Argus Partners | View firm profile

Non-fungible tokens or NFTs, as they are more popularly known, are digital collectible tokens, unique in form (hence non-fungible) which are verified and secured by a blockchain. NFTs provide and represent the authenticity of origin of an underlying work/item, its ownership, scarcity as well as its permanence.

Further, NFTs are cryptocurrency ‘tokens’, implying that the existence of an NFT leverages an existing cryptocurrency’s blockchain. A large proportion of the NFTs are created and exist on ‘Ethereum’, ‘Polygon’ and ‘WAX’ blockchains.

Most NFT transactions take place on internet platforms through smart contracts. A smart contract is a self-executing contract in which the terms and conditions of the buyer-seller agreement are directly inscribed into lines of code. The code and the agreement contained within it are dispersed and decentralised over a blockchain network. Transactions are easily traceable and irreversible, and the code controls the execution.

The non-fungibility or the uniqueness of NFTs prevents counterfeits of the underlying assets. As a general rule, non-fungible items aren’t freely exchangeable or replaceable by similar items. One cannot freely exchange NFTs or replace one NFT with another as each NFT is verified and secured independently on the blockchain and remains on the blockchain forever for any person to verify and authenticate. Though NFTs have been around for a while, the boom in NFTs came about in the year 2017, when a Canadian gaming company, Dapper Labs created a blockchain based game named ‘Crypto Kitties’, wherein people could purchase, collect, breed, and sell virtual cats over the internet. The trading community benefitted financially due to the non-fungible nature of the collectible traded. This paved the way for the expansion and recognition of NFTs on a larger scale in the financial and investment market.

A few examples of NFTs issued / sold recently are as follows:

- ‘This Changed Everything’ – An NFT featuring the source code of one of the early versions of the World Wide Web (www) was sold for USD 5,400,000 (United States Dollars five million four hundred thousand) through an online auction held on Sothebys’ website. Additionally, this NFT gave the owner of the NFT, a letter written by Sir Timothy John Berners-Lee, the inventor of the World Wide Web, a digital poster of the code written by him, and time-stamped documents recording the history of the World Wide Web in its initial days.

- ‘Madhushala NFTs’- An NFT collection was recently sold by Bollywood superstar Amitabh Bachchan, this included his father, the late Harivansh Rai Bachchan’s famous poem, Madhushala recited in Amitabh Bachchan’s voice, for a sum of Rs. 7,18,00,000 (Rupees seven crore eighteen lac);

- ‘Huddles membership NFT’- NBA player Michael Jordan recently launched an NFT collection which will give buyers access to a new platform called ‘Huddles’, that enables fans to hold question and answer sessions, buy merchandise and have access to a ‘Discord’ chat among other things with athletes.

Industry Jargon

- Minting: Minting denotes the action that brings an item into existence on the blockchain, and costs “gas” to do so (“Minting”). Minting using the NFT Marketplace only occurs when necessary, i.e. (i) when you transfer an item to another account; and (ii) when someone buys an item from you.

- Gas Fees: The term “Gas Fee” refers to the cost or payment required to carry out a transaction or execute a contract on the Ethereum blockchain. Gas Fees is an essential incentive in the form of a cryptocurrency that is given to miners for validating transactions on a blockchain. The Gas Fee is usually collected by the NFT Marketplace from the creator and passed on to the miners. Gas Fees is an important levy as it helps miners prioritise the validation of certain transactions over the others when there are multiple transactions queued up for validation.

NFTs and cryptocurrencies

NFTs are functionally similar to cryptocurrencies, except for the limit on Error! Reference source not found.. Theoretically millions of cryptocurrencies can be minted, but NFTs, in order to remain non-fungible, are required to have a limited supply of only 1 (one) token per NFT. However, there exists a fairly common exception to the rule of fungibility which is observed for a number of multi-token NFTs wherein at the time of creation of the NFT, minting additional copies is permitted, subject to a specified limit. [1]

Purpose of an NFT

In the limited time that NFTs have existed, NFTs have served varying purposes including promotion of art (digital or otherwise) by way of creating a marketplace with demand for ownership of artworks in a digital and thus globalized and accessible format.

