GC at a US retail company makes a blunt assessment: ‘The firm’s role in the scandal must be made clear and there needs to be a statement about the firm’s values, to which it will adhere in the future.’ Freshfields’ May 2020 code of ethical practice might have sought to answer the second part of this, but the risk for the firm is that it is seen as no more than a belated PR exercise to try to distance itself from the ongoing bad publicity without directly confronting the part it played in cum-ex matters.

Conversations with German GCs show that specific individuals’ or departments’ involvement in unethical behaviour is the most relevant factor. However, when it comes to securing new business, the focus is on the entire law firm.

Beyond not wanting to be associated with questionable ethics, some corporate counsel already go one step further and consider themselves to be ethical guides whose job is to set out the right path not solely on a legal level. One respondent, in their role as in-house counsel at a German consumer electronics company, sees themself ‘as a kind of moral compass for the company’. As such, mandating a firm involved in the cum-ex scandal goes against the grain.

‘Legally clean work is no longer enough today,’ they comment. Instead law firms are subjected to a holistic analysis by legal departments, and this in turn means ethics and morality are increasingly and more explicitly incorporated into corporate decision-making processes. If firms do not meet ethical standards, this may be reason enough not to mandate them. This is where reputational damage potentially has a snowball effect. Corporate counsel will be reluctant to be seen as approving of seemingly unethical behaviour. As a GC at a food services conglomerate states: ‘If some clients avoid the firm, remaining clients could feel they have been thrown into the same pot morally.’ In short, clients end up needing to justify mandating a firm whose ethics have already come under question and whose reputation has already taken a hit.

Freshfields has already come close to this scenario. In February, the giant German semiconductor manufacturer Infineon (market cap of $30bn+) was forced to justify retaining the firm as legal counsel after one of its shareholders challenged the decision’s ethical standards. ‘The board of directors instructed the law firm Freshfields, which is said to be responsible for what is probably the biggest tax robbery in post-war history,’ stated the shareholder, pointing to a violation of Infineon’s code of ethics and its code of business conduct.

Fairly or not, that is the context in which finance minister Scholz indicated that the German government should no longer instruct Freshfields. If the German government will not instruct the firm, then the pressure on GCs (German and non-German) not to appoint it may be ratcheted up another notch. The obvious danger for Freshfields with state intervention of this kind is that a local problem becomes a global problem – and that the governments of other countries decide that they should distance themselves from the firm.

The resounding message from clients is that any firm involved in an alleged scandal should not simply keep quiet. Instead, the firm should openly address and deal with its behaviour. As a first step, a firm should ‘fully clarify [the involvement in the scandal] and, if necessary, distance itself from unethical individuals’, says a senior regional counsel at a medical technology company.

A director of legal operations at a multinational pharmaceutical company agrees: ‘What matters to us is that law firms deal transparently and consistently with the issue.’ This includes ‘open communication and consequences of possible participation’. They point towards the need for documentation of measures that are being taken to prevent such a situation from arising again, sustainable instruments for monitoring and control, as well as training.

On top of that, they call for ‘a very clear statement from the firm’s management on the ethical principles to which the employees are obliged’. The Infineon example illustrates the dangers for firms not perceived to have taken up a proactive commitment to ethical standards, where that commitment has often already been taken by the client itself.

Indeed, some GCs report that they already include ‘ethical standards and values’ in their assessment when selecting preferred legal advisers, and law firms are increasingly measured against codes of conduct. This also reflects the larger trend within corporate companies, and the same is now expected of their business partners, including their legal advisers.

An existential threat?

No doubt, the consequences of being involved in the cum-ex scandal are existentially threatening for some individual financial, and also some legal advisers in Freshfields and other law firms (Freshfields was not the only law firm implicated in the global cum-ex market).

But it goes beyond the individual. As the cum-ex tax fraud scheme has engulfed law firms across Europe, departments and firms as a whole may need to delve deeper, openly evaluate the ethical aspects of their own practices and put new measures in place that reflect today’s call for transparency, accountability and ethical standards.

The results of our informal survey of German GCs showed that 88% agreed that firms involved in the scandal would suffer reputational consequences, and the same percentage claimed to take ethics into consideration when selecting a firm. Less than a third claimed to be content to work with implicated firms.

