Global Vietnam Lawyers | View firm profile

Ms. Tran Minh Nguyet & Ms. Le Thi Ngan

Global Vietnam Lawyers

Global Vietnam Lawyers would like to introduce our valued readers to an article by Ms. Tran Minh Nguyet and Ms. Le Thi Ngan titled “Vietnam enhancing transparency of beneficial ownership: From legislation to implementation”. This article was originally published in The Saigon Times, issue No.31-2025 (1.807) on July 31, 2025 and is shared here with permission from the publisher.

On July 1st 2025, the Law on amending and supplementing a number of articles of the Enterprise Law dated June 17th 2025 (“Enterprise Law 2025”) and Decree No. 168/2025/ND-CP dated June 30th 2025 on enterprise registration (“Decree 168”) entered into forced, making the first time that the concept of “beneficial owners” (BOs) has been regulated in Vietnam’s enterprise legislation. This represents a significant advancement in promoting transparency of business operations, particularly regarding individuals who actually control and benefit from the enterprise.

This move not only demonstrates Vietnam’s commitment to implementing Financial Action Task Force (“FATF”)’s recommendations regarding anti-money laundering (including the requirement for disclosure of the information of BOs of legal entities), but also serves as a crucial key in facilitating Vietnam’s removal from the Increased Monitoring List (or Grey List) and protect the country against the potential of being placed on the FATF List of High-Risk Jurisdictions subject to a Call for Action (Black List) .

Why are BOs important to Vietnam?

The inclusion of Vietnam on the Grey List could lead to a serious repercussion for the economy, especially impacting the private sector and other sectors attracting foreign investment. International investors tend to be cautious or withdraw from monitored markets, leading to a significant decline in FDI inflows. Not to mention that individuals and entities in the Grey List countries will also be subject to stricter scrutiny by the global banking system. The consequences could be even more severe if Vietnam is placed on the Black List, e.g. Vietnamese financial institutions could be barred from establishing their branches or representative offices abroad. The regulation of BOs in the enterprise law is anticipated to faciliate Vietnam’s timely exit from the FATF Grey List.

So, how to identify a BO and what should enterprises do when the regulations on BOs officially come into effect?

Identifying the beneficial owner of a legal entity

The concept of BOs, although newly introduced in the Enterprise Law 2025, has been utilized for an extend period in the field of anti-money laundering. Specifically, this concept has already appeared in the Anti-Money Laundering Law 2012 and remains relevant to be used in the Anti-Money Laundering Law 2022. The purpose is to assist financial institutions in verifying the identity of institutional customers.

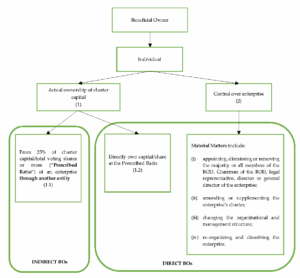

The concept of BOs in the Enterprise Law 2025 is well aligned with the provisions outlined in the Anti-Money Laundering Law 2022. The characteristics/identification criteria of BOs and how they are categorized under the enterprise law are presented in the following diagram:

The diagram above indicates that:

Firstly, a BO must be an individual. This is consistent with the FATF Recommendation 24 and established international practices, which aims to clearly identify the actual controller of an enterprise. If a “legal entity” qualifies as a BO, the disclosure mechanism fails to effectively trace to the ultimate individual controlling the enterprise, and therefore impairing the system of monitoring, preventing and combating money laundering, tax evasion or terrorist financing.

Secondly, in respect of criteria for identification of a BO: An individual qualifies as a BO when he/she meets either: criterion (1) Have actual ownership of the enterprise’s capital; OR criterion (2) Have control over that enterprise.

Regarding criterion (1), as described in the diagram, capital ownership can be established through the form of “direct ownership” – i.e. individuals who are listed as members or shareholders of an enterprise and own the Prescribed Ratio in that enterprise, OR through the form of “indirect ownership” – i.e. individuals who own capital at the Prescribed Ratio in an enterprise THROUGH ANOTHER ENTITY.

