If there was ever any doubt about what might be in store for the Volkswagen Group following its recent emissions scandal, a glance at the banking industry over the last five years offers a sobering clue.

It is nearly seven years since many banks were deemed too big to fail during the financial crisis of 2008 and 2009. The price of being rescued, and for bringing the global economy to its knees, was regulation on a scale never previously experienced. In the wake of this increased regulatory oversight, a series of mis-selling and rate manipulation scandals have cost the banking industry billions of pounds in fines, civil settlements and legal fees. Only now, some years later, is there even the slightest expectation that the worst is in the past, or at the very least out in the public domain.

‘There was obviously a massive and sudden increase in the number of regulatory investigations and litigation, but now we’re at a steady state in terms of volume,’ says one in-house lawyer at a major bank. ‘The very large cases are known and those that haven’t quite made the public forum are known. I would be surprised if there is any more of the bring-the-house-down litigation, like Libor and Forex, the real mega-cases.’

| Top ten FCA and FSA fines | |||||

|---|---|---|---|---|---|

| Rank | Fine value | Institution | Reason | Date | Bank legal adviser |

| 1 | £284,432,000 | Barclays | Failure to control FX trading business | 20/05/2015 | Clifford Chance |

| 2 | £233,814,000 | UBS | Failure to control FX trading business | 11/11/2014 | Gibson, Dunn & Crutcher |

| 3 | £226,800,000 | Deutsche Bank | For Libor-related misconduct and misleading the regulator | 23/04/2015 | Slaughter and May |

| 4 | £225,575,000 | Citibank | Failure to control its FX trading business | 11/11/2014 | Allen & Overy |

| 5 | £222,166,000 | JPMorgan Chase | Failure to control its FX trading business | 11/11/2014 | Slaughter and May |

| 6 | £217,000,000 | The Royal Bank of Scotland | Failure to control its FX trading business | 11/11/2014 | Linklaters |

| 7 | £216,363,000 | HSBC | Failure to control its FX trading business | 11/11/2014 | Cleary Gottlieb Steen & Hamilton |

| 8 | £160,000,000 | UBS | For Libor-related misconduct | 19/12/2012 | Gibson, Dunn & Crutcher |

| 9 | £137,610,000 | JPMorgan Chase | For serious failings relating to its ‘London Whale’ trades | 18/09/2013 | Sullivan & Cromwell |

| 10 | £126,000,000 | The Bank of New York Mellon | Failure to comply with custody rules | 15/04/2015 | Allen & Overy |

| Source: FCA | |||||

To better understand the financial industry’s current attitude towards regulation and litigation, Legal Business teamed up with Simmons & Simmons to survey senior in-house disputes and regulatory lawyers at major banks, asset managers, hedge funds and other financial institutions. We also interviewed senior general counsel (GCs), barristers and high court judges to find out where they feel regulation and litigation are headed, and what sort of infrastructure and mechanisms have been put in place to better manage these risks.

Peak fines

For financial institutions, unquestionably, the burden of regulation and litigation will remain heavy for the foreseeable future. Eighty-eight percent of respondents to the survey have been involved in a formal dispute since 2013 (when we last surveyed the in-house banking litigation community), while 68% have experienced a regulatory investigation. This is illustrated by the growth in UK civil claims involving major financial institutions, and the larger fines handed out by the Financial Conduct Authority (FCA) and its predecessor the Financial Services Authority (FSA) (see ‘Ten years of FCA and FSA fines’ and ‘Significant litigation involving major financial institutions’ below).

For litigation, the number of claims involving financial institutions climbed from 95 in 2008 to 192 claims in 2014. The contrast in regulatory fines is greater still: in 2007, the FSA handed out £5.3m in fines, just 0.36% of the £1.47bn that the FCA issued in 2014. Fines for 2015 currently stand at £826.9m, which includes a record fine of £284m given to Barclays for ‘failing to control business practices in its foreign exchange (FX) business’.

Breakdown of respondents

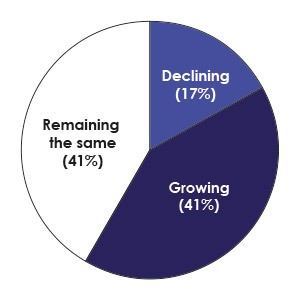

How many formal disputes (including arbitrations) has your institution been involved in since 2013?

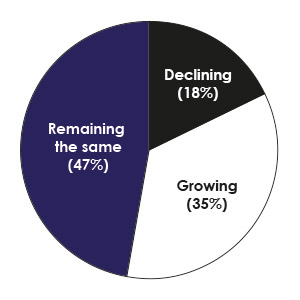

How many regulatory investigations has your institution been involved in since 2013?

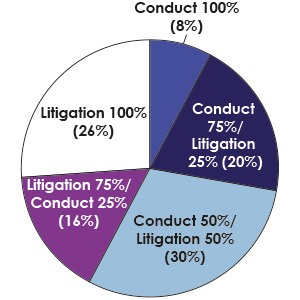

What do you envisage will be the balance between conduct and litigation matters?