For months, Freshfields took little obvious public responsibility for its cum-ex advice. Only in late February did the firm for the first time issue a self-critical statement, when managing partner Stephan Eilers spoke with the German weekly newspaper Die Zeit. Previously, the firm’s official line focused entirely on the legality of its advice with no comment on the criminal legal proceedings against its partners or the damage claim settlements over its advice to the now defunct Maple Bank.

In a tentative change in communications, Eilers acknowledged that its advice in the context of cum-ex deals is not a glorious chapter in the firm’s history. The timing of this first open recognition of reputational damage strongly suggests it was spurred by the Infineon incident: it shortly followed Infineon’s AGM, where the Freshfields client was forced to justify using the firm.

Only a few months later, in May, Freshfields recognised the need to address its ethical standards by establishing an ethics committee and publishing its code of ethical principles and rules of conduct. But by then much harm had already been done. The clear message from some German GCs is that they still feel they are waiting for clarification from Freshfields on the role the firm played in cum-ex advice. Instead, Freshfields has become known for a wall of silence.

‘What matters to us is that law firms deal transparently and consistently with this issue.’

What will the firm do next? One suggestion from the reputational-damage casebook might be to appoint a credible outsider to conduct an independent review, which would then be published. That might go a long way to reassuring clients that the firm retains its moral and ethical compass. The model might be the searingly honest review commissioned by house-builder Persimmon in 2019 (which confronted the issue of whether high earnings had come at an unacceptable cost). There is no historical precedent for a Magic Circle firm doing that; Freshfields had no comment in response to this suggestion being put to them.

GCs report that relationships with firms allegedly involved in the scandal are likely to come under increased scrutiny, although relationships would not be immediately terminated. However, when it comes to new instructions, alleged involvement in cum-ex deals is seen as much more likely to rule out a firm from selection.

In short, existing relationships may – for now – continue, albeit harmed, while new relationships have unquestionably been jeopardised: ‘I consider it impossible to instruct law firms known for such practices,’ says one GC. ‘Freshfields Bruckhaus Deringer will suffer reputational damage for a long time due to Ulf Johannemann’s advice,’ states another.

There is also an expectation that there will be more accused parties, more proceedings and more who will suffer the consequences. When speaking to tax lawyers at firms and to their clients there is certainly the sense that the entire sector has suffered a blow.

For Freshfields’ new leadership team of senior partner Georgia Dawson and the three joint replacements for Eilers – Rafique Bachour, Alan Mason and Rick van Aerssen – these problems are first-hand and real. The firm’s reputation has been trashed in Germany in a way that would have been inconceivable a few years ago. There may be other global issues to contend with, ranging from the strategic (can the firm establish itself in the US and what additional pressures do those efforts place on the already brittle lockstep pay structure?) to a series of significant departures (notably that of M&A co-head Bruce Embley to Skadden, Arps, Slate, Meagher & Flom on the eve of Dawson’s election). However, those may yet pale into insignificance compared to the potential damage to the firm’s standing caused by the cum-ex scandal. Ultimately a Magic Circle law firm trades on its reputation – damage that, and you can end-up damaging the whole firm.

Stop press

At the end of January it was reported that Freshfields had made a voluntary payment of €10m to the Frankfurt Public Prosecutor’s Office (PPO), and that the PPO no longer pursuing the firm as a concerned party in connection with Maple Bank. Freshfields said that the move followed “constructive dialogue” with the PPO and had not admitted guilt and/or liability. While Freshfields’ hope will be that a line can be drawn underneath the affair, their efforts to move on seem unlikely to be helped by the cum-ex scandal rumbling on in Germany and beyond (with Danish prosecutors now investigating and charging traders with tax fraud). Cum-ex long since moved from dramatic incident to long-running saga, and the consequent fundamental problem for Freshfields seems likely to be one of long-term reputation, heavily damaged by association with the largest tax scandal in modern European history and unanswered questions over how the firm allowed itself to be implicated in the first place. €10m will not buy back that reputational damage.

Research: Anna Bauböck, Editor of The Legal 500 Deutschland.

Commentary: John Pritchard.

All interviews with German GCs and corporate clients were carried out in September 2020.

At the best of times, the role of the in-house counsel is marked by loosely defined and ever-expanding boundaries. It is part of why the role demands a sufficiently flexible and open-minded candidate in order to be done effectively.

