V&T Law Firm | View firm profile

Author: Su Yuqiang Partner [email protected]

1. The Legal Due

Diligence Conducted by Acquirer

In a cross-border

M&A transaction, the legal due diligence conducted by experienced attorneys

for Acquirer towards Target Company is essential. It is a way for Acquirer to

take a full look of Target Company and detect minor defects or risks beneath

the surface of Target Company. To conduct legal due diligence requires the

capabilities to sense the legal and commercial defects or risks of Target

Company from attorneys.

Therefore, there are several essential aspects in the due diligence worth the

attention:

(1) The business scope

of Target Company

On the top of the whole due

diligence, the investigation of business scope of Target Company is the first

priority. The reason to do so is that certain business scope might require

permission or qualification issued by Competent Authorities under PRC laws and

regulations. In the event that the business scope of Target Company falls into

the business scope that requires permission or qualification from Competent

Authorities, in the due diligence, attorneys should verify whether Target

Company has obtained such permission or qualification issued by Competent

Authorities. Furthermore, if Target Company is a Foreign Invested Entity

(“FIE”), attorneys should pay more attention to whether business scope of

Target Company matches any business in Special Administrative Measures

(Negative List) for Foreign Investment Access (2019 Edition (“Negative List 2019”). If

the business scope of Target Company falls in Negative List 2019, the certain

business scope requires the controlling party of the business would be a local

Chinese corporate or such certain business would be prohibited from FIE.

(2) The

debts or liabilities lie in the Selling Equity

There are two forms of transactions

through M&A, the transfer of assets and transfer of equity. What we discuss

here is transfer of equity through M&A, for it is the most popular way to

settle the deal. Though the transfer of assets is safer and clean, it is also

more complicated, especially when it relates to real estates, therefore, most

of M&A transactions are done by the transfer of equity. However, compared

with the transfer of assets, transfer of equity may cause problems. The key

problem of transfer of equity would be the debts or liabilities in the equity,

especially the potential debts or liabilities. Therefore, the legal due

diligence conducted by experienced attorneys would be highly necessary for

finding out those debts or liabilities lie in the transferring equity.

(3) Potential and existing lawsuits

or arbitrations against Target Company

The lawsuits which have been issued

verdicts from courts could be verified via China Judgment Online website if

Target Company is a PRC legal entity. However, it is difficult to verify

potential or ongoing lawsuits and arbitrations of Target Company for attorneys.

The potential or ongoing lawsuits and arbitrations rely on the self-disclosure of

Target Company and Selling Party, but in order to avoid any potential or

ongoing lawsuits and arbitrations that might bring loss to Target Company, we

could arrange warrants or representations from selling party in SPA in terms of

selling party’s false disclosure of any lawsuits and arbitrations which bring

loss to Target Company and eventually harm the Acquirer, all such loss shall be

borne by the Selling Party.

Sure, there will be other issues

should be viewed in due diligence phrase. Above mentioned three issues are the

ones we believe important and essential for Acquirer’s attention.

2. The Share Purchase Agreement

(“SPA”)

(1) The Parties to enter into the SPA

In a cross-border M&A

transaction, at least one of the Parties to enter into the SPA is a foreign

legal entity. Our team used to help a client to close a typical cross-border

acquisition of equity of a PRC Target Company owned by a Germany company

(“Seller”).

In this transaction, Seller is going

to sell its 100% equity of Target Company in PRC. Our client is a Hong Kong

company and prepared to acquire 100% equity of Target Company from Seller.

