Corporate crises have long called for General Counsel (GC) to apply their legal expertise and judgement.

But, with the rise of cyberattacks and data breaches, a greater focus on environmental, social and governance issues, class actions and the emergence of more powerful artificial intelligence, GCs are contending with more frequent and varied crises.

GCs are also playing a larger role in helping businesses navigate such events. Instead of simply being asked for legal opinions, they find themselves and their offices leading the coordination of internal response teams. They are also being asked to have a view about the ‘right’ path forward for the company – one that considers both ‘hard’ and ‘soft’ law standards and wider community and stakeholder expectations.

To explore how companies are approaching these issues, the Ashurst Leadership Centre convened a roundtable in partnership with The Legal 500 in Sydney in November 2023. The event was attended by 15 GCs from Australia’s largest companies and Ashurst partners and communications experts.

The discussion was facilitated by Lea Constantine, Partner, Head of Region – Australia.

In 2021, The Legal 500 partnered with Irwin Mitchell to produce our ESG Risk Report. Since then, we’ve seen environmental and social issues dominate corporate agendas, but comparatively, there has been little focus on governance. This is despite the fact that implementing a robust corporate governance plan provides a framework which will maximise protection for the stakeholders’ interests, reduce reputational risks and help companies to gain an advantageous position in the market.

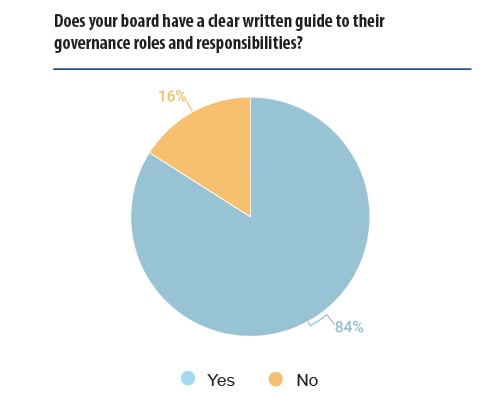

Traditionally, board directors have, almost exclusively, been responsible for governance-related matters; however, as the role of general counsel (GC) evolves, and as the results of our survey suggest, board members are looking to their in-house counsel to pre-empt and reduce governance risks. Further, with many sustainability questions and issues not yet being clearly addressed by regulation, in-house teams are rightly being asked to work with people across their business to put resilient governance and reporting frameworks in place.

We surveyed over 115 in-house lawyers worldwide to gather their insights for how to develop and implement successful and forward-looking governance programmes.

In-House Legal Research Team – GC Magazine

Irwin Mitchell Comment

‘Effective and transparent governance is an essential part of the business toolkit for companies that want to thrive in today’s rapidly evolving and competitive business environment.

Although the G in ESG rarely makes the headlines in the same way as environmental and social factors, good governance is fundamental for building trust in and across any organisation, as well as long term sustainability and value.

How businesses operate is increasingly influenced by a wide range of stakeholders including employees, customers, suppliers and communities as well as shareholders and investors. Their priorities and values go far beyond regulatory and legal requirements, and the bottom line. For GCs and in-house teams, this means that the landscape of risks and opportunities that they oversee has changed considerably in recent years, and the pace of change continues to accelerate.

I’d like to thank everyone who contributed to this research for sharing their time and insights with us. We hope you’ll find this report a useful resource for guiding your business in developing and achieving its governance aspirations. But this is just the start of the journey, and we’d love to hear your thoughts on how governance and the role of the GC in progressing this agenda will evolve

from here.’

Hannah Clipston, Director of Strategic Growth, Irwin Mitchell

Foreword

Board members across the world are familiar with the theory of effective governance. It embraces several key aspects, including regulation, compliance, good practice and board ability. Over the past few years, a two-fold evolution has meant the traditional appreciation of governance has moved on from the textbook approach. First, the role of general counsel has undergone significant transformation in the past decade, which has broadened its scope to strategic partner, prompting companies to expect corporate counsel to – among other things – provide advice and strategic guidance on corporate governance and all ESG-related matters.

The second evolution concerns the concept of governance itself. The concept has historically been used to describe transparency and accountability within the corporate sector. As business models have evolved and become more complex, companies have used governance models to enforce ethical corporate behaviours, both internally as well as with external stakeholders.

The past few years have seen a proliferation of statements, proposals and revised codes of corporate governance. While some of these statements reaffirm conventional doctrines and practices, others call for efforts to better align corporate activities with society’s interest in building a more inclusive, equitable, and sustainable economy.

In today’s market, with a customer base that holds expectations that can exceed a business’s legal and regulatory obligations, and is becoming more discerning on where and with whom they do business, ensuring alignment between a business’ purpose and what it does in practice is critical in building trust, both internally and externally.

In-house counsel have a pivotal role to play in the development and implementation of effective governance programmes that will steer the way a business conducts itself and ultimately, its success.

Key factors: In good governance

The research identified three key factors in creating a governance framework that is successful. These issues were repeated by the in-house community, regardless of sector and geography.

Focus on engagement: before creating your framework, spend time on gaining buy-in from all levels of the business including the board, the wider leadership team and team leaders who will be accountable for implementing the framework. Take time to listen to the business about their day-to-day work, challenges, expectations and what works well already. Socialising ideas and changes is important too.

Furthermore, ‘always listen, learn and adapt, because the theory doesn’t always work in practice’.

When developing the framework, keep it simple and use training to ensure that everyone is clear on what the objectives and expectations are and why they are important. You may also consider starting small with some key areas, gaining traction and then growing from there, rather than introducing wide-ranging changes in one go.

‘Make sure you have a progressive plan. Start small and get buy-in from leadership and employees, and then move to bolder actions’.

Create a framework that is specific to your organisation, its goals, strategy and risks as well as the regulations it is bound by. Hiring consultants or carrying out research within your sector will help you to gain insights and ideas which can be adapted into achievable and measurable governance objectives that will resonate within your business.

‘Every organisation is unique. Connect with your organisational requirements to propose a customised governance module that offers a mix of innovation and dynamism without making the stakeholders uncomfortable.’ Or, more succinctly put: ‘don’t copy and paste’.

This report considers each of these factors in more detail and provides practical guidance on how to achieve each of them.

Engagement with your board

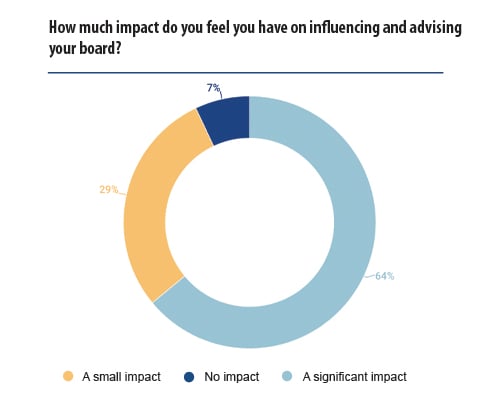

One of the key factors for achieving good governance identified in the survey was the ability for GCs to influence the board, and it is positive that the majority of the respondents felt they could both influence and challenge their board of directors.

Influencing and challenging your board

GCs play a crucial role in advising the board when it comes to risks, compliance and regulatory-related issues. But to be truly effective, GCs need to look beyond their immediate area of expertise. As one GC said to us, ‘we are not only lawyers, we are part of the business. I think my advice to other GCs would be: you have to be part of the board, because first of all, you are part of the business.’

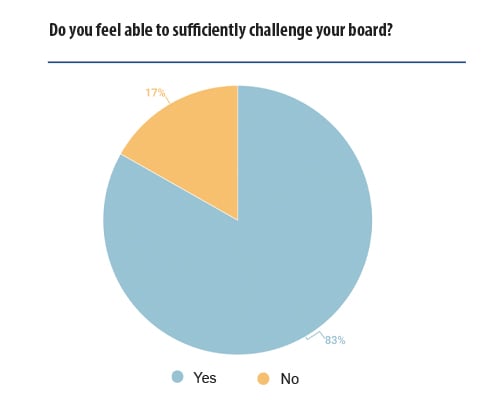

Overall, even though a vast majority of GCs expressed the ability to sufficiently challenge boards of directors, the respondents expressed an interest in having more direct engagement at board level. This would help them to have a better understanding of the business drivers and focus on the ways the legal ecosystem can support them. ‘Our role is to prevent any risks the company faces in its business and projects. Direct access is the best way to influence it’, another interviewee explained.