Enter COVID-19: norms of business and the global economy have been thrown into turmoil as countries across the world struggle to balance the need to control the flow of the pandemic with economic survival.

As of the start of August, four of the top ten countries for confirmed cases of coronavirus are Latin American. Businesses working in the region will be as pressed as businesses anywhere to weather the storm, adjust their practices and adapt to whatever world in which they find themselves operating after the peak of the pandemic has passed.

How do in-house counsel across Latin America feel about the effects of the pandemic? What have their experiences been? How do approaches differ between counsel and across businesses?

In The Legal 500’s GC Powerlist: Latin America Survey, we asked counsel working in the region all of these questions and more.

Status Report

While the pandemic hasn’t exactly affected all countries equally, most of the in-house counsel surveyed for this report could agree that it had affected their work, and that of their legal team.

46% of respondents felt that the COVID-19 pandemic had affected the output of the legal team to at least a moderate degree, with 20% feeling that the impact had been ‘great’. The single largest group were those who felt that the pandemic had ‘slightly’ impacted their legal team’s output, at 37%.

All but a small number of in-house counsel working in their country’s defense sector reported that them and their teams had been working from home during the pandemic.

“Communication was repeatedly emphasized in the interviews conducted with general counsel from across the region as being of particular importance in adjusting to entire workforces being taken off-site.”

‘I think everyone would agree that working from home under these circumstances would be ideal,’ said one GC working for an aviation and defense contractor within the region.

‘But for us, it is not permissible. We are working with documents and files that are highly sensitive, and that cannot be risked in remote working. Many of our employees are given a special government pass to be commuting during the pandemic.’

The majority of respondents (76%) felt that home-working had been ‘highly’ effective, and another 20% characterized home-working as having been ‘somewhat’ effective. The rest felt it was too difficult to say; not a single respondent reported feeling that home-working had been less than effective.

Measuring success remotely

This data begs the question: how can the effectiveness of home-working be properly gauged?

It’s a question which takes on added import among the speculation that this period of remote working will extend beyond the pandemic if not become the norm entirely. Despite virtually all respondents reporting their team working from home since the start of the pandemic, just over half (58%) said that they had been monitoring the effectiveness of homeworking for their employees.

For many, the proof is in the pudding:

‘We manage to complete integration projects and M&A initiatives in a record time,’ says Alejandra Castro, head of legal at Bayer, based in Costa Rica.

‘The feedback of the business is that the team is not only very responsive but also very involved in every company’s decisions. Home office has increased the overload of work in the organization but we have manage to keep performance on track.’

But the work doesn’t always speak for itself, particularly when the benefits brought by having a competent legal team are often difficult to quantify. In these instances, broader brush strokes are required when attempting to track how the team is coping under pandemic pressure.

‘We have shifted to goal based work, improved communication and knowledge sharing practices across the regional legal team, keep each other updated on target completion and adopted legal project management practices to keep everything on track,’ says Jorge Hirmas, general counsel at Orica.

Communication was repeatedly emphasized in survey responses and the interviews conducted with general counsel from across the region as being of particular importance in adjusting to entire workforces being taken off-site.

Ana Haynes, general counsel at Essilor in Brazil, said that they monitor home-working ‘through video calls, through the delivery of many work demands, through constant feedback and phone and video interactions, as well as surveys performed by our company.’

Sheila La Serna, Chief Legal at Profuturo, shares her organisation’s approach amongst the pandemic in Peru: ‘From the outset of the Sanitary Emergency Declaration and Social Isolation declared by the Government of Peru, we conducted daily videoconference meetings first to assess how the team was keeping up with their current home office situation, what needs they had (i.e. accesibility to our systems or physical attendance to the office, and health status) and furthermore, set a schedule considering housekeeping and child care hours since the majority of our members in the legal department arewomen.’

‘Also, the CEO and senior management shared with the teams some podcasts with updates con health monitoring, challenges and quick wins during the COVID-pandemic. From June 2020 on, we had a twist for good knowing that “no size fits all”: we agreed on having virtual sessions twice a week only,to review how we started and finished the week, but we kept communicating one -on -one by Whatsapp (legal department chat and individual chats), email and mobile when necessary.

‘After that, the team´s motivation rose because they felt they had more flexible time to spend with their families,and I saw a change on our productivity measured by quicker responses made and greater number of emails that were replied during the day.’

