Regardless of the fact that Ecuador’s economy is the eighth largest in Latin America and the Caribbean (among 33 countries), Ecuador has amazing potential of business activities in the mining, energy, tourism and agriculture industries. With large natural mineral reserves (in gold, cooper and iron), amazing conditions for the development of energy projects, especially photovoltaic and hydroelectric energy, incredible tourism locations such as the Galapagos Islands, beautiful highlands, and considered to be one of the most bio-diverse countries in the world, Ecuador is also one of the top exporters worldwide of bananas, shrimp, flowers and cacao.

Due to all these interesting factors and many others like a dollarized economy, the government’s current policy has been focused in promoting attractive conditions for foreign investors and working on improving the benefits that were already granted in the Organic Code of Production, Commerce and Investment (COPCI) published in December 2010, but had little or none effect during the previous government (aligned to Hugo Chavez ideology).

The Law of Productive Development, Attraction of Investment, Employment Generation and Fiscal Stability (Investment Law) enacted in august 2018, offers to investors the possibility of obtaining interesting benefits such as: tax exemptions (income tax and currency remittance tax), reduction of custom tariffs, legal stability and entering into arbitration agreements while entering into Investment Agreements with the State, which has given law firms a new scope of work that involves project finance, tax, regulatory matters and contracts.

Furthermore, Ecuador offers investors a dollarized economy and a much more transparent State which has promoted transparency and the implementation of ISO 37001 anti-bribery among its government institutions and companies. These benefits have caused almost a 130% increase in foreign direct investment in comparison to the former government as per studies of the Central Bank of Ecuador.

However, despite the new foreign investors that came in different industries due the favorable conditions of the Investment Law and the effort of the current government to solve the extremely high debt left by the former government (which in addition to other matters caused a division among the elected political party, some in favor of the previous government and some in favor of the actual government), the economy of Ecuador was affected again by a combination of different factors. These are the social unrest events that occurred not only in the country but also in the Latin American region around October 2019, followed by the oil crisis (price-drop), the damages in the local oil pipelines due to massive landslides and COVID-19.

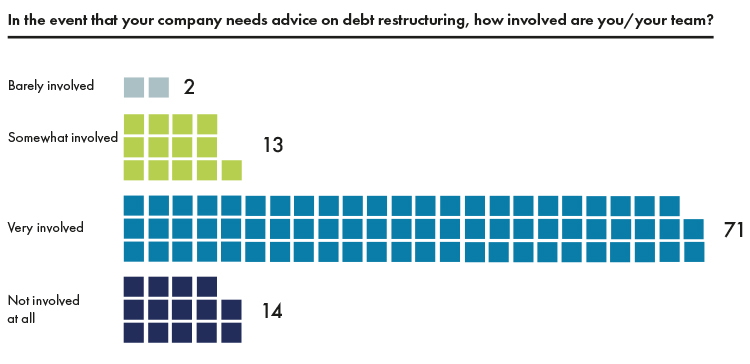

COVID-19 impact not only revealed the deficit in the country’s health system but also caused the lockdown of the country and the suspension of most economic activities for a couple of weeks. As a consequence, certain small businesses have faced bankruptcy or many other, have had to reduce their production capacity and employment force, generating many opportunities for law firms in debt restructuring, ADR and labor advice, that had to innovate their services to provide legal assistance while working from home.

In addition, Ecuador has upcoming presidential elections on February 2021, and the political scenario is uncertain due to the fact that most of the high public official (President, Vice President and some ministries) of the former government have been prosecuted in relation to corruption allegations, and there is low probability that they can run for a public position. As such, after 14 years of having the same political party in government, there is a high probability of having a different political party achieving the presidency.

Some of the key aspects take into account while deciding to invest in Ecuador are the following:

Key Indicators for 2020 and forecast

Current Business Environment

Tax Regulation

Bellow a brief description of the main taxes applicable to commercial activities in Ecuador:

a) Income Tax

Income tax taxes the rent obtained by persons and local and foreign companies. Under the Ecuadorian law, income refers to:

Income from Ecuadorian source obtained free of charge of from work or capital.