(2) The transaction schemes

The transaction scheme is the core of

a M&A transaction. It relates to the safety of the whole deal. In the

foresaid transaction, we hear the needs of our client and help them design the

following scheme:

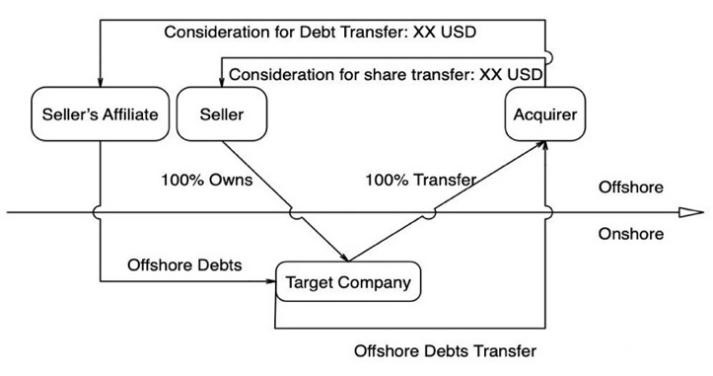

1) The sole shareholder

of Target Company is a Germany corporate, who holds 100% equity intertest of

Target Company.

2) The Germany

corporate has an affiliate company that lends several loans to Target Company.

On the top of that, if our client

pays 100% of the Equity Transfer Price, and eventually owns 100% equity

interest of Target Company after the Completion of transaction, our client may

face tremendous debts hold by affiliate company of the Seller. We have to

figure out a way to help our client resolve the debts issues. The 100% Equity

Transfer Price is a reflection of net assets plus future valuation of Target

Company, which is the combination of assets and debts of Target Company,

therefore, after the payment of equity transfer price, the assets should be

owned by our client via equity transfer and the debts should be resolved.

However, if we just ask the affiliate company of Seller to waive all the debts

after the Completion of transaction, our client may face tax issues due to debts

waiver (the waiver of debts raises profits in the book, which leads to income

taxes).

We suggest our client to conclude a

deal with affiliate company of Seller to accept the transfer of debts. There

are two reasons for us to suggest our client to accept the transfer of debts

instead of waiver of debts: i. taxes avoidance; ii. safety of transaction. In

accordance with the Administrative Measures on Registration of Foreign

Debt (“Foreign Debt Registration”), all the debts owned by a FIE to a

PRC corporate should be registered in the State Administration of Foreign

Exchange (“SAFE”) regarding of the establishment, adjustment and cancellation

of debts.

The waiver of debts would be

registered as cancellation of debts in SAFE, which might cause suspicions from

SAFE due to money laundry and raise tons of questions from authorities. For the

sake of safety of this transaction and registration in SAFE, we believe the

transfer of debts would be the best choice of our client. Therefore, we introduce

to our client the payment scheme: 60% of total equity transfer price would be

defined in SPA for equity transfer; 40% of total equity transfer price would be

defined in Loan Transfer Agreement (“LTA”) for transfer of all debts. The

fundamental transaction scheme is as following: 12

{kind=link}

We believe the transaction scheme is

the most important issue regarding of M&A transaction. Seeing from foresaid

case, there would be three important keys we have to take into account before

introducing the transaction scheme: i. tax issues; ii. safety of the

transaction; iii. efficiency and effectiveness of the transaction and all these

three keys serve one sole purpose that is facilitating the deal, not blowing

it.

(3) The locked box mechanism vs

completion accounts mechanism

A recent trend in the United Kingdom

and European M&A market is to use the "locked box" approach to

determine the price for a target business in the context of a private M&A

transaction instead of the conventional completion accounts approach. The primary

difference between the two mechanisms “locked box” and “completion accounts” is

the date of transfer of economic risk. When a completion accounts mechanism is

used, the Acquirer will pay for the actual level of assets and debts of the

target as at completion in accordance with a post-completion pricing

adjustment. The final price is not known for some time after completion. In

contrast, a locked box mechanism involves the parties agreeing a fixed equity

price calculated using a recent historical balance sheet of the target prepared

before the date of signing of the sale and purchase agreement. Cash, debt and

working capital as at the date of the locked box reference accounts are

therefore known by the parties at the time of signing and there is no post-completion

adjustment. The economic risk and benefits of the business pass to the Acquirer

from the date of the locked box reference accounts.