Generally, an NFT serves the following purposes:

- Preservation of an artwork;

- Store of value;

- Serve a parallel new-age collector’s market;

- Marketing and recognition of an artist; and

- Bragging rights for the owner.

Creating and Minting NFTs

Issuing an NFT for an existing artwork is quite simple. One needs to set up a cryptocurrency wallet (“Wallet”) and open an account on an NFT marketplace. The artwork, if it is digital, can be uploaded to the NFT marketplace and a token i.e., the NFT, can be generated.

While the process seems cumbersome and may require a lot of handholding, a large number of dedicated NFT marketplaces have simplified and made the creation, issuance and marketing of NFTs quite intuitive.

Though non-digital art can also underly an NFT, it is most common to issue NFTs for digital art, which could be anything from an image to a music video. The artwork can be of any size and resolution, though most NFT Marketplaces usually enforce an upper limit on the file size that can be uploaded onto the NFT Marketplace’s online platform. Opensea, Rarible, SuperRare and Nifty Gateway are some of the most common NFT Marketplaces where NFTs can be created, listed and traded. As for Wallets, Ethereum wallets are among the most common, since as they allow the user to hold Ethereum (abbreviated as ETH) cryptocurrency, Error! Reference source not found. tokens [2] as well as NFTs. Metamask, Coinbase, Bitski and Torus are some popular service providers which provide easy to use Ethereum based Wallets to the users.

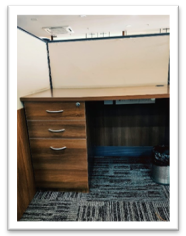

In order to understand the practical processes and challenges that a lay person may face in minting, marketing and selling NFTs, Anurag, Aryan and Aishwarya (“The AAA Team”) created and minted their own NFTs based on the two amateur photographs shown below (a) Bombay Through a Fence; and (b) Pandemic Office Desk.

Bombay Through a Fence

Pandemic Office Desk

The AAA Team opted for Opensea, a very popular NFT marketplace which allows a user to upload the underlying content for an NFT, up to a maximum file size of 100 (one hundred) Megabytes (“MB”). Opensea also has restrictions on the type of file that can be uploaded, as explained below.

Opensea is one of the most popular NFT marketplaces and setting up an account with Opensea entails the following steps:

- Setting up a cryptocurrency Wallet – Setting up an Opensea account for NFT trading, minting, and listing requires creating and linking of a Wallet. The AAA Team opted to set up a Coinbase Wallet, for which the process was as follows:

- Once the AAA Team downloaded the Wallet and added it as an extension to their web browser, they received a screen prompt to pick a username, after which, a universal wallet address (“wallet address”) was assigned to them. The username or the wallet address can be used to send and receive digital assets. The username/wallet address assigned to each Wallet can be used to search the Wallet, upon which cryptocurrency, NFTs and tokens may be transferred. A wallet address looks like the following – “0x78F612C7e861xxxxxxxxxxxxxxxxxxxx986fD6C4”

- After a username had been successfully created, a prompt for setting a 12-word recovery phrase (“Recovery Phrase”) appeared on the screen. This Recovery Phrase is colloquially referred to as a backup phrase and is the key to one’s Wallet. It must be kept completely secure as this is the sole method of recovering one’s Wallet, if one loses their password or migrates from one Wallet platform to another. It must be noted that if any third party gets access to one’s Recovery Phrase, they can import such user’s Wallet into their browser and transfer the underlying digital assets. Thus, it is important to not reveal one’s Recovery Phrase to anyone at any time. It must also be noted that the order of occurrence of each word in the Recovery Phrase is vital and the Recovery Phrase should be saved exactly as displayed on the Wallet.