Advice: How to increase your influence in the boardroom

The advice from our respondents, for those looking to increase their influence in the boardroom can be split into three key areas:

First and foremost you need to be in the boardroom, and once you are there:

Invest time in winning support from senior advocates

But always maintain an independent advisor role and don’t shy away from uncomfortable truths

Don’t be afraid to express your views on non-legal matters

Always keep one step ahead in order to proactively provide training, guidance and advice

Implement a robust horizon scanning programme to ensure that whatever the future risk might be, they hear it from you first

Spend time to understand all facets of the business and create training and guidance focused on specific business priorities and risks

Be crystal clear on what your expectations of the board are

Articulate the value of good governance

Quantify risks in relation to brand values, reputation and business operations

Measure and benchmark progress so it can be used to demonstrate competitive advantage to your board

Ensure your messages are considered constructive rather than obstructive and always frame advice so that it speaks directly to business needs and future growth

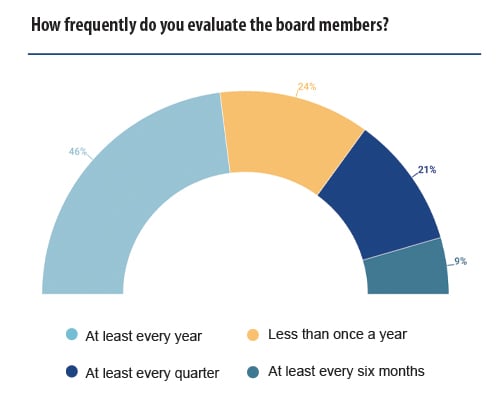

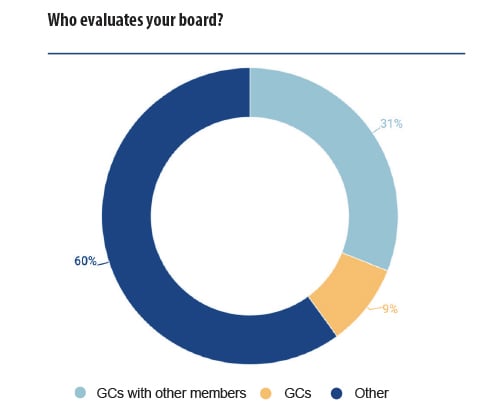

Who evaluates the board?

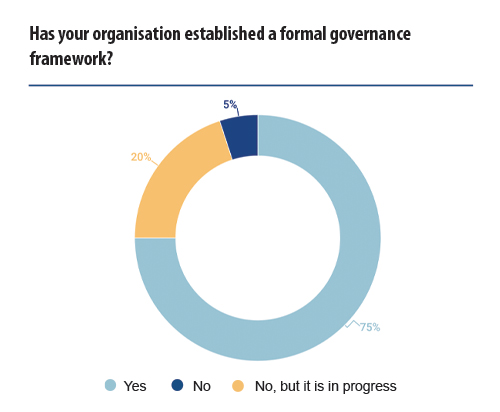

When you have achieved buy-in from your board, or are trying to do so, understanding the evaluation procedure for the board is critical. The ideal scenario is to link good governance, along with other E&S targets, throughout the organisation with reward at a board level. However, that can only occur when there is a clear and transparent board evaluation culture and procedure. Here, we look at how boards are currently evaluated.

Typically, the board of directors carries out a self-assessment where it evaluates itself, often alongside an external independent group, such as a consultancy or audit firm. Some boards of directors take the view that relying solely on self-assessment may provide either the perception of a conflict of interest or may lead to a biased assessment. Therefore, in these cases, this evaluation is carried out by an external auditor to provide, in the opinion of one respondent, ‘an objective view’ of the status of the company.

As one respondent notes, due to the structure of many companies, members of in-house counsel may be part of developing a governance programme, but they generally do not participate in follow-up assessments of whether compliance has been met. One GC noted: ‘As an employee I do not evaluate the board of directors. The board does a self-assessment regularly with the assistance of an external consultant’. If, however, as some companies have done, they brought in-house counsel onto the board of directors, this would allow GCs to continue their involvement in governance frameworks beyond their initial development.

Notably, 60% of respondents noted that GCs did not participate in evaluating the board. Within this cohort, the responses included self-evaluation by the board; evaluation by an internal team not connected to in-house counsel, such as shareholders; and/or evaluation by an external team.

Interestingly, in some cases, even when governance standards had been adopted, some respondents expressed disappointment about a lack of any standards for board members. One respondent said, in response to our question as to who evaluated the board of directors, ‘No-one. Unfortunately’. This shows that while even if good governance policies have been set, that is only the first (and perhaps) easiest step. Without a way to reliably evaluate whether standards have been met, proposed governance programmes will be no more valuable than the paper they’ve been printed on.

The responses by in-house lawyers made clear that they felt linking board performance on good governance to objectives and reward, coupled with an external and independent entity to evaluate performance, provides a valuable incentive for the board to promptly implement governance goals in measurable ways. Unfortunately, this has yet to happen in many organisations and continues to be an area for improvement.

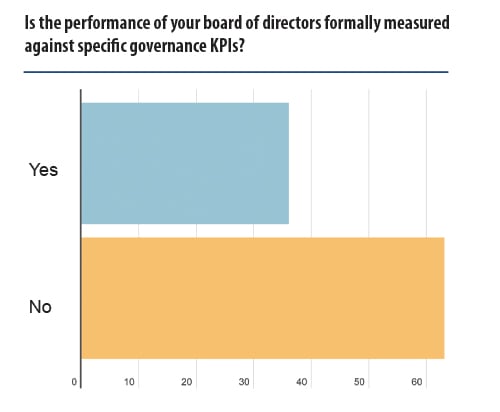

A follow-up survey addressed both measurement of performance of boards and remuneration of directors. The first question’s respondents gave a strong split, with one third noting performance was formally measured against specific governance KPIs.

Some responses noted they implemented the S&P’s DJI ESG scores, while others had developed bespoke policies, with one noting their 2030 agenda consisted of ‘30 cross-company goals that align to outcomes of sustainability, equity and trust’. Others emphasised corporate compliance, gender equity and diversity, while some highlighted a ‘specific focus’ on ‘ethical-related risks’ or a ‘holistic view on enterprise risks’.

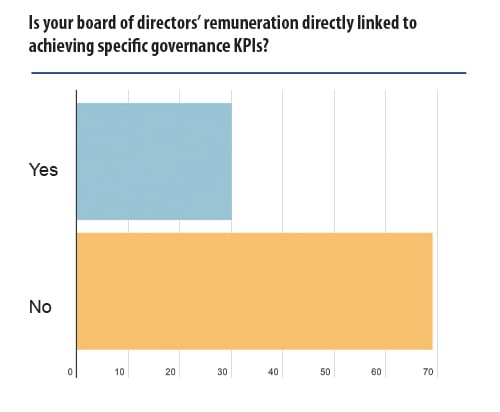

The responses to the second follow-up question track the first, with a little under one third noting that their board of directors had remuneration policies directly linked to achieving specific governance KPIs.

Cross-referencing the two questions, we discovered a full 54% of respondents had neither any formal measurement in place, nor any remuneration to boards of directors directly linked to achieving specific governance KPIs. Only 21% of respondents had both formal measurements in place as well as a form of remuneration in place to boards of directors directly linked to achieving specific governance KPIs.

This demonstrates that there is still a long way to go for boards to be collectively and personally accountable for governance in their organisations. However, it is clear that progress is being made and it will be interesting to evaluate if those who have created a firm link develop a better governance culture and improve business performance as a result.