Each mechanism has advantages and

disadvantages, some of which we summarize below. The pros and cons of completion

accounts include:

Pros for Seller: May speed up

negotiations and conclusion of a deal as an Acquirer needs less comfort on the

balance sheet before completion, and the Seller retains the economic benefit in

the business including the profits right up until completion; Pros for

Acquirer: Only pays for what it gets because price is adjusted, and in full

control of business when compiling and checking completion accounts;

Cons for Seller: Less control over

the adjustment process, takes economic risk of business up to completion, delay

in ascertaining final price, and costs of preparing completion accounts and any

potential disputes; Cons for Acquirer: Delay in ascertaining final price, and

costs of preparation of completion accounts and any potential dispute.

The pros and cons of a locked box

mechanism include:

Pros for Seller: Certainty of price,

increased control over the process, simplicity and avoids cost of completion

accounts; Pros for Acquirer: Certainty of price, simplicity and avoids cost of

completion accounts;

Cons for Seller: Does not get full

benefit from continued operation of business in the interim period, and

post-locked box interest rate, if any, is often insufficient to compensate the

Seller for the earnings of the target during the interim period; Cons for

Acquirer: Enhanced due diligence (particularly financial) often necessary,

increased reliance on warranties, risk of business deteriorating between locked

box date and completion, need to debate items such as debt and working capital

earlier in the sale and purchase process.

Key issues that arise using a locked

box mechanism:

The sale and purchase agreement must

provide for "leakage", being any transfer of value from the target

business to the Seller or its connected parties between the locked box date and

completion including, for example, dividends and other distributions, and

management bonuses. The parties will need to negotiate what constitutes leakage

and other categories of payment which are permitted (including, for example, inter-group

payments in the ordinary course, agreed dividend payments, payroll). As a

target business is priced as at the date of the relevant reference accounts and

this is the date on which economic risk and reward passes to the Acquirer,

Sellers may ask for a specified rate of interest on the equity price,

particularly when disposing of a profitable business (given the level of

profits generated would remain in the business unless otherwise agreed).

In our case, we provide our client a modified

locked box mechanism for the transaction. We introduce a Base Day, on which all

assets and debts are consolidated in a fixed number and on that day, we settle

a Base Price based on the number generated from consolidated assets and debts

of Target Company. Therefore, there will be a transition period between Base

Day and Completion Day. Because that Target Company remains operating its

business in the transition period, and this would lead to the number fluctuated

till Completion Day, we create a working capital adjustment mechanism. In this mechanism,

the final equity transfer price would be Base Price plus working capital

adjustments in transition period. If both parties cooperate efficiently, the

transition period may not last for long, therefore, in this way, we could lock

the transaction in a certain transaction scheme and settle most of the equity

transfer price, which could avoid uncertainty in the deal and is safe for both

parties.

(4) Take advantage of Escrow Account

The most frequently argued issues

with lawyer from other party are the payment schedule of equity transfer price

and equity transfer registration. Both lawyers want the safest way to close the

deal, the lawyer from Acquirer wants the equity transfer to be done with

limited payment as soon as possible, however, the lawyer from Seller wants to

receive as much the money as possible before equity transfer. It looks like

this is unsolvable paradoxes before the launch of Escrow Account.

Escrow Account is a banking service

from most of the banks. Both parties could jointly open an Escrow Account which

is under control by both parties. Only with orders at the same time from both

parties, the money in the Escrow Account could be released. Escrow Account

provides a solution for the foresaid paradoxes. The Acquirer reimburses certain

percent of equity transfer price into Escrow Account and Seller initiates

equity transfer registration and after the completion is done, both parties

agree to release the money in Escrow Account to Seller.

In the end, from Acquirer’s aspect,

transparent and firm due diligence conducted by experienced attorneys prior to

M&A transaction is necessary and the result from due diligence would

provide tremendous help for attorneys to design transaction schemes and draft

transaction documents. A complex cross-border M&A transaction will not only

contain foresaid phrases also include but not limited to tax issues, foreign

currency issues, authorities’ permissions or qualifications, anti-trust issues

and so on. For the limitation of such context, we can not illustrate each of

the issues in terms of a complex M&A transaction. Thank you for your

attention, for more information, please do not hesitate to contact us.