- The platform prompted the AAA Team to create a password, after the Recovery Phrase had been successfully generated. This password may be used to unlock the Wallet after a pre-set duration of inactivity on one’s computer.

- It is noteworthy that Wallets allow interoperability, therefore allowing a user to shift from one Wallet to another simply using their Recovery Phrase.

- Once the Wallet was created, it could be linked to the AAA Team’s account on Opensea, the AAA Team’s chosen NFT marketplace. Upon linking, the AAA Team could list, buy and sell NFTs through the NFT marketplace.

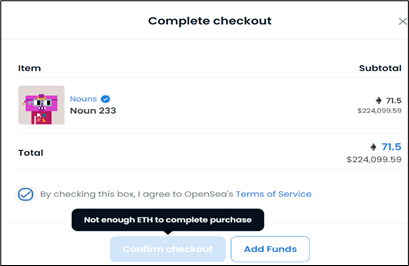

Illustration 1: Buying an NFT on Opensea.

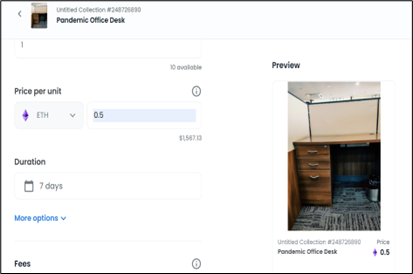

Illustration 2: Selling an NFT on Opensea.

- Setting up an account on the NFT marketplace – Opensea is one of the largest NFT marketplaces and is also considered to be one of the most user-friendly. While creating NFTs on Opensea a user is not required to pay any Error! Reference source not found.. However, a Gas Fee might be required at the time of listing of an NFT for sale, especially on the Ethereum blockchain. The following steps are required to be followed for setting up an account with Opensea

- A user needs to click on the ‘Create’ button on the home page of Opensea’s website. On the next page, they will receive a prompt to connect/sign-in with their Wallet. On selecting the same, the Wallet shall open up as an extension window on the browser.

- This extension window with the Wallet will prompt the user to sign in with their password. Upon entering the correct Wallet password, the Opensea account shall automatically activate.

- Once the account has been activated, a user can add personal details like a profile picture, banner image etc. The user will then receive a prompt to associate an email account with their Opensea profile. Opensea would require the user to verify the email before proceeding. Pertinently this is the only instance at which Opensea collects personal / personally identifiable data.

Creating the NFT

Opensea allows users to create NFTs of various formats including images, videos, audio as well as three-dimensional models up to 100 (one hundred) MB in size. Opensea supports multiple formats to convert into NFTs, including JPG, PNG, GIF, SVG, MP4, MP3, WAV, among others.

To create an NFT, any piece of art including digital artworks, music audios, videos, pictures of objects, places and physical artworks can all be uploaded onto a designated field on the Opensea platform. After the relevant artwork has been uploaded onto the designated field, the same is required to be named, following which the user can select a preferred blockchain for hosting the NFT.

The Opensea platform provides for hosting of an NFT on ‘Ethereum’ and ‘Polygon’ blockchains. Upon choosing the blockchain, Opensea provides the creator with the option to choose the number of copies of the NFTs that the user wants to be created.

It is pertinent to mention here that in case of Opensea, while multiple copies can be created if the NFT is hosted on the Polygon blockchain, however only 1 (one) copy can be created on the Ethereum blockchain.

Once the required number of copies of the NFT to be created is selected, the user can insert a description for the NFT. This is only an optional feature. After filling in the said information, the user can select the create tab and the preferred number of NFTs will be created and added to the user’s profile on Opensea.