One common sentiment was that there has been a realization (or validation, in many cases) that employees are just as effective when working from home, particularly when properly supported by the organization.

‘[We have] follow up conference calls and meetings,’ says Catalina Gaviria, legal vice president at SBS Seguros in Colombie.

‘Nonetheless, we are confident that our team is composed of great people who are very professional and committed to the result of the company! Therefore, more than conducting follow up meetings to tasks (which we do), during these times is always important to keep a warm contact. We usually use video to see each other, we ask daily how we are, talk about our personal and family concerns. We even celebrate special dates as happy birthdays of the team, by sending food and celebrating!We are convinced that a happy team always provide great results and are always effective, open, and available.’

Mental health

The COVID-19 pandemic comes at a time where an increasing amount of attention is being paid to health and wellbeing at work. The legal profession is in many parts of the world associated with long hours and high pressure, and despite a prevalent myth that these concerns do not exist in-house, general counsel must be careful to ensure they and the teams they lead are taking care of themselves.

Just under half (49%) of all respondents to the survey sent out as a part of this report felt that in-house counsel have appropriate resources available to them in order to assist with stress or mental health issues, and 37% answering in the negative.A little over half (54%) of respondents reported that their organization has an employee mental health policy.

Of those who reported their organization having such a policy, the most commonly cited feature of the policy in use was the specification of a chain of command or point of contact for support. The second-most commonly cited feature was flexible working arrangements.

“Just under half (49%) of all respondents to the survey sent out as a part of this report felt that in-house counsel have appropriate resources available to them in order to assist with stress or mental health issues.”

When asked to identify the leading causes of mental health problems for in-house counsel, the most commonly given answer was the high stress nature of the job (68%), followed by long hours (57%).

Now, thanks to COVID-19, the workforce is remote, which means the line at which work ends and recreation begins is even more difficult to manage. This was a concern expressed by many participants in this research, but just as common was a feeling that the pandemic has given teams the opportunity to explore how to keep their motivation and mental well being high.

‘We have been in constant communication with team members within my region, and also with the rest of the members of the Law Function within Cargill across the globe,’ explains Michelle Canelo, legal director at Cargill in Honduras.

‘We have been monitoring feedback we receive, how are people feeling, dealing with the challenges that came with Covid-19, not only work related, but with new challenges from home with family. being mindful of the needs of our team members, providing them with resources, accessories that could make their job at home more easily, for example, coordinating that team members received the chair, their docking station, monitors, files needed, printers, headphones, etc from office and deliver to their homes, so that they can work better and take care better of their posture, their overall health.

‘We’ve been also talking about mental health and how we can support each other, listening, talking of our challenges, etc.we even had happy hour every month, getting together virtually at the end of the day, and sharing, a cup of coffee, a glass of wine or other, and a good non-work related conversation.’

Lasting change

For the in-house community, the upheaval of 2020 has manifested in a variety of ways.

The practically universal uptake of home-working for the duration of the pandemic is an easy example. But the in-house counsel surveyed also pointed to other areas that have seen change.

For example, respondents largely reported being more likely to renegotiate obligations with business partners as a result of the pandemic: 71% said they would be more likely, as opposed to 16% who said they would not; the rest were undecided.

45% of those surveyed said that they expect the way in which external firms will deliver their services to change as a result of the pandemic, compared to just 26% who did not expect any such change; the remainder were undecided.

‘I expect external law firms to be more proactive, more efficient, more agile and for their business understanding to improve,’ says Ricardo Estrada, senior lawyer for the wider Latin America region at GlaxoSmithKline.

‘I also think they need to be open to provide support 24/7 and to team with other external law firms and forget about how to compete with them, rather [focus on] how to team up for work.’

‘We are already living a change,’ emphasizes Sheila La Serna at Profuturo.

‘Most of the firms we work with have acknowledged the importance of adding value to in-house teams during COVID pandemic. Webinars, live or recorded and podcasts with legal content are now trends in many firms to keep clients engaged.

‘Delivery is definitely quicker and it is expected to continue that way.Legal service will not disappear in the near future but I think that digitalization of the services, blockchain and artificial intelligence will challenge traditional law firm service sooner or later.’

As for homeworking, counsel were almost united in their expectations going forward: 77% said they expected homeworking to become more frequent, and another 17% said they expected it to become the norm. Just 2% said they expected the pre-COVID status quo to persist.