Diversity in boards

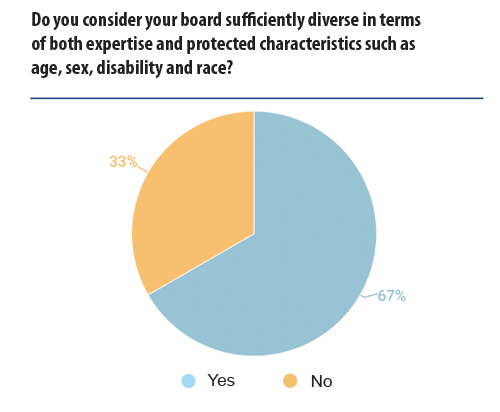

Another key issue that companies are faced with when considering good governance is the diversity of their board, including gender, ethnicity and diversity of thought among others. While this is often something in-house advisors may struggle to influence it does bear consideration, including when looking at how to influence your board and what issues may have differing levels of importance to them. Here, we look at the thoughts of those surveyed on the diversity of their own boards.

The statistical data provides a positive sign regarding diversity on boards of directors, with two thirds believing their boards of directors to be sufficiently diverse. This reflects a strong focus in recent years on board diversity, with the associated improvement in governance it is felt this can bring. It was, however, noticeable that the feedback from GCs who responded with ‘No’ painted a general picture of frustration from in-house counsel that their board of directors were generally older, white men, and what steps had been taken to improve diversity regarding gender were, in the words of one respondent, ‘minimum and limited’.

However, while some expressed frustration at failures to diversify boards of directors, others expressed optimism towards future improvements: ‘We have taken actions, including raising the non-diversity issue with the local board and explaining to them how this lack of diversity will be perceived’. It should be taken as a positive that improvements have been made and that action continues to create more balanced and diverse boards which are essential for tackling increasingly complex commercial issues, often requiring innovative and creative solutions.

Irwin Mitchell Comment

‘Increasing diversity at board level helps to create more inclusive and collective governance, and strengthens an organisation’s ability to respond to and anticipate change in ever-evolving markets and client bases. Greater diversity has been shown to bring about improved productivity and performance, a more responsive approach to client needs and increased innovation and creativity through a sense of belonging and the power of diverse thought. Therefore, a diverse range of board members brings with it a valuable range of perspectives and experiences to decision-making and problem-solving.

You also can’t underestimate the power of senior role models, particularly at board level, for under-represented groups and the impact this has on an organisation’s culture. While change on this doesn’t happen overnight, more can be done to recognise where there is a lack of diversity at board level and in wider decision-making groups and to seek out more diverse views to inform decision-making. Board members can act now and challenge views presented to them to ensure that diverse views have been taken into account in shaping proposals and policies prior to approval, while work takes place to increase the overall diversity of the board and the talent pipeline within an organisation’.

Charlotte Delaney, Diversity and Inclusion Manager, Irwin Mitchell

Irwin Mitchell Comment

‘Looking to the future, businesses are having to think more and more about how to generate innovation in order to respond to increasingly complex customer needs. Within Irwin Mitchell, we want to ensure that our products and services evolve so we are constantly exceeding client expectations. We know this is dependent upon attracting and retaining diverse talent and future leaders so we can benefit from different perspectives and experiences at all levels across our business. This starts with a commitment to widening access and increasing social mobility and by participating in initiatives like our new mentoring programme with City University, access to work experience with PRIME and increasing our apprenticeship offerings, we provide opportunities for students who might not otherwise have considered a career within the legal sector.’

Satinder Bains, Partner and Chair of Irwin Mitchell’s Social Mobility Colleague Network, IM Aspiring

Keep it simple

Ensuring your governance framework is simple and well understood is key to its success. Complex structures lead to a lack of understanding and engagement. This section looks at some of the challenges to embedding a good governance structure, and with winning buy-in from the business’ people at the top of the list, the importance of a simple, well understood and articulated plan cannot be overstated.

Challenges to embedding good governance

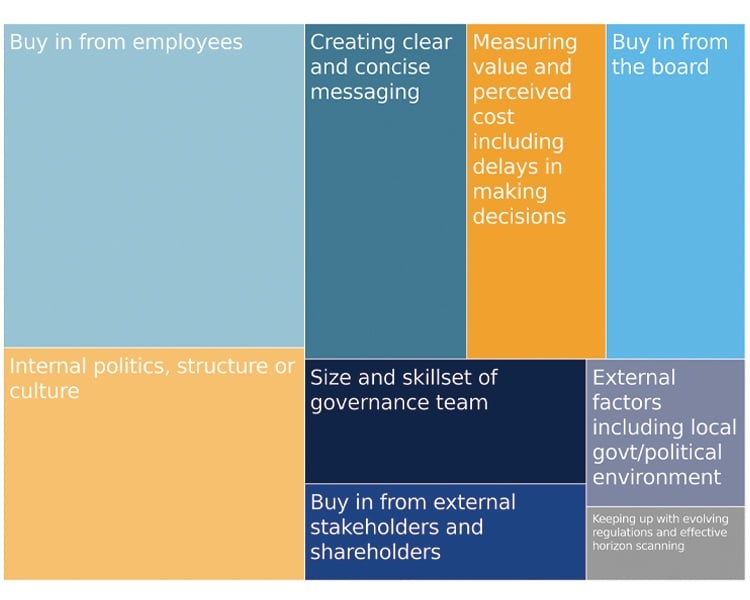

We asked about the main challenges to achieving good governance in an organisation, and while some cited difficulties caused by external factors such as local culture and politics, the majority of responses related to internal factors that GCs can actually influence.

Employee buy-in is considered the main challenge to achieving good governance, and this is noted as particularly tricky in organisations with high staff turnover, where employees are located over multiple sites and jurisdictions, and when people are already time-poor. But clear and concise messaging will go a long way to garnering buy-in. In addition, small steps can help bed in the framework, creating a simple starting point which can then be built on.

As one GC we spoke to pointed out: ‘The biggest difficulty is communicating clearly and in a manner that cuts through the noise of so many other regulatory, reputational and business demands on the attention of all stakeholders, including, not least, employees’.

Similarly, boards and other stakeholders will be more inclined to support governance issues if they have clarity on the costs of taking or not taking certain actions.

Formulating a simple framework which includes measurable principles provides valuable data which can be used to the advantage of the business. 75% of those surveyed said they use governance data and achievements in their marketing to employees and new hires, as well as customers.

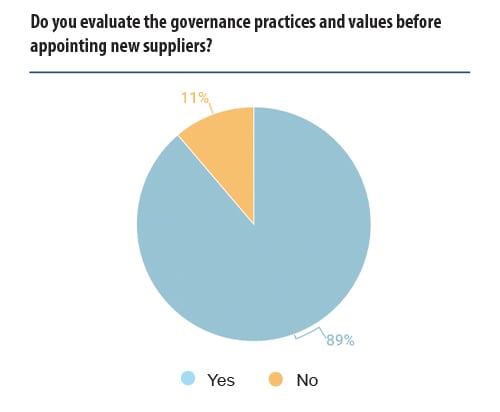

At a time when GCs are increasingly looking for ESG as part of their own supplier procurement process, having readily available and clear metrics on ESG compliance, including governance, is becoming a must-have for any business who wishes to grow, recruit and attract investment.

Irwin Mitchell Comment

‘A robust governance framework is critical to our Responsible Business strategy. As well as ensuring that we set sufficiently challenging KPIs and objectives around our work, we engage external partners and participate in a number of benchmarks and accreditations to measure our progress and ensure that we continue to make an impact. We report on our performance in our annual Responsible Business report.’

Kate Fergusson, Head of Responsible Business, Irwin Mitchell

Make it specific

A key factor in success was making the framework specific to your organisation. This will necessitate in-house counsel understanding the needs and issues within their business and prioritising their governance objectives accordingly, which will then naturally flow into the framework for your organisation.

This section considers the priorities and aspirations from those surveyed, to provide support when considering some of the aspects you may wish to examine while looking at your own specific governance framework.

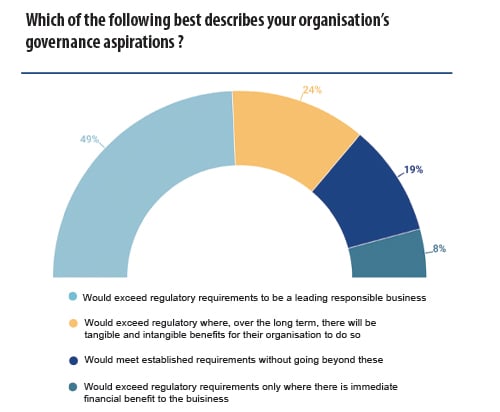

Governance aspirations

In our study, we found that most companies’ governance aspirations go beyond regulatory requirements. 48.7% of those interviewed stated that they would exceed regulatory requirements to be a leading responsible business because, simply, it is the right thing to do, rather than for commercial

gain. A further 23.5% say they would exceed regulatory requirements where, over the long term, there will be tangible and intangible benefits for their organisation to do so.