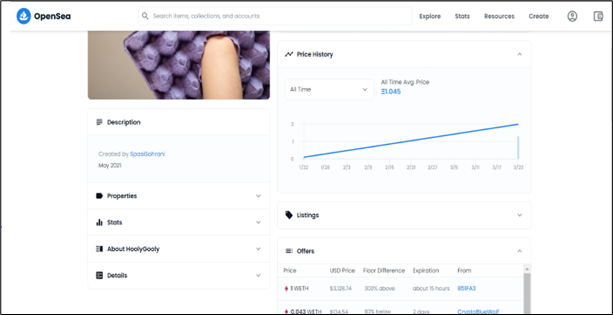

Tracking the ownership of an NFT

Since NFTs are integrated on a blockchain, tracking the ownership of NFTs and transactions involving them, is simple. Every NFT has an owner, creator, transaction history and a listed price, and all of such information is easily verifiable. An NFT listed on OpenSea can be easily tracked by navigating to the ‘Details’ section of a displayed NFT. Additionally, all transfers of the NFT and even offers made for sale of the NFT, can be viewed on OpenSea. The information that may be accessed by OpenSea users includes a hyperlinked contract address, token ID, token standard, relevant blockchain as well as metadata pertaining to each NFT listed on Opensea.

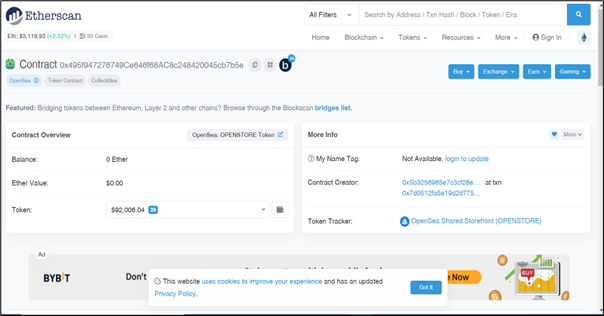

It is noteworthy that the hyperlinked contract address of the NFT redirects a user to a third-party website, ‘Etherscan’. Etherscan is analogous to a search engine for the Ethereum blockchain that lets users search, confirm and validate transactions (including NFT transactions) on the Ethereum blockchain.

Instead of using an NFT marketplace, one can also track the ownership and transaction history of an NFT by entering the relevant contract address in the search box on Etherscan website.

Illustration 3: Tracking an NFT through OpenSea

Illustration 4: Tracking an NFT through Etherscan

NFTs and the Law

NFTs have emerged as an important asset class worldwide but there still exist major concerns around their real economic value and impact on financial markets. Further, since NFTs are traded using cryptocurrencies and the Indian government is yet to formally declare its final position on the legality of cryptocurrencies, the future of NFTs in India can only be described as ‘uncertain’. If cryptocurrencies forming the consideration for the trading of NFTs are held to be illegal under law, the consideration for the underlying smart contract itself becomes illegal, which essentially renders the smart contract void.

Other than the issues arising out of the government’s position on cryptocurrencies and NFTs, the following legal issues involving NFTs are also relevant.

Nature of NFTs

Can it be said that NFTs are a form of cryptocurrency? If so, any ban on cryptocurrencies would affect NFTs as well. Section 3 of the Banning of Cryptocurrency & Regulation of Official Digital Currency Bill, 2019 (“Crypto Bill”) which was recently introduced in Parliament, but wasn’t passed, essentially prohibits mining, generating, holding, selling, dealing in, issuing, transferring, disposing of or using cryptocurrency in India. The Crypto Bill defines a cryptocurrency to include any information, code, number or token, generated through cryptographic means or otherwise, which has a digital representation of value and has utility in a business activity, or acts as a store of value, or a unit of account. It could be argued that NFTs provide a digital representation of value and therefore could fall under the ambit of cryptocurrency under this Crypto Bill.