Some readers may know that González Calvillo has uninterruptedly partnered with The Legal 500 in sponsoring the Private Practice Powerlist: US-Mexico for several years. Looking back, each of the issues from 2017 onwards contained widely distinct business messages from our firm, ranging from record-breaking transactional work and law firm profits on 2017, to the forced adaptation of the Mexican economy to geopolitical changes in 2018, and finally the stagnation of our economy in 2019 due to a series of erratic decisions by President Andres Manuel Lopez Obrador and his administration. Market uncertainty and increasing concerns for investors were well underway at the outset of 2020. But cliché as it may be, nothing could have prepared anyone for what was about to happen this year.

Here we are, then, in the midst of 2020, facing what is now clearly the most severe global economic debacle since the Great Depression, let alone the vast human tragedy. By the time we write these words, we already know Mexico will not fare well from COVID-19. While developed countries across Asia, Europe and North America have already installed rescue and recovery plans of inconceivable dimensions -mostly aimed at saving small business who are primary sources of employment-, our government has opted to stay stale, basically. Experts have already pointed to the potential loss of Mexico’s investment grade by 2021, likely depending on the results of the midterm legislative elections coming next summer.

So where does this leave us lawyers besides working from home during many months? Well, this depends on whether one sees the glass half full or half empty.Truth be told, our profession has been and continues to be one of sustained privilege; most of us have been able to continue serving our clients and attending each of our affairs without serious interruption and mostly seamlessly. All from the safety of our homes.

All of a sudden, a hefty chunk of clients to law firms were forced to alter their strategies, radically. The legal industry had to adapt swiftly to new needs; the experience accumulated in years of deal-making had to be abruptly applied to helping longstanding clients, with many of whom we have developed close friendships, survive. Those firms lucky enough to have invested in insolvency litigation and restructuring are now beyond busy. Sadly, expectations are that there will be an incalculable number of bankruptcies in Mexico as a consequence of the virus, exponentiated by the lack of robust economic assistance directives and support by the current administration.

But not all is lost. In addition to insolvency work, we are proactive witnesses of the notable uptick in revenue stemming from our technology practice group. Big-Tech companies, led by GAFAM, have evidenced that the world is accelerating towards technological solutions in most if not all of the components of our daily lives; the NASDAQ index is trading at all-time highs while fintech and ‘app’ companies are showing no signs of deceleration. Who had heard about Zoom just a few months ago? This appears to be welcome news for fund formation, private equity and M&A generally. Even during the pandemic, there have been substantial transactions announced between traditional banking institutions and technology companies, unimaginable just a few years back. Most of these deals imply considerable regulatory hurdles, so law firms carrying demonstrable sophistication and experience in banking, securities, pension funds and insurance are likely to be involved to sort these obstacles. Given the size of some of these deals and the potential competitive overlapping effects that they may have on the relevant markets, antitrust counsel to help navigate these challenges becomes critical.

It seems humanity is not likely to disappear as a consequence of this sad episode. If we concede to this premise, then we can safely assume that demand will pick up on homes, schools, and entertaining generally; leisure travel is already on the rise. In addition, valuations on infrastructure assets have been impacted in ways that can hardly be described. Those investors with longer horizon expectations are probably pleased to detect business opportunities in this jurisdiction that had not been available in decades. This is where solid real estate and hospitality legal teams can and should be tapped. We are especially optimistic on tourism prospects, where substantial investment has been made in our country and, with some long-term tweaks perhaps, it will be back stronger than ever. All of these enterprises typically come paired with strict ESG principles so expert advisors on these issues are additive to transaction outcomes.

We are optimistic, then, as we have been since our firm was founded. We may be working from home and may have had to learn a few tricks to safeguard full team communication and 24/7 availability, but interestingly we have had a chance to share more of our personal side with our team members, both colleagues and co-workers, and make it less a mechanical machine and more a human organization. We have learned and gained from each other in ways we never thought possible. We hope this ultimately derives in enhanced working experiences with our clients, to whom we are devoted.

It is not news that the role of in-house counsel has become increasingly demanding and complex. The flip side to that is that the in-house counsel role has become even more strategic, challenging and stimulating than it was 5 or 10 years ago.