These figures demonstrate that for many, governance has moved on from being seen as a compliance exercise to a more strategic framework built to support sustainable business growth and impact.

19.3% of those surveyed would meet the established regulatory requirements without going beyond these, and the remaining 8.4% would exceed regulatory requirements only where there is an immediate financial benefit to the business, such as on cost savings.

Irwin Mitchell Comment

‘The direction of regulation and of client, colleague and community expectations around Responsible Business are clear and accelerating. Today’s aspirations and “nice to haves” will soon become tomorrow’s bare minimums. And changes of this scale in business take time to implement effectively. So a significant factor for the long term sustainability of all businesses is anticipating successfully the direction in which change in the business ecosystem is happening – and not just looking at today’s position (as you will fail to meet future needs if you do) – and then starting the change process proactively in that direction so that the needed changes are completed in the business in line with or even ahead of, rather than behind, the competition.’

Bruce Macmillan, GC, Irwin Mitchell

Understanding your priorities

priorities for the next 12 months

For the majority of respondents, the main focus for the year ahead is on their governance policies, frameworks and programmes. For some, it is about putting these into place while others are looking to refresh and update. Improving accountability and compliance also scored highly.

Looking at specific types of risk, unsurprisingly ESG tops the list, and drilling down further it is environmental issues that are highest on the agenda. This reflects the general trend in society and from stakeholders to ensure these issues are considered and understood, and appropriate governance procedures put in place to manage the risks.

As to cybersecurity and data privacy, respondents pointed out how organisations benefit from a comprehensive, integrated and centralised strategy for achieving data privacy compliance. Data sharing, they say, should have stricter controls and policies, which implies either current legislation is not being complied with or does not go far enough. Organisations should develop more solid data security compliance methods to track personal data in accordance with legal standards.

Irwin Mitchell Comment

‘We often see that organisations don’t have a complete picture of all the data sharing happening either from an intra-group perspective or with third parties. This is particularly the case with increased globalisation – there is often data export which is overlooked. For example there can be line management in groups done by managers in other group companies and other countries. IT and tech contracts often have an international aspect somewhere in the supply chain. Since the compliant export of personal data is a hot topic at the moment for the ICO and the European regulators it is important to understand what data sharing and export is happening and to ensure that it is compliant. Things are complicated by the fact that the data export rules and standard export contracts have changed recently. The old approach of signing EU standard contractual clauses and forgetting about them doesn’t work anymore. The issue will be further magnified once the UK data protection reform happens. We don’t yet have sight of the draft legislation after the Data Protection and Digital Information Bill was scrapped but we understand that it is still on the cards.’

Joanne Bone, Partner – Commercial and Data Protection

Prioritising your framework

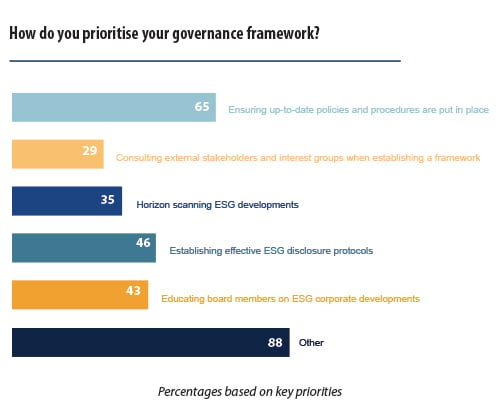

In terms of priorities, over 60% of GCs stressed the importance of having adequately up-to-date policies and procedures in place. This is a key starting point for any governance framework but it must be specific – companies should not adopt policies for the sake of it where they are not necessary or adding value. Over 40% consider the most pressing matter as the establishment of effective governance disclosure protocols and educating board members on governance developments. Less than half of the people interviewed see the necessity of consulting external stakeholders and interest groups when establishing a governance framework (29.41%) as a number one priority.

Nonetheless, it is interesting to note that under the category ‘other’, the majority indicated that their priority lies in organising training for all stakeholders to better achieve good governance and create a sustainable change. When it comes to taking the ultimate responsibility for achieving good governance, the general feedback is that this is a collective task, however,

the board of directors and key managerial personnel have the last word. The board’s purpose is to support corporate performance and establishing clear Key Performance Indicators (KPIs) and appropriate measures for evaluating against those KPIs. Linking that success (or failure) to reward helps focus the board on the importance of good governance.

This reflects the contents of this very report: that board engagement, simple policies which employees can understand and are trained on, aligned with a framework for for your business, are how you can achieve good governance success.

Irwin Mitchell Comment

‘Creating a Culture of Compliance, as we are doing, needs to have a clear metrication of what is right – directionally and in terms of what a material improvement or deterioration looks like; clearly and openly spelt out to leaders and team members – we use a Balanced Scorecard with Key and Leading Performance Indicators; and then their needs to be a clear, explicit and adhered to approach that makes good or poor compliance a material reward and promotion issue.’

Bruce Macmillan, GC, Irwin Mitchell

Looking to the future

Having established and embedded a good governance framework, the work of an in-house lawyer is not complete. Good governance practice continually evolves. This report has already flagged the importance of independent monitoring of compliance and performance against the background of the governance framework set. However, from a commercial perspective, the focus of a business will shift to reflect new trends and demands from stakeholders, customers and employees.

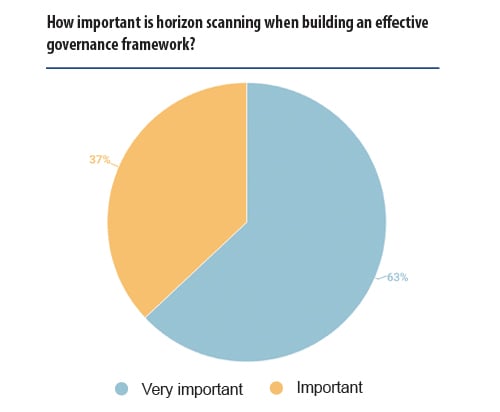

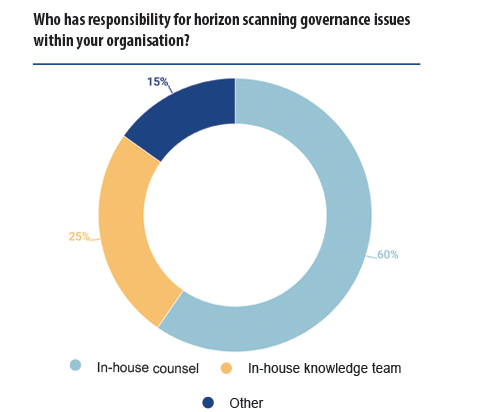

Keeping your governance policies and procedures up to date requires a strong emphasis on horizon scanning, together with regularly revisiting your materiality assessment to understand the key issues for your stakeholders and which will impact your business and governance framework.

Like the captain of a ship, in-house counsel need to be able to identify ‘hidden icebergs’ and thorough horizon scanning will detect future disruption along with new opportunities to build into responsible business plans which will positively impact their business and society. Effective horizon scanning also provides decision-makers with the time to plan their response, and clear communication with external partners ensures those in the supply chain have the opportunity to ‘stay ahead of the game’.

As well as relying on monitoring services and updates from external experts including law firms, auditors, regulators and the government etc, the GCs surveyed take advantage of networking events, training and digital forums such as LinkedIn groups to ensure they are keeping up to speed with what is on the horizon.