Concerning the “Prescribed Ratio” – from 25% of the charter capital or total voting shares, this is a threshold widely applied in many countries globally. According to a survey, 39 out of 63 countries (including 55 United Nations members and ASEAN countries) currently apply this ratio. Several countries implement a lower threshold, such as Colombia, the Philippines and Myanmar choosing a level as low as 5% to enhance control over BOs. In Vietnam, the Prescribed Ratio has actually been recognized since 2019 under Decree 87/2019 on anti-money laundering, and it remains in effect as outlined in Decree 19/2023, which elaborates on a number of articles of the Anti-Money Laundering Law 2022.

Regarding the form of “indirect ownership” through another entity, the entity serves as a member/shareholder of the enterprise, while the individual is a member/or shareholder of that entity.

For criterion (2), as the diagram indicates, an individual is deemed to have control over an enterprise if they possess the ability to vote for or against at least one of the Material Matters of the enterprise, even if their status is limited to that of a member or shareholder with a capital contribution or shares lower than the Prescribed Ratio.

Control over an enterprise often arises from provisions in “shareholders’ agreements” or “members’ agreements”, in which a certain member or shareholder holds only a minority capital ratio yet retain the ability to influence decisions on the Material Matters of the enterprise, due to the binding terms of such agreements.

Categorizing BOs and illustrative scenarios: understanding for accurate declaration compliance

Individuals who “directly own” the Prescribed Ratio according to criterion (1), or who have control over an enterprise according to criterion (2), are categorized as Direct BOs. Meanwhile individuals who “indirectly own” the Prescribed Ratio according to criterion (1) are categorized as Indirect BOs. This way of categorization facilitates enterprises to fulfill the obligations for declaring and providing information of BOs to the provincial business registration agency, as presented below.

To make it easier to understand, let’s analyze the following scenarios:

The following 03 scenarios will be analyzed in relation to BOs of joint stock companies (“JSC”) and limited liability companies (“LLC”). In each scenario, you can visualize how to identify the actual BO and then refer to the corresponding declaration obligations stipulated by law:

| No. | Company | Shareholder/Member | BO | Grounds for identification | |

| Direct BOs | Indirect BOs

|

||||

| 1. | JSC 1

|

03 shareholders:

Individual A1: 20% Individual B1: 25% Company C1: 55%

C1 is a one-member LLC owned by Individual X1

|

B1 | X1 |

X1 is an Indirect BO because X1 through C1 indirectly owns 55% (100 x 55%) of the charter capital/total voting shares of JSC 1 – meeting the Prescribed Ratio.

|

| 2. | JSC 2 | 03 shareholders:

Individual A2: 20% Individual B2: 25% Company C2: 55%

A2 has a shareholders’ agreement with B2 and C2, stipulating that any amendment/supplement to the charter or the reorganization/dissolution of JSC 2 can only be approved by the shareholders representing at least 65% of the total votes of all shareholders attending the meeting AND WITH A VOTE OF APPROVAL FROM A2.

C2 is a LLC with 02 members, including X2 and Y2, with the capital ownership ratio being 80% and 20% respectively.

|

A2

B2 |

X2 |

|

| 3. | LLC 1 | The one-member LLC is owned by Company C3.

(C3 is a one-member LLC owned by Individual X3) |

None | X3 |

|

So, what should enterprises do next?