Can it be said that NFTs are derivatives? Section 2(ac) of the Securities Contracts (Regulation) Act, 1956 (“SCRA”) defines a derivative as follows,

“Section 2(ac): derivative includes—

(A) a security derived from a debt instrument, share, loan, whether secured or unsecured, risk instrument or contract for differences or any other form of security;

(B) a contract which derives its value from the prices, or index of prices, of underlying securities;”

However, Section 18A of the SCRA stipulates that contracts in derivatives shall be legal only if they are traded on recognised stock exchange. Hence, if NFTs were to be classified as derivatives, then any contract in such derivatives would be deemed illegal because the marketplaces on which they are traded currently are not recognized by under the applicable law as recognised stock exchanges. If it were to be classified as derivatives, then the current platforms and marketplaces trading in NFTs would have to apply to the government to be classified as recognised stock exchanges.

Taxation of NFTs

Since the nature of NFTs is unclear, the taxation of the same remains uncertain as well. “Goods” are defined under Section 2(52) of the Central Goods and Services Tax Act, 2017 (“GST Act”) as moveable property other than money and securities. “Services” are defined under Section 2(102) of GST Act to include anything other than goods. Therefore, NFTs could be made subject to taxation under goods and services tax (GST) regime as either goods or services.

Under the Finance Act, 2020, if the marketplaces engaged in NFT trading fall under the definition of an e-commerce operator, then an equalisation levy of 2% (two percent) might be charged on either the value of the NFT or the Gas Fees charged by the marketplaces, or even both.

However, in February 2022 during her budget address on the floor of the Lok Sabha, Hon’ble Finance Minister Ms. Nirmala Sitharaman, announced that income earned from transacting in digital assets will attract a capital gains tax of 30% (thirty percent) and tax deducted at source of 1% (one percent).

Does this mean, that trading in cryptocurrencies and buying NFTs were legalized or recognized by law? Well, crypto-currencies were not illegal to start with. Even during the period from April 2018 to March 2020 when the RBI prohibited regulated entities from dealing in crypto-currencies or providing services for those doing so, crypto-currencies were not outright illegal. Theoretically, the government is entitled to tax even ill-gotten gains. On a practical note, the crypto tax indicates the Indian government is likely to regulate crypto-currencies instead of banning them outright, something that will become clear once the ‘Cryptocurrency and Regulation of Official Digital Currency Bill’ is tabled in Parliament.

Intellectual Property Rights and NFTs

As discussed above, NFTs are digital copies or tokens of an underlying artwork, which is usually digital. However, ownership of an NFT does not necessarily translate into ownership of the underlying artwork represented by the NFT. When one buys an NFT, one may acquire the right to use and display the NFT, which is a copy of the underlying artwork. However, the buyer would not have the right to distribute, publish or sell copies of the NFT’s underlying content or create derivative works out of it, unless the underlying smart contract expressly provides for the same.

An NFT holder, therefore, will be treated as the owner of the copyrighted work only if the rights are assigned to him by way of the underlying smart contract. Therefore, all rights of the NFT holder in relation to the work are governed by the underlying smart contract. As a collector or a purchaser of an NFT, it is important to be vigilant of one’s actions in respect of the purchased NFT to ensure that there is no violation of the rights of the creator. Further, it is important to check the underlying smart contract and the terms assigned to the NFT bought on a marketplace.

Since the artworks underlying the NFTs created by the AAA Team are digital photographs (whether or not they possess artistic quality is up to our discerning readers), they fall under the definition of an “artistic work” under Section 2(c) of the Copyright Act, 1957. Since the AAA Team are the authors of the work, the copyright in the same vests in the AAA Team by virtue of Section 17 of the Copyright Act, 1957.

When creating an NFT, it would be ideal if the underlying artwork is original. This is because the protections offered to copyright holders under Section 14 of the Copyright Act, 1957 may prevent the reproduction of somebody else’s work for creation of an NFT. However, enforcing one’s copyright against a seller of an NFT which violates one’s copyright might be difficult due to the decentralised nature of blockchain transactions. An NFT is linked to a Wallet address and ascertaining the owner of a Wallet may prove to be difficult owing to the anonymity of Wallets and NFT marketplace accounts (Opensea, for example, only collects the users’ email addresses and no other personally identifiable information).