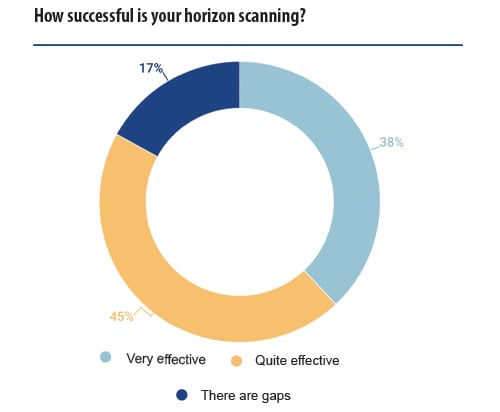

The majority replied that the horizon scanning in place is effective in identifying governance issues before they arise. However, gaps persist. Under the gap section, interviewees expressed a willingness to have more resources allocated within the in-house legal team. Until then, working alongside your legal advisors and other sources of updates should be a priority to ensure your governance framework remains fit for purpose.

The pace and scale of societal, economic and environmental challenges facing us means we need to generate innovation and creativity within our organisations to quickly devise and implement solutions. This will require diversity of thought and openness to collaboration across our own business and the wider economy.

By leading the focus on effective governance against measurable KPIs which are understood and supported, GCs can be at the forefront of this challenge, making a difference to not only their organisations, but to society as a whole.

Conclusion and practical tips

Establishing a successful governance framework relies on many different things but its importance to a business should always be remembered. The G in ESG is often overlooked, but for a business to be successful it should be a core part of its focus, from the board to employee. The role of the in-house lawyer in achieving that can look daunting, but by focusing on getting the right engagement, keeping your plans simple and being specific to your organisation, you can achieve success.

In the column on the right, we have set out a checklist from the research to help you assess where you are on your governance journey, and what the next steps are for you and your organisation.

Checklist: For ensuring good governance

Communication

Are your governance policies available and easy to find for employees and external stakeholders?

Are your policies written in a way that means everyone is clear on what’s expected in terms of their individual and collective duties and behaviours, and why?

Do you have a training and communications programme in place to regularly remind people about new and existing governance matters? And for new employees as part of their induction?

Compliance

Do you undertake scheduled and/or unannounced audits and checks on employees and suppliers?

Are your procurement documents and standard contracts regularly reviewed and updated to incorporate evolving governance requirements and KPIs?

Do you have a robust horizon scanning system/process in place to ensure your policies reflect new and forthcoming changes?

People and culture

Do you (as a GC or more widely as an organisation) have a sufficiently resourced and proactive team with responsibility for creating, implementing, reviewing and measuring your governance programme?

Does the board ‘walk the talk’? If not, do you have at least one senior leader to be your ambassador?

Is your board evaluated and rewarded based on successful governance compliance?

Even before the Covid-19 pandemic altered businesses and society, the environmental, social and governance (ESG) movement was gaining steam within corporate circles. Issues of climate change, consumer pressure, regulatory reform and social movements, were top of mind for investors and executives.

The global pandemic only further heightened the awareness around ESG, and the social impact of severe lockdowns and business instability forced companies to rethink their priorities. As a result, ESG issues such as environmental sustainability, social justice, and emerging reporting disclosure protocols have dominated corporate news headlines around the world.

ESG reporting has been voluntary in many countries, but in the last 12 months the EU – along with many other national governments and regulatory bodies – have issued ESG reporting guidelines. As the move towards establishing a common reporting standard around ESG continues, corporate counsel have been tasked with implementing effective protocols and oversight.

GC partnered with Irwin Mitchell to gauge the ESG outlook of leading corporate counsel across Europe and the United States. With the 26th UN Climate Change Conference (COP26) taking place in the United Kingdom from 31st October to 12th November 2021, the ESG agenda has been cemented as a business imperative for general counsel. This research documents the thoughts and opinions of more than 190 in-house lawyers on ESG, their risk outlook, and how a shift in business focus has shaped their legal agenda.

In-House Legal Research Team

GC magazine

Irwin Mitchell Comment

Irwin Mitchell is determined to become a leading responsible business. We’re already on a journey to ensure that our environmental, social and governance values are embedded into our business and influence our relationships, strategies and aspirations. But to be truly successful, we need to proactively engage in conversation and collaboration; with our colleagues, with our clients, within our business and geographic communities, and, setting commercial competition aside, with our peers across the legal sector. In doing that, we believe our aspirations will be realised and we will lead as a responsible business. We’re delighted that so many in-house counsel contributed to this research, and I’d like to thank them for their time and for sharing their insights into the role of in-house in setting and supporting the ESG agenda within their businesses. We hope that you’ll find this research useful in plotting where you, your team and your business are on your own ESG journey, and where it will take you next.’

As pressure for sustainable and ethical corporate practices from regulators, investors and consumers mounts, ESG has become the most pressing topic in the boardroom.

From our research, a staggering 96% of corporate counsel reported that their companies have either implemented a formal ESG plan or are in the process of developing one. While this focus is not new, treating ESG as a crucial component of the business and governance framework has increased in recent years.

GCs are placed in a unique position to take the lead, and influence company policy. Increased focus from regulators has been one key driver, explains a survey respondent: ‘ESG has become the main focus of regulators and certain key players in the financial sector. The fact that these players promote ESG best practices means that other market participants should make ESG a priority to keep up with the best practices and improve the chances of better financial return in the longer run.’

Before the pandemic, ESG reporting was a nice-to-have niche. But 2020 saw several major regulatory developments from the European Union:

The Sustainability-Related Disclosure Regulation (SFDR) lays down the ground rules for financial markets on transparency

The Corporate Sustainability Reporting Directive sets out legislative goals

The Taxonomy Regulation (TR) defines what is regarded as sustainable.

Meanwhile, in the United States, although there are no mandatory ESG disclosure requirements, the Biden administration has declared its intentions to make sustainability a priority. In 2021, the House of Representatives passed the ESG Disclosure Simplification Act, requiring public companies to make ESG disclosures in their Securities and Exchange Commission (SEC) filings.

Does your company have an ESG plan?

Echoing this sentiment, the UK government has also indicated its intentions to introduce its own mandatory ESG reporting requirements. Currently, there is no single over-arching ESG regulation, but rather a disparate array of regulations that touch on ESG concerns. The Corporate Governance Code 2018, Companies Act 2006 and the Disclosure Guidance Transparency Rules all set out the current ESG disclosure regulations.

The fragmented legal policies around ESG, and the regulatory notices governments have put forward, signal to lawyers and businesses that a unified ESG framework is in development.

One respondent from the financial sector explained: ‘There is a much greater focus in the regulatory sphere when it comes to ESG. Covid-19 has accelerated this interest and legal teams will play a key role in managing these changes.’

Irwin Mitchell Comment

‘Although there is currently no global standard for ESG reporting, there is a huge range of legal reporting requirements for businesses. In the UK alone there is a wide variety of existing and incoming legislation that involves important elements of ESG reporting such as gender pay gap reporting and modern slavery statements. In addition, we believe that some of the confusion around current ESG reporting obligations has arisen from the fragmented reporting framework that places obligations on companies depending on their size (rules for large undertakings under section 172 and 414 Companies Act), whether they are listed (arising from the Disclosure Transparency Rules and UK Governance Code) and whether they are in the regulated financial services sector (Prospectus regulations, Disclosure Guidance and Transparency Rules and Market Abuse Regulations).

The current reporting requirements are disparate and can be difficult to navigate. It’s clear that in-house counsel will play a crucial role in guiding businesses through their approach to ESG and how ESG performance is measured and reported both now and as harmonised ESG reporting obligations are introduced. As standardised reporting is introduced, we are likely to see the introduction of financial penalties for non-reporting or false reporting and in-house counsel will become even more important in bringing key ESG stakeholders together to make reasoned and justified decisions to allow effective reporting and compliance’.

Jason Newall, Senior Associate Solicitor, Regulatory and Crime

Ignore at your own peril

Whilst regulators work towards legislating ESG obligations, our survey results highlighted that companies have already started prioritising key areas.

Unsurprisingly, it was reported that 42% of ESG plans contained a governance framework. This was closely followed by plans containing published policies and guidelines, identification of ESG related risks, a named senior management sponsor, and KPI monitoring and reporting. Lower on the agenda was identification of ES-related opportunities and setting SMART objectives. In fact, it was alarming to note that almost 90% of respondents failed to take into account all of the above when considering their own ESG framework.