We live in a world which is much more regulated than it was a few years ago, which moves and reacts at a much faster pace than before, in a world where the risks (legal, reputational and others) that general counsel has to help manage, mitigate and protect from are several and diverse in nature.

Below, in summarized form, is an attempt to describe some of the most relevant themes sitting atop of the agenda of general counsel across the country.

Data privacy and cybersecurity issues

The Brazilian GDPR, or LGPD, will soon come into force. At the time of writing, the Brazilian Congress is still debating whether to bring LGPD into force on August 2020 or postpone its enactment to May 2021.

In any event this is a concrete fact in the horizon of all businesses and their legal departments. To the extent these businesses are subsidiaries of companies subject to European or US data protection laws less adaption to comply with local regulations will be required, but at the very least some compliance effort will be necessary.

Beyond LGPD, cybersecurity and electronic fraud in general are increasingly seen as by in-house legal teams, which are called upon to deal with all aspects and repercussions of security breaches of companies’ electronic systems, from a data privacy, consumer and/or criminal law perspective.

Fake news

When we hear the expression ‘fake news’ we usually think of it purely in the political context. The truth is that a number of professionals and business are attacked by producers of fake news everyday with an aim to harm their reputation and gain undue market advantage for competing businesses. In Brazil this huge new problem is compounded by the additional difficulty that the crimes of slander, libel etc and their penalties were designed for a time when fake news would spread by analog means, and thus the potential of harm was smaller. Currently there is a bill of law dealing specifically with the issue of fake news being analyzed by Brazilian Congress and the Brazilian Supreme Court is conducting an investigation on the subject.

Tax Reform

With the Brazilian Federal Government and Congress refocusing on the legislative reform after being sidetracked by COVID-19, the first item on the agenda is the Tax Reform. Each of the Federal Government and Congress have proposed and are supporting different bills of law addressing the tax reform. Until this situation is resolved and a common project negotiated it is unclear if, when and how the reform will shape up.

The new tax rules will be a challenge for everyone until fully understood by market agents and interpreted by the administrative and judicial courts. Some of the changes being potentially contemplated are substantial and can have a significant impact on businesses. The legal and business community are paying close attention to the matter and lobbying for the positions they advocate. The Tax Reform will keep both in-house and external counsel busy for quite a while, before and after the approval of the new rules.

Restructuring

Another challenge/opportunity for in-house counsel is the current situation of financial distress for many businesses provoked by the COVID-19 pandemic. This should allow for exposure on the renegotiation of the company’s debts, and sometimes in the Brazilian processes of Recuperação Extra-Judicial and Recuperação Judicial (respectfully pre-packaged reorganization and court-supervised reorganization), hopefully negotiating with the creditors and approving it with the court, as the case may be, the restructuring plan for the company. Conversely, when in-house counsel is employed by a business that is capitalized and seeking acquisitions/consolidation or debt acquisition opportunities, in-house counsel can exercise their legal creativity to the maximum.

We expect the next couple of years to present plenty of these opportunities, which we know come at a heavy cost for many in-house counsel because it generates the pressure to lay-off part of the team, the fear to lose one’s job and all the mental distress that comes with these situations.

Anticorruption

Since the enactment of the Brazilian anticorruption law in 2013 and the beginning of Operation Car Wash, anticorruption compliance and prevention has been at the forefront of the agenda of most businesses and legal departments in Brazil. This is a trend which came to stay and became part of the day to day of in-house counsel, sometimes adding people to the general counsel’s team and more often simply adding regulatory complexity and responsibility in cases where organizational structures do not provide for a separate integrity/anticorruption function lead by another professional.

The state of ESG (environment, sustainability, governance) in Brazil

The discussion around ESG is still in its very early stages in Brazil, certainly less advanced than in the US or Europe. Nevertheless, after the latest annual letter to investors from the CEO of BlackRock and the endorsements that ESG policies have received by a representative group of CEOs of a number of S&P 500 companies, the finance and business world may be coming to realize the size of the environmental threat not only to our health and planet but also to the economy.

When one recognizes the pressure being exercised on the Brazilian Government in light of the illegal burning and deforestation that is taking place in the Amazon, and the strong reaction of world leaders and private investors – both foreign and domestic – it becomes clear that the environment and sustainable practices, together with good governance, are a much bigger concern than ever before for businesses, their customers and, consequently, the general counsel and her team.