Section 19(1) of the Copyright Act, 1957 provides that an assignment of a copyright shall be valid only if the same is in writing and signed by the owner of such copyright or a person so authorized by them. As per Section 4 of the Information Technology Act, 2000, where any law provides that information or any other matter shall be in writing or in the typewritten or printed form, then, notwithstanding anything contained in such law, such requirement shall be deemed to have been satisfied if such information or matter is (a) rendered or made available in an electronic form and (b) accessible so as to be usable for a subsequent reference. Therefore, assignment of a copyright may be effected through a smart contract, if the parties so agree and the terms of such contract expressly provide for the assignment.

Can an NFT be trademarked independent of the trademark over the underlying asset? This seems to be unlikely, since the Trademarks Act, 1999 requires a mark to be capable of distinguishing the goods or services of one person from another. An individual NFT cannot be registered as a trademark, though the brand covering a collection of NFTs may be trademarked. For example, an apparel brand may also be trademarked to market its digital goods including collectibles, artworks, or other digital media. Such a trademark application has been filed by Nike to introduce virtual goods, retail stores featuring virtual goods and non-downloadable virtual goods in virtual environments. Similar applications have also been filed by McDonald’s which currently awaits approval. While the question of whether trademark registrations will be granted depends on the decision of the US Patents and Trademarks Office, it is safe to say that a trademark may be filed for a brand creating and selling NFTs to ensure authenticity and marketability.

Another important question which arises in case of NFTs and trademarks is whether NFTs can exploit the trademarks of an existing brand. A few disputes have recently been filed before the US courts wherein, NFTs have been alleged to breach the trademarks of a third party. The case of Hermès International v. Mason Rothschild [3] is pertinent. Hermès, a French luxury design house is the creator of and holds trademark to the Birkin, an iconic handbag named after the actress Jane Birkin. Hermès filed a lawsuit in January 2022, against one Mason Rothschild, a Los Angeles-based interdisciplinary artist and designer, who created a collection of 100 (one hundred) MetaBirkins which are images showing furry renditions of the Birkin Bag and sold them through platforms like OpenSea. The MetaBirkins are also linked to Rothschild’s social media handles titled @MetaBirkins on instagram, twitter etc. Hermès International and Hermès of Paris, Inc. (collectively “Hermès” henceforth) filed a detailed complaint alleging that Mason Rothschild has engaged in trademark infringement, dilution and unfair competition. Hermès has claimed that Rothschild’s addition of the generic term “meta” is not sufficient to distinguish it from Hermès’ trademarks. Though Rothschild has not yet appeared for the lawsuit, except for a filing dated February 9, 2022, entailing a motion to dismiss the proceedings, he has penned an open letter to Hermès, contending his right to freedom of expression granted under the first amendment to the Constitution of the United States as a defence.

While the opinion of the court remains to be seen, the case raises notable issues for brand owners, especially those looking to venture into the NFT space and bring out their digital assets.

Nike Inc. v. StockX LLC [4]

In February this year, Nike filed a complaint against a sneaker resale marketplace called StockX LLC) (“StockX”) alleging that the NFTs created by StockX use its trademarks without approval and sells them at inflated prices.

StockX launched its own series of NFTs linked with physical Nike products assuring that the so-called Vault NFTs can be redeemed or traded instantly as digital goods by the owner of the physical items. With respect to this issuance of NFTs by StockX, Nike alleges that the said crypto assets result in trademark infringement, false designation of origin and trademark dilution.

The core issue is whether the said NFT issuance is an extension of its reselling process (analogous to placing Nike products on StockX’s shelves physically) or if the same would constitute a product itself. The court’s opinion in this matter remains to be seen.

A growing line-up of cases involving alleged infringement of trademarks by issuing NFTs only proves that such alleged breaches are not one-off instances and there is a pressing need for courts/legislatures across the world to settle the law surrounding NFTs and their intersection with trademark law.