Barclays’ annual reports illustrate the growing significance of its various regulatory and legal proceedings. In 2007 they merited a page and a half in the ‘Notes to the Financial Statements’. By 2014, coverage had ballooned to over 11 pages, plus a significant mention in the chief executive’s review. The notes included a £5.2bn provision against the cost of payment protection insurance (PPI) redress; £1.5bn for ‘Interest Rate Hedging Product redress’; and £1.25bn held for ‘ongoing investigations’ and ‘litigation relating to Foreign Exchange’. According to a Reuters report published in May, 20 of the world’s largest banks have paid £151.7bn in fines and compensation since 2008. Roughly 60% was linked to mis-sold mortgages in the US, while nearly 20% was linked to the mis-selling of insurance products in the UK, such as PPI.

BANKING ON TROUBLE: THE RISE OF IN-HOUSE LITIGATION AND REGULATORY TEAMS

While the growing importance banks and financial services place on their in-house disputes and regulatory teams is unsurprising, given the huge regulatory burden that they now face, the speed of that growth has been startling. In the case of many banks, a vital in-house legal function that is now taken for granted barely existed in 2007.

‘There is now a regulatory and contentious side; there never was before – no-one ever heard of it and it didn’t exist,’ says one experienced in-house litigator. ‘It’s a reasonably recent phenomenon. Regulation has basically overtaken the dispute resolution world since 2008/09.’

The development of Barclays’ global litigation function, following the appointment of Bob Hoyt as general counsel (GC) in 2013, illustrates the strategic importance that litigation and regulation have to the bank and to the wider industry as a whole. Whereas in the past, separate litigation heads at Barclays were spread across separate business units, now there is one, Stephanie Pagni, who was appointed head of litigation, enforcements and investigations in May 2014 and reports directly to Hoyt, sits on the legal executive committee and is a member of Barclays’ senior leadership group.

Since Hoyt’s arrival, there has been a changing of the guard at Barclays. Several senior lawyers have left, including deputy GC Michael Shaw, who departed in September 2015, and Barclays corporate and investment banking global GC Judith Shepherd, whose exit was announced in January. Others have taken jobs elsewhere, such as former EMEA GC for Barclays Investment Bank, Erica Handling, who is now EMEA GC at global asset manager BlackRock. Meanwhile, the bank’s former global head of financial crime legal, Jonathan Peddie, joined Baker & McKenzie as a partner in its corporate investigations group after leaving the bank earlier this year.

The in-house merry-go-round hasn’t been exclusive to Barclays. 2015 saw several new names crop up in senior litigation and regulatory positions at other major banks, including Wilson Thorburn, who left JP Morgan to become GC for group litigation, regulatory and competition legal at Lloyds Banking Group, replacing Philippa Simmons. Thorburn’s arrival preceded the announcement that Lloyds GC, Andrew Whittaker, was stepping down after two years, to be replaced by his deputy, Kate Cheetham, in May. Cheetham will eventually report to outgoing Linklaters’ managing partner, Simon Davies, who is joining the bank in January 2016 as chief people, legal and strategy officer.

Of those surveyed, a third stated that their in-house litigation teams have grown in the past two years, while 50% have remained the same size. In addition, when it comes to recruitment of in-house counsel, the banks are fishing from a much larger talent pool, including rival banks, private practice firms and the regulators themselves.

‘We’re able to recruit from really good Magic Circle firms, because they’re intrigued at what the financial services are going through and how we deal with the regulator,’ says Joanna Day, director of legal services for Santander UK. ‘There is an opportunity to engage more in strategy and tactics than you would elsewhere.’

There is also a growing acceptance by other departments within banks that legal and regulatory issues are critically important to what they do.

‘We are in the process of rolling out on a worldwide basis a database where all notes and analysis on new banking and financial regulations affecting the group will be gathered and be accessible to the other stakeholders outside the legal department,’ says Société Générale group GC Dominique Bourrinet. ‘This is something that ten years ago would probably not have been put into existence and that reflects the growing regulatory implications on business.’

As other departments increasingly grapple with the regulatory aspects of their business, the reverse is true of the lawyers, who are now more focused on how the wider business fits into the changing regulatory landscape.

‘In terms of what the lawyers do, we’re no longer focused on things like the Civil Procedure Rules,’ says Day. ‘You need to be focused on really, truly understanding the bank’s business – understanding the tactics and strategies for dealing with a lot of these things. We operate in a regulatory framework that is principles-based. That, from a lawyer’s point of view, opens up greater scope for interpretation than it would in a strict line-by-line translation of the rules.’

This in-depth understanding of the business is something in-house lawyers expect from their external counsel as well, particularly in the wake of increased regulatory scrutiny.

‘When you have an investigation, generally it involves getting into the weeds of how the bank operates,’ says the head of litigation at one bank. ‘The natural consequence of that is the law firms will get to know you and how you work better. You also spend a lot more time with each other, so on a personal level you do get to know each other better.’

In the most high-profile regulatory and civil cases, these relationships will go to the very top. This is reflected in the way that banks like Barclays are giving their senior litigators prominent leadership positions and why high-profile private practice lawyers such as Davies at Linklaters would consider an in-house position at Lloyds. For those seeking a challenge, the exposure that senior in-house litigators are now getting to the top echelons of the business is clearly appealing.

‘Because of the regulatory investigations, and these are really bet-the-branch type claims, they are all subject to an incredible amount of board attention,’ says another senior in-house litigator. ‘In the past, a litigation or regulatory investigation, to the extent that there was any, would not necessarily hit board level. Now it does.’

While the pressure remains high, there is a subtle difference between the volumes of claims and regulatory investigations that our 86 respondents expect to see, and expected costs. While 41% percent expect to see