Basically, depending on the form of the BO, the enterprise will have corresponding obligations. Specifically:

| Subjects performing obligations | Obligations regarding BO information | |

| Direct BO | Indirect BO | |

| LLC

|

Declaration time: At the time of establishment of the enterprise and when there is a change in BO information or declared ownership ratio.

|

|

| Partnership

|

||

| JSC

|

Declaration time: At the time of establishment of the enterprise and when there is a change in the declared information

|

|

| Note: For enterprises established before July 1, 2025, the addition of information on the enterprise’s BO (if any), information to determine the enterprise’s BO (if any) is carried out[1]:

|

||

As stated in the table above, JSCs have an additional obligation to declare “information to determine” Indirect BO instead of directly declaring the identities of these individuals. This represents a distinctive aspect of the Vietnamese legal system in contrast to international practices, as illustrated by the following two points:

First, rather than mandating that enterprises identify and disclose the identities of Indirect BO themselves, the existing enterprise legislation only requires enterprises (specifically only requiring JSCs) to declare “information related” to Indirect BO to assist authority in identifying these individuals.

This related information pertains to be “organizational shareholders” of a JSC, specifically when such shareholders possess a captial stake that reaches the Prescribed Ratio threshold in that JSC. The process of gathering information regarding “organizational shareholders” of a JSC serve as a foundational data source, assisting the authorities gradually clarify the identity of the individuals behind – the Indirect BO of the JSC.

Second, the obligation to declare information to determine the Indirect BO is applicable sole to JSCs, excluding LLCs or partnerships.

This issue may stem from the current enterprise registration data system’s lack of a mechanism to store complete information regarding all shareholders of a JSC – except for founding shareholders and shareholders who are foreign investors . Meanwhile, the system has effectively managed information on members of LLCs and general partners of partnerships, including information at the time of establishment and changes throughout the operation process .

All information about shareholders of a JSC, on the other hand, is exclusively recorded in the shareholder register, which is a record maintained and preserved by the JSC itself , from its establishment until each change. This information will remain unchanged at the business registration agency (except for information about founding shareholders and shareholders who are foreign investors).

The reduction in the scope of subjects and types of information required for declaration related to Indirect BO at this initial phrase represents a reasonable adjustment by the legislator, aiming to balance the demands of transparency and the ability to implement in practice of the enterprise.

Thus, based on the above provisions, JSC 1, JSC 2 and LLC 1 in the illustrative situations will have to fulfill the following declaration obligations:

| Enterprise | Direct BO | Indirect BO |

| JSC 1 | Declare and notify information about B1

|

Declare and notify information about C1, including organization name, enterprise code/establishment decision number, date of issue, place of issue, head office address, ownership ratio of total voting shares in JSC 1

|

| JSC 2 | Declare and notify information about A2 and B2

|

Declare and notify information about C2 similarly to JSC 1

|

| LLC 1

|

Challenges arising from Nominee Arrangements: A Loophole in BO Transparency?

Despite advancement in the law, the concept of “nominee arrangements” – a type of “disguised” investment – remains to pose significant challenges in identifying the actual BO. Accordingly, a domestic individual or organization may act on behalf of a foreign investor to establish an enterprise and be recorded as a shareholder or capital contributor, while all actual control, benefits and decision-making rights are retained by the foreign investor.

Consequently, even when enterprises declare members and shareholders of companies to identify the actual BO, the concealed investors may still exist without being disclosed and there is currently no effective mechanism to detect or control such arrangements. This issue reflects complexities within the market, especially those involving property ownership and intricate investment structures that currently fall outside the direct purview of enterprise laws. Therefore, in the immediate future, the enterprise laws only require declaration of basic information, aiming to ensure initial compliance to international commitments.

Conclusion and prospects

The official incorporation of the concept of BOs and obligation to declare BOs into Vietnam’s enterprise legal framework marks a significant milestone in enhancing transparency in corporate ownership, corporate governance, and anti-money laundering efforts.

To ensure full compliance with new regulations and mitigate potential legal risks, enterprises should proactively review their organizational structure, clearly identify their BOs, and promptly update information with the business registration authority. Such declarations serve as a foundation for the authority to progressively establish a more comprehensive and coordinated monitoring data system in the near future, contributing to the enhancement of Vietnam’s investment environment reputation on the international arena.