In a stark contrast to the Rothschild dispute, recently, the Raja Ravi Varma Heritage Foundation, a foundation set up to promote and preserve the artistic legacy of the great artist Raja Ravi Varma, announced that 2 (two) of the renowned artist’s paintings were going to be auctioned off on ‘RtistiQ’, a Singapore-based online art marketplace that also dabbles in NFT auctions (colloquially known as NFT Drops). ‘The Coquette’ and ‘Reclining Nair Lady’ are the first of the artist’s creations to be tokenised and launched online. Here, the foundation themselves have granted permission and initiated the conversion and launch of the work into an NFT, making it available on the metaverse. This allowed the foundation to collect the proceeds of the sale themselves and create a legitimatized token of the works before the space was infiltrated by variants or derivations of the artist’s work. The Rothschild dispute arises from the fact that the brand lost out on the chance to enter the metaverse, to an artist who in turn raked in money off of the luxury brand’s most iconic product. At the end of the day, it was about an opportunity that was not effectively monetized by the brand and a rare case of a digital artist turning into a competitor.

In a hypothetical scenario, if we had taken pictures of an M.F. Hussain painting instead of the amateur photographs, we would find ourselves in hot water. Why? Because it would amount to copyright infringement. As per Section 14 of the Copyright Act, 1957, the copyright in an artistic work includes the rights listed under Section 14(c)(i), (ii) and (iii), namely, the rights (a) to reproduce the work in any material form; (b) to communicate the work to the public; and (c) to issue copies of the work to the public not being copies already in circulation. Taking a photograph of a painting and issuing NFTs for sale/purchase of such painting would infringe on the IP rights of the copyright owner of such painting.

Concluding Remarks

Despite the various legal uncertainties plaguing NFTs, the AAA Team found the process of issuing NFTs to be very simple and straightforward, thanks to the efficiency of the enterprises operating NFT marketplaces and cryptocurrency wallets. It appears that NFTs are here to stay, though the path ahead is bumpy and uneven. Going by global trends in terms of technological advances and innovation, it is only a matter of time before all legal and regulatory hurdles relating to NFTs are ironed out and NFTs are treated like any other asset type or class of investments.

This paper has been written by Vinod Joseph (Partner), Anurag Prasad, Rabia Rahim, Aishwarya Manjooran and Aryan Mohindroo (Associates).

DISCLAIMER

This document is merely intended as an update and is merely for informational purposes. This document should not be construed as a legal opinion. No person should rely on the contents of this document without first obtaining advice from a qualified professional person. This document is contributed on the understanding that the Firm, its employees and consultants are not responsible for the results of any actions taken on the basis of information in this document, or for any error in or omission from this document. Further, the Firm, its employees and consultants, expressly disclaim all and any liability and responsibility to any person who reads this document in respect of anything, and of the consequences of anything, done or omitted to be done by such person in reliance, whether wholly or partially, upon the whole or any part of the content of this document. Without limiting the generality of the above, no author, consultant or the Firm shall have any responsibility for any act or omission of any other author, consultant or the Firm. This document does not and is not intended to constitute solicitation, invitation, advertisement or inducement of any sort whatsoever from us or any of our members to solicit any work, in any manner, whether directly or indirectly.

You can send us your comments at:

Mumbai I Delhi I Bengaluru I Kolkata

www.argus-p.com

[1] Matt Fortnow & QuHarrison Terry, The NFT Handbook: How to Create, Sell and Buy Non-Fungible Tokens (Wiley, 2021).

[2] ERC20 is one of most significant standard for ethereum tokens. It refers to a scripting standard used within the Ethereum blockchain, that sets out a number of rules and actions that an Ethereum token or smart contract must carry out to implement the contract. ERC stands for “Ethereum Request for Comment”.

[3] Case number 1:2022cv00384, US District Court for the Southern District of New York, accessible here.

[4] Case No. 1:22cv00983, US District Court for the Southern District of New York, accessible here