Given the increasing importance of ESG initiatives, responsibility still lies with a relatively small group of people. In 57% of the cases, ESG strategy was led by one or no people, with the majority (83%) of those individuals reporting to either their CEO or CLO. A GC from the transport industry commented: ‘Depending on ESG strategies and targets, the responsibility should lie either with the Chief Executive Officer’s or the Chief Legal Officer’s department.’

When survey respondents were asked what areas they believed needed more investment to improve ESG oversight, 31% indicated the need to invest in a dedicated ESG team. This is reflective of the upward trend of companies creating new ESG-specific roles.

While 26% of respondents pointed to the ability of their organisations to continue operating in increasingly difficult conditions as a significant environmental concern, a larger number of GCs said that issues not directly tied to their organisations’ market performance were top priorities. This included, 31% or respondents saying they wanted to see greater investment in efforts to improve biodiversity or tackle pollution, and 38% saying resource use and the so-called circular economy was their biggest concern.

It is also clear that social issues are now deemed to be risk items relevant to the legal team. While issues such as working conditions or health and safety have long been a potential matter for the legal team, respondents were just as likely to see diversity and inclusion as an area needing their oversight.

What does your company’s ESG plan include?

The growing importance of new types of risk is even shaping GCs’ views on corporate governance. While the staples of fraud, bribery and corruption emerged as pressing concerns, just as many respondents said they wanted to see greater attention to corporate transparency.

Even five years ago, few general counsel would have felt that their role called for ensuring fair operating practices or scrutinising executive pay and boardroom diversity. Now they are seen as key areas of risk.

Nevertheless, legal departments are still expected to play a crucial part in setting the ESG agenda — although other business functions may share responsibility. As one respondent explained: ‘I think it should be sponsored at the highest level but that responsibility should sit across all staff and not just a specific team.’

Another survey participant said that spreading ESG accountability across numerous company functions would lead to better outcomes: ‘Different elements of ESG should have different owners,’ explained an in-house lawyer from the tech industry.

‘ESG should address all stakeholders and touch on all areas of a company’s business. Shared responsibility is especially important given the breadth of topics (operational/facilities, HR and Legal).’

ESG in more detail: where do GCs think investment is needed to improve oversight?

Environmental

Social

Governance

Avoiding pitfalls

General counsel play a unique role as the gatekeepers of good corporate practices and ethical considerations.

As guardians for disclosure controls, company litigation strategy and company compliance practices, ESG certainly falls within the corporate counsel remit. Our data reflected this with 63% of respondents reporting that they believe in-house legal teams play a ‘very significant’ or ‘significant’ role in ESG activities.

When asked in what way in-house legal teams are involved in ESG initiatives, 59% of respondents agreed that they contributed to the development and/or evolution of the ESG plan. Whilst 18% said they were involved in the creation and implementation of policies and their adoptions. Those who selected ‘other’ mainly focused on specific parts of the ESG agenda.

As the sustainability movement grows within the corporate community, GCs are not only important legal advisors to the companies they serve, they are crucial strategic partners. So as the trend towards ESG accelerates, having a broad grasp of the wide extent of its impact has never been more important.

Legal teams have become fully involved in ESG-related matters: analysing risks, developing ESG strategy and working on governance-related issues,’ shares a respondent.

In what way are you or your team involved in ESG activities?

Irwin Mitchell Comment

‘The in-house legal team’s role is to ‘help their business do “it” right’ – the “it” being sustainable, successful and compliant business.

ESG is now all pervasive – in the supply to the business, in the supply from the business, in the stakeholder and regulator expectations of the business and, increasingly, in colleague expectations of their employer. So getting ESG right is now at the heart of helping the business to get “it” right overall.

And the key to ESG is the G – the Governance. Contractual, regulatory, processes and policies allow you to document and deliver all the ES things your suppliers and customers want you to commit to.

In-house counsel owns G. Getting G right helps the business get its ESG right. That’s now a core part of in-house helping their employer get “it” right overall.’

Bruce McMillan, General Counsel

The need to focus

Although governance oversight is essential for corporate counsel, it is interesting to note that GCs are placed in a unique position to take the lead, and influence company policy. As a result of the regulatory push towards sustainably conscious guidelines, ESG has become an essential part of influencing investment decisions.

According to the data collected, a total of 92% of survey participants shared that they had either completely, or to some extent integrated ESG into their companies’ investment decision making process.

For this reason, it was no surprise to see this shift in investment sentiment influence GCs to realign their legal objectives. When in-house counsel were asked what their company’s top motivation was for investing in ESG, just under half of respondents (47%) said improving long-term returns. The second highest motivation was ‘doing the right thing’ (12%) followed by ‘environmental sustainability and resilience’ (11%).

Explaining the motivation behind focusing on ESG initiatives, one survey respondent explained: ‘an increased interest from the public about ESG will drive many more companies towards the adoption of ESG practices.’

Does your business integrate ESG criteria into investment decision-making?

Irwin Mitchell Comment

‘The G in ESG is becoming increasingly more important for businesses in the funds and investments space; aligning how you operate your own business with your external ESG messaging is crucial. The impetus for businesses to build ESG into their investment decision making is driven partly by the introduction of new regulation and partly by the growing appetite and demand from stakeholders, whether they be shareholders, investors or customers. Post Brexit the UK has not ‘onshored’ the EU Sustainable Finance Disclosure Regulation (SFDR) into UK domestic law, opting instead to make disclosures that are aligned with the Task Force on Climate related Financial Disclosures (TCFD) fully mandatory by 2025 but there is a general view that it still has a number of indirect/practical implications for funds and investment related businesses in the UK given the UK’s Green Finance Strategy and the fact that ESG considerations will become integral to future EU trade deals and the ability to attract international capital.’

Sean Scott, Partner, Banking and Finance

Risk appetite

Since the pandemic, ESG concerns have propelled to the top of the business risk agenda, and corporate counsel have taken notice.

When GCs were asked if they had incorporated ESG issues into their own risk and resilience plans, 85% reported that they had. This shows that corporate counsel understand that failure to address ESG matters have both reputational and financial risks.

‘ESG is transforming from being a reputational risk to becoming a legal risk. This is particularly obvious when we consider the close adoption of EU legislation in the field,’ explains a survey participant.

When it comes to determining ESG risk, GCs were asked what they believed fell wholly within the remit of their legal team. The threat of regulatory sanctions ranked at the top at 47%, with a further 16% of respondents selecting that this risk fell within the remit of their legal team. Other risk areas that ranked highly included the threat of litigation and corporate reputation.

With new legislative reform around ESG on the horizon, the risk for regulatory liability is an anticipated threat. However, the ESG outlook — if appropriately adopted — does present opportunity.

Which of the following risks fall within the remit of your legal team?

Generating goodwill from showcasing sustainable practices will go a long way with stakeholders. On the other hand, doing the opposite may lead to embarrassing disclosures triggering fallout with investors, employees and consumers.

The data collected is undeniably indicative of the pressures felt by in-house counsel to incorporate ESG into their risk and resilience plans. The pace at which regulatory changes are occurring are making some in-house counsel nervous. A GC from the finance sector explained: ‘From month to month, I can see that environmental issues and regulations are becoming more serious, visible and severe. Results, revenues, incomes and dividends are going to be pivotal when light is directed to them.’

So when it comes to risk, should companies be investing more? The majority of corporate counsel believe businesses should be investing more (68%). The question which then arises is, should this investment be directed at systems, people or knowledge and training? As the risk appetite shifts towards ESG, knowledge and training was considered the area in which investment was most required.

As business priorities shift, training teams to understand new legislative protocols is an important company investment. ‘The way of doing business in the future is transitioning and

the regulations are moving in a particular direction. Understanding this will be necessary to avoid legal risks,’ says

a survey respondent.

GCs are often the torch bearers of responsible conduct. When it comes to manging risk, in-house counsel are well placed to ensure adequate protocols and policies are developed and managed. As ESG becomes the new industry focus, our data highlights that in-house leaders are at the forefront of managing the risks and opportunities a new framework may provide.

Irwin Mitchell Comment

‘ESG is not just about risk management. It is about everything an organisation does and how it goes about doing it. Effective risk management is an essential mechanism for identifying and managing the risks across an organisation, so as to best avoid unnecessary problems and potential reputational damage.