Income obtained from abroad by persons domiciled in Ecuador or by Ecuadorian companies.

The tax basis is the total taxable income, less returns, discounts, costs and expenses deductible and attributable to such income. In general terms, the rate for companies is of 25%.

b) Value Added Tax

Tax on the value of transfer of ownership or import of goods, services, copyrights, industrial property and related rights. A 12% rate is applied over the price of goods and services. Some exceptions may apply to certain goods and services that will be taxed with a 0% rate.

c) Currency Remittance Tax (ISD)

The Currency Remittance Tax (ISD) taxes transfers in cash, through money orders, bank transfers, shipment, withdrawals or any payment of any kind, of currencies sent abroad, with the exception of an account clearing made with or without the intermediation of financial institutions.

The tax rate of 5% is applied over the value of the currency transfer. This tax is declared and paid by the financial institution by which the financial operation is carried out.

d) Capital Gains Tax or Property Transfer Tax

The tax rate for Capital Gains Tax and Property Transfer Tax ranges from 2% to 10%.

Labor – Profit sharing

15% of the net earnings of a company are distributed to all employees in the payroll. It can also apply to employees of companies that provide the company complementary services such as catering, security, cleaning and courier services. From the 15%, 10% is divided and distributed to all employees. The remaining 5% is distributed in accordance with the employee’s household.

Profit Sharing in mining, oil, and hydroelectric companies: as an exception to the general profit sharing rule, that the 15% of the annual profit must be distributed to all employees, in the case of mining, oil and hydroelectric companies it is only distributed 3% to all employees in the payroll, and 12% is distributed to the state.

Public Private Partnerships

The government has promoted Public Private Partnerships (PPP) which can be established for the provision of goods, building infrastructure, or services. All terms and conditions of PPPs are set out in a contract that must be signed with the public entity.

The PPPs have, among others that might be agreed upon the contractual parties, the following incentives:

a) Legal stability.

b) Income tax Exemption: Income tax exemption for ten years in projects in the prioritized sectors determined by an inter-institutional committee, period which starts from the first fiscal year in which the company generates operating income.

c) Currency Tax Remittance Exemption: All companies that participate in an PPP will be exonerated from ISD in the following scenarios:

- In the importation of goods for the execution of the public project, whatever the import regime used.

- In the acquisition of services for the execution of the public project.

- The payments made by the company to the financiers of the public project, including capital, interest and commissions, provided that the agreed interest rate does not exceed the reference rate at the date of registration of the credit. The benefit extends to subordinate loans, provided that the borrowing company is not in a situation of undercapitalization in accordance with the general regime.

- The payments made by the company for distribution of dividends or profits to its beneficiaries, notwithstanding where they have their fiscal domicile.

- Payments made by any person or company due to the acquisition of shares, rights or participations of the structured company for the execution of a public project in the PPPs modality or for transactions that fall on securities representing obligations issued for the financing of the public project.

d) Reduction of tariffs: Customs tariffs that are related to the PPP projects will also be exonerated

e) International or domestic arbitration agreements

The incentives mentioned above may be enjoyed for the term agreed upon in the contract, with the exception of the income tax exemption, which can only be 10 years.

Investment Contracts

The Investment Law and COPCI benefits are directed to those new investments (either made by foreign or local investors) that meet the criteria of new productive investments in prioritized sectors of the economy that increases production and generates new employment.

The benefits granted by the government will depend on the investment project, its location, its industry, whether is a new company or an existing one, amongst other criteria, as shown bellow:

a) Total or partial income tax reduction from 8 to 15 years.

b) Currency Remittance Tax (“ISD”) exemption for the payment of imported machinery and raw materials, and for the payment of profits to foreign shareholders.

c) Tax stability for up to 15 years of the current applicable income tax rate. This provision does not provide stability for municipal, customs nor VAT Taxes.

d) Temporary exemption of custom tariff.

e) International or domestic arbitration is available for investors.

Initially, the aforementioned benefits apply for those investments made up to August 2020, but the President has recently extended the benefit for 2 years more, until 2022.