Privatizations, concessions and the new role of the BNDES

Another interesting development we are observing stems from the new role attributed to the National Economic and Social Development Bank – BNDES by finance minister Paulo Guedes.

BNDES in the past would finance, through debt and equity instruments, a huge portion of all infrastructure build-out in Brazil plus virtually all its large corporates. This has changed and BNDES is rapidly divesting of various equity stakes it held in publicly-held companies, state owned or not. The most recent example was a block trade of Vale’s shares for R$8.1bn (approximately US$1.5bn) on 4 August 2020, arguably the largest block trade in Latin America’s history.

Additionally, BNDES is in charge of executing the Federal Government’s privatization program and assists, whenever called upon, Brazilian States and Municipalities with their own privatization, concession and PPPs programs. This is an interesting development which provides in-house and outside counsel alike with ample opportunities.

Similarly, PETROBRAS continues to divest from a number of assets, providing for opportunities both on the acquisition and potential buyers’ finance sides.

New and not so new preoccupations of general counsel

Given the increased pressure to deliver more with less resources, general counsel in Brazil have embraced innovation in general, and technology in particular, from within their own company and also from their vendors, be it a law firm, a legal service provider, a Big Four or a lawtech. Competition has never been so intense, but at the same time there are more opportunities to innovate and create new needs that clients did not know they had.

Diversity is another big item on most general counsel’s agenda. Nothing new, obviously, but relevant, especially in an environment where not only women face challenges, but where the LGBTI+, the black and mulato and purely economically disadvantaged populations are given much less opportunity. It is important to acknowledge that the largest companies and law firms have made good progress in the last few years, which is encouraging. However, there is still a lot to be done.

Two other topics frequently mentioned by general counsels are (i) mental wellness related issues in their companies, in their teams and in the profession, and (ii) pro bono legal work. General counsel are trying a number of measures to keep their people happy and healthy at work and this seems to be a fairly high priority for many of them.

Pro bono became more widespread in Brazil in the last decade and many of the more sophisticated firms run more or less structured pro bono programs. Interestingly, very few general counsel based in Brazil seem to take this into consideration in their hiring decisions compared to their foreign counterparts. We expect this to change and to become more important to them going forward. We certainly hope so as it would be a movement in the right direction.

The changing needs of in-house counsel and the challenges they face inside the company

This article would be incomplete without mentioning the current needs of general counsel and their teams in the challenges they face daily in delivering to their internal clients and other stakeholders of their businesses.

We continue to hear that law firms still tend to think more about what is good for them instead of for their clients. We continue to hear that law firms do not listen, do not innovate and do not engage in true dialogue with their clients as to what their needs are and how they can collaborate together. Conversely and to be fair, we sometimes hear the same speech from managing partners of other firms: that the majority of general counsel do not engage in true dialogue with their firms as to what their needs are and how they can collaborate together.

It seems that someone ought to take the initiative of this conversation. Considering that law firms are the service providers in this relationship and usually well paid to deliver solutions, we are of the opinion that law firms should overcome their old ways and their fear to get in front of the client somewhat vulnerably because they will not have all the answers, venture out of their comfort zone and take the first step. Whoever does that earnestly, consistently and diligently has a much higher chance of success at developing a closer and more meaningful relationship with its clients.

*The author would like to acknowledge the contributions made to this article by his partners, for which he is very grateful.

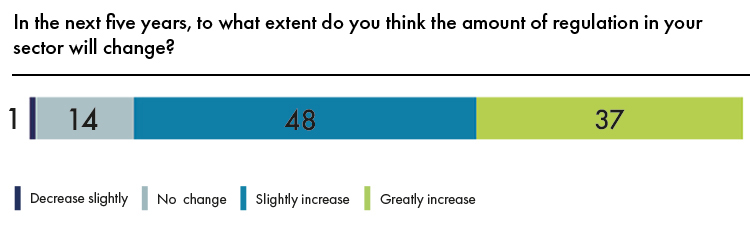

Regulation is taking over the agenda for in-house counsel across Latin America, according to the results of the 2020 GC Powerlist Survey: Latin America. Almost 70% of respondents reported that the sector in which they are operated is highly regulated – 92% said that their sector was at least moderately regulated.