‘In this context, identifying and defining the most relevant ESG risk factors for your organisation and incorporating them into your existing risk frameworks should be a priority.’

Georgie Collins, Partner, Intellectual Property and Media

Irwin Mitchell Comment

‘For two weeks in autumn 2021, the eyes of the world will be on Glasgow as it plays host to the UN Climate Change Conference (COP26). These talks will bring together heads of state, climate experts, leading businesses and campaigners to discuss a coordinated action plan to tackle climate change. Top of the agenda will be the urgency around net-zero commitments and the need for business transparency and accountability.

For the UK, we hope that these discussions will be the catalyst needed to bring the long awaited Environment Bill to fruition. This Bill introduces a green watchdog in the form of the Office of Environmental Protection, which is already taking cases in its interim function. We’re also waiting to hear more about the ‘strong and meaningful’ targets relating to the four priority areas: biodiversity, air quality, water and resource management. Although the target deadlines won’t kick in until sometime in the mid to late 2030s, in-house counsel will need to be alert to the interim targets which will be set to make sure progress is made sooner, rather than later. We can expect to hear more about this in the coming months and years.’

Claire Petricca-Riding, Partner and National Head of Planning and Environmental Law

Greener pastures

As the social and economic impacts of Covid-19 continue to play out on the global stage, 85% of corporate counsel believe ESG will remain a top priority for GCs in the future.

In recent months, the ESG movement has shifted from a non-essential requirement to a vital reporting standard for investors and other stakeholders. Nevertheless, ESG is still in its infancy, with forthcoming legislation on the horizon expected to unify reporting standards.

But for many GCs, there is an even more pressing reason to take these issues seriously: ‘The planet continues to face an existential threat, so ESG must remain a top priority. This will likely be driven by both regulatory (SEC) disclosure obligations and investor interest in sustainable businesses.’

Another survey respondent supported this sentiment by saying: ‘I anticipate we, as general counsel, will become more involved in unpacking the requirements of the various ESG initiatives and support reporting. I also anticipate that there will be an update to legal agreements as ESG becomes more legally binding over time.’

Although ESG reporting isn’t a legal requirement yet, most ESG plans currently enacted are based on feedback from employees (45%). Other important stakeholders include investors and customers who play a crucial role in shaping the current ESG outlook. Going forward, this will likely change as ESG reporting legislation is enacted.

‘In future, ESG issues will likely become more programmatic as consistent standards are developed to allow broader and quicker adoption,’ predicted one survey respondent.

The survey data also indicated that GCs expect their ESG outlook to increase with importance within the next five years, as reported by 88% of respondents. Although 12% believed ESG would retain the current level of importance, it’s vital to note not one respondent thought it would become less important.

The unanimous consensus regarding the future of ESG highlights that the way of doing business is evolving. Although responsibilities around ESG obligations may vary between sectors and jurisdictions, the pressure in-house counsel are feeling from regulators, consumers and employees is universal.

Pre-emptive reporting requirements are reshaping the corporate agenda, with general counsel set to oversee the application of non-financial reporting rules and governance. As policy momentum accelerates, ESG trends are set to raise the corporate profile of general counsel among organisations. With more companies feeling the need to launch more holistic programs, policies and reporting frameworks, one thing is clear, general counsel are pivotal in managing this new focus.

Irwin Mitchell Comment

‘Diversity and inclusion, as part of a wider ESG agenda, provides clear opportunities for those businesses ready to truly embrace it. D&I cannot be seen as a job for HR; as something that should be monitored and reported on but then forgotten. A strategic approach that is embraced by all leaders including GCs must be taken to embracing D&I on a day-to-day organisational basis. We have seen huge leaps forward by businesses who are paving the way including for example the creation of shadow boards or “reverse” mentoring programmes. These businesses are already reaping the rewards of these programmes and those businesses who have not started to properly engage with D&I as an agenda item risk falling behind.’

In Latin America, concern for environmental and social issues is high and made more urgent in the Coronavirus era. Scarcely a day passes without newly issued statistics, a newly created ESG (Environmental, Social and Governance) index, investor groups weighing in, or a domestic or international political initiative in the area.

ESG is a complex topic, raising a broad range of issues. In Latin America, a number of these issues are centered on ESG investment. With the region demonstrating the strongest demand for ESG investment globally and an influx of public and private investment to aid in rebuilding economies after the COVID-19 pandemic, raising capital in the form of ESG bonds, green loans, and other similar instruments, is not only compelling to investors, but essential for the development of the region.

What is ESG?

ESG is the consideration of environmental, social and governance factors as a way of looking at the long-term sustainability of an entity, alongside backward looking and more short-term financial metrics. How ESG considerations impact an entity or investment opportunity depends on many investor-, entity-, industry-, country- and region-specific factors:

Environmental: How is an entity performing as a steward of the natural environment, including with respect to energy consumption, water management, pollution, and other material issues? Issues include climate change, protection of natural resources, development of renewable and/or low carbon energy, pollution, including carbon mitigation, control and waste management.

Social: How is an entity managing relationships with its employees, suppliers, customers and the communities in which it operates, as well as pressing socioeconomic disasters, such as the current COVID-19 pandemic? Issues include education, which encompasses human capital development within an entity, product quality, social opportunities, and access to healthcare and retirement benefits

Governance: How is an entity handling important structural, policy and behavioral matters, such as executive pay, board composition, ethics, transparency and shareholder rights? Issues include diversity, pay, ownership and control, and corporate behavior.

Forces Driving ESG Evolution

The environmental leg of ESG investing is one of the driving forces of ESG evolution in Latin America. Motivated by a push towards low carbon energy to address the looming threat of a climate crisis, both internal and external forces have played an integral role in its development. The signing of the Paris Agreement by 23 countries, coupled with the September 2019 public pledge by a coalition comprised of a number of the region’s jurisdictions to generate 70% of their electricity needs from renewables by 2030, has resulted in a wide range of opportunities for investors looking to expand their ESG portfolios.

Another driving force is the social leg of ESG investing, which includes addressing the vast gaps in healthcare that have been further exposed by the COVID-19 pandemic. The urgent need to make investments in the development of better health infrastructure and significantly improve access to healthcare is expected to be another source of ESG investment. As new investment vehicles are created to address these issues, such as the COVID-19 bond, this social need will inevitably continue to influence ESG investment.

Basics of ESG Investment

There is a range of ESG investment products, including bonds and loans. ESG bonds are securities issued to address specific Environmental, Social, and Governance matters. The most common ESG bond is a green bond issued by a public or private entity (including a sovereign) in which the issuer agrees to use the proceeds raised for dedicated ‘green’ purposes, typically environmentally friendly projects. A total of 1,802 green bonds were issued globally in 2019, up by 13% as compared to the previous year (according to the Climate Bonds Initiative’s ‘Green bonds Global State of the Market 2019’), and that growth has continued in 2020.

In the lending space, ESG-linked loans, also referred to as sustainability-linked loans, are any type of loan instrument and/or contingent facility, that incentivizes the borrower to meet predetermined sustainability targets. A green loan, in its strictest sense, is a type of ESG loan that has stringent requirements for the use of its proceeds, requiring that said proceeds be used exclusively to finance or refinance green projects, such as those tied to increased energy efficiency, avoided and/or mitigated carbon emissions, reduced water consumption or other assets that have a positive externality for the environment. Unlike with a green loan, proceeds from ESG-linked loans do not need to be allocated to a specific ESG project, rather proceeds from ESG-linked loans can be used for general corporate purposes.

Where is Latin America in the evolution of ESG?

Key ESG Players

ESG key players include a wide variety of entities, such as institutional investors, NGOs, ISS/Glass Lewis, and ESG standard setting bodies.

The International Capital Markets Association (ICMA) has launched the Green Bond Principles, the Social Bond Principles, the Sustainability Bond Guidelines, and as recently as June 2020, the Sustainability-Linked Bond Principles (collectively, ‘the Principles’). Serving as the Secretariat, the ICMA provides guidance for the governance of the Principles, which have become the leading framework globally for the issuance of ESG bonds. Taking the lead role in disseminating this information to catalyze a pipeline of investments, the investor-focused, not-for-profit, Climate Bonds Initiative focuses on developing a liquid green bond market in order to facilitate the transition to a low carbon economy.