What’s more, 85% of all respondents said that they expect regulation in their sector to increase in the next five years, with almost half of that number (37% of all respondents) expecting a great increase in regulation. Virtually no respondents expected regulation to decrease in the next five years, and just 14% expected no change at all.

‘The explosives industry is highly regulated and for very good reasons,’ says Jorge Hirmas, general counsel for the Americas at Orica.

‘The regulations in the different countries of the region are similar and of a high standard.Some important aspects of our industry regulations and the means of implementing them could be improved, however, in most countries there are plans currently underway to address these gaps.’

The numbers reveal a complicated relationship between in-house counsel, their businesses and the regulations that are governing their conduct. Taken as a whole, the in-house counsel that participated in the survey were cold on the prospect of more regulation in their sector: 42% said that they thought more regulation in their sector would be a bad thing, compares to 23% who thought it would be positive. Those who came from highly regulated sectors we most likely to see increased regulation as a bad thing: half of those from such sectors said that more regulation in their sector would be a bad thing, as opposed to just 18% who thought it would be a good or great thing.

‘Regarding regulation, it is required because we owe fiduciary duties and so we are regulated on investment limits and eligibility of investment assets,’ explains Sheila La Serna, chief legal counsel at Profuturo AFP. ‘However, there are always aspects that can be improved in regulation now that we are facing more digital relationships with our clients.’

Overall, counsel reported that their companies were well prepared for the event of a regulatory investigation: 76% said that their company has a response plan for such an event. Predictably, those that came from highly regulated sectors were more likely to have a response plan (89%) as opposed to those who came from sectors with less regulation (66% for those in lightly regulated sectors, 79% for those in moderately regulated sectors).

Traditionally, ethics and law go hand in hand. Law firm partners should have an innate moral compass. On that basis no distinction should be necessary between legally sound and morally or ethically justifiable advice, and for corporate counsel this distinction should not play a role either when mandating a firm. Ethics committees and supervisors should therefore – in theory – be superfluous. But that traditional approach is now seen as old-fashioned and incompatible with some aggressive profit-driven clients demanding aggressive profit-driven solutions. The danger for any law firm is that it is obliged to adopt the moral compass of its important (high-profit) clients and place money-making over traditional ethics. That is a problem that faces all major firms, not just Freshfields, although it is Freshfields that is providing a case study in how high-profit work can come at a reputational cost.

Traditionally, ethics and law go hand in hand. Law firm partners should have an innate moral compass. On that basis no distinction should be necessary between legally sound and morally or ethically justifiable advice, and for corporate counsel this distinction should not play a role either when mandating a firm. Ethics committees and supervisors should therefore – in theory – be superfluous. But that traditional approach is now seen as old-fashioned and incompatible with some aggressive profit-driven clients demanding aggressive profit-driven solutions. The danger for any law firm is that it is obliged to adopt the moral compass of its important (high-profit) clients and place money-making over traditional ethics. That is a problem that faces all major firms, not just Freshfields, although it is Freshfields that is providing a case study in how high-profit work can come at a reputational cost. Whether flawed culture has afflicted Freshfields is uncertain, but the danger for the firm is one of perception: whether those two malefactors are seen (fairly or unfairly) to indicate a deeper-seated problem in the larger organisation. At the very least, the crisis poses questions over internal checks and balances. The GC at a US retail company makes a blunt assessment: ‘The firm’s role in the scandal must be made clear and there needs to be a statement about the firm’s values, to which it will adhere in the future.’ Freshfields’ May 2020 code of ethical practice might have sought to answer the second part of this, but the risk for the firm is that it is seen as no more than a belated PR exercise to try to distance itself from the ongoing bad publicity without directly confronting the part it played in cum-ex matters.

Whether flawed culture has afflicted Freshfields is uncertain, but the danger for the firm is one of perception: whether those two malefactors are seen (fairly or unfairly) to indicate a deeper-seated problem in the larger organisation. At the very least, the crisis poses questions over internal checks and balances. The GC at a US retail company makes a blunt assessment: ‘The firm’s role in the scandal must be made clear and there needs to be a statement about the firm’s values, to which it will adhere in the future.’ Freshfields’ May 2020 code of ethical practice might have sought to answer the second part of this, but the risk for the firm is that it is seen as no more than a belated PR exercise to try to distance itself from the ongoing bad publicity without directly confronting the part it played in cum-ex matters.