Similarly, in the loan market, the Loan Syndication & Trading Association, the Loan Market Association, and the Asia Pacific Loan Market Association, collectively issued the two highest profile loan guidance documents (and their recently published accompanying guidelines): the Green Loan Principles (GLPs) and the Sustainability Linked Loan Principles (SLLPs). The GLPs and SLLPs each provide four core components, all of which must be satisfied for a loan to be deemed a green loan or an ESG-linked loan. With the sustainability finance market currently remaining largely unregulated, these guidance documents are emerging as the de facto market standard.

One development in the region is the implementation of disclosure standards and indices spearheaded by local regulators and stock exchanges. For example, this past year, Mexico launched the S&P/BMV Total Mexico ESG Index, which uses a rules-based selection criterion based on relevant ESG principles. However, ESG reporting is still voluntary. In Argentina, the Buenos Aires Stock Exchange (BYMA) does not require a public company to submit or publish a sustainability report. Instead, in line with international practices, the BYMA has implemented various initiatives to promote good corporate governance and sustainability practices, such as a Sustainability Index with the IDB that serves to highlight leading ESG companies to investors. Brazil is requiring listed issuers to disclose socio-environmental information in their annual reports. The stated purpose is to encourage issuers to make consistent disclosures on social and environmental issues, and provide the market with comparative information, thereby dependably apprising investors of Brazil’s pertinent ESG information.

Many other countries in the region are developing sustainability standards and are looking to enhance the investment products in the space to further aid in economic development.

Overall, Latin America is actively creating many opportunities for ESG investment and we expect that governments and private sector actors will continue to promote ESG investment in the region.

‘Effective and transparent governance is an essential part of the business toolkit for companies that want to thrive in today’s rapidly evolving and competitive business environment.

‘Effective and transparent governance is an essential part of the business toolkit for companies that want to thrive in today’s rapidly evolving and competitive business environment.

Irwin Mitchell is determined to become a leading responsible business. We’re already on a journey to ensure that our environmental, social and governance values are embedded into our business and influence our relationships, strategies and aspirations. But to be truly successful, we need to proactively engage in conversation and collaboration; with our colleagues, with our clients, within our business and geographic communities, and, setting commercial competition aside, with our peers across the legal sector. In doing that, we believe our aspirations will be realised and we will lead as a responsible business. We’re delighted that so many in-house counsel contributed to this research, and I’d like to thank them for their time and for sharing their insights into the role of in-house in setting and supporting the ESG agenda within their businesses. We hope that you’ll find this research useful in plotting where you, your team and your business are on your own ESG journey, and where it will take you next.’

Irwin Mitchell is determined to become a leading responsible business. We’re already on a journey to ensure that our environmental, social and governance values are embedded into our business and influence our relationships, strategies and aspirations. But to be truly successful, we need to proactively engage in conversation and collaboration; with our colleagues, with our clients, within our business and geographic communities, and, setting commercial competition aside, with our peers across the legal sector. In doing that, we believe our aspirations will be realised and we will lead as a responsible business. We’re delighted that so many in-house counsel contributed to this research, and I’d like to thank them for their time and for sharing their insights into the role of in-house in setting and supporting the ESG agenda within their businesses. We hope that you’ll find this research useful in plotting where you, your team and your business are on your own ESG journey, and where it will take you next.’ ‘Although there is currently no global standard for ESG reporting, there is a huge range of legal reporting requirements for businesses. In the UK alone there is a wide variety of existing and incoming legislation that involves important elements of ESG reporting such as gender pay gap reporting and modern slavery statements. In addition, we believe that some of the confusion around current ESG reporting obligations has arisen from the fragmented reporting framework that places obligations on companies depending on their size (rules for large undertakings under section 172 and 414 Companies Act), whether they are listed (arising from the Disclosure Transparency Rules and UK Governance Code) and whether they are in the regulated financial services sector (Prospectus regulations, Disclosure Guidance and Transparency Rules and Market Abuse Regulations).

‘Although there is currently no global standard for ESG reporting, there is a huge range of legal reporting requirements for businesses. In the UK alone there is a wide variety of existing and incoming legislation that involves important elements of ESG reporting such as gender pay gap reporting and modern slavery statements. In addition, we believe that some of the confusion around current ESG reporting obligations has arisen from the fragmented reporting framework that places obligations on companies depending on their size (rules for large undertakings under section 172 and 414 Companies Act), whether they are listed (arising from the Disclosure Transparency Rules and UK Governance Code) and whether they are in the regulated financial services sector (Prospectus regulations, Disclosure Guidance and Transparency Rules and Market Abuse Regulations). ‘The in-house legal team’s role is to ‘help their business do “it” right’ – the “it” being sustainable, successful and compliant business.

‘The in-house legal team’s role is to ‘help their business do “it” right’ – the “it” being sustainable, successful and compliant business. ‘The G in ESG is becoming increasingly more important for businesses in the funds and investments space; aligning how you operate your own business with your external ESG messaging is crucial. The impetus for businesses to build ESG into their investment decision making is driven partly by the introduction of new regulation and partly by the growing appetite and demand from stakeholders, whether they be shareholders, investors or customers. Post Brexit the UK has not ‘onshored’ the EU Sustainable Finance Disclosure Regulation (SFDR) into UK domestic law, opting instead to make disclosures that are aligned with the Task Force on Climate related Financial Disclosures (TCFD) fully mandatory by 2025 but there is a general view that it still has a number of indirect/practical implications for funds and investment related businesses in the UK given the UK’s Green Finance Strategy and the fact that ESG considerations will become integral to future EU trade deals and the ability to attract international capital.’

‘The G in ESG is becoming increasingly more important for businesses in the funds and investments space; aligning how you operate your own business with your external ESG messaging is crucial. The impetus for businesses to build ESG into their investment decision making is driven partly by the introduction of new regulation and partly by the growing appetite and demand from stakeholders, whether they be shareholders, investors or customers. Post Brexit the UK has not ‘onshored’ the EU Sustainable Finance Disclosure Regulation (SFDR) into UK domestic law, opting instead to make disclosures that are aligned with the Task Force on Climate related Financial Disclosures (TCFD) fully mandatory by 2025 but there is a general view that it still has a number of indirect/practical implications for funds and investment related businesses in the UK given the UK’s Green Finance Strategy and the fact that ESG considerations will become integral to future EU trade deals and the ability to attract international capital.’

‘For two weeks in autumn 2021, the eyes of the world will be on Glasgow as it plays host to the UN Climate Change Conference (COP26). These talks will bring together heads of state, climate experts, leading businesses and campaigners to discuss a coordinated action plan to tackle climate change. Top of the agenda will be the urgency around net-zero commitments and the need for business transparency and accountability.

‘For two weeks in autumn 2021, the eyes of the world will be on Glasgow as it plays host to the UN Climate Change Conference (COP26). These talks will bring together heads of state, climate experts, leading businesses and campaigners to discuss a coordinated action plan to tackle climate change. Top of the agenda will be the urgency around net-zero commitments and the need for business transparency and accountability. ‘Diversity and inclusion, as part of a wider ESG agenda, provides clear opportunities for those businesses ready to truly embrace it. D&I cannot be seen as a job for HR; as something that should be monitored and reported on but then forgotten. A strategic approach that is embraced by all leaders including GCs must be taken to embracing D&I on a day-to-day organisational basis. We have seen huge leaps forward by businesses who are paving the way including for example the creation of shadow boards or “reverse” mentoring programmes. These businesses are already reaping the rewards of these programmes and those businesses who have not started to properly engage with D&I as an agenda item risk falling behind.’

‘Diversity and inclusion, as part of a wider ESG agenda, provides clear opportunities for those businesses ready to truly embrace it. D&I cannot be seen as a job for HR; as something that should be monitored and reported on but then forgotten. A strategic approach that is embraced by all leaders including GCs must be taken to embracing D&I on a day-to-day organisational basis. We have seen huge leaps forward by businesses who are paving the way including for example the creation of shadow boards or “reverse” mentoring programmes. These businesses are already reaping the rewards of these programmes and those businesses who have not started to properly engage with D&I as an agenda item risk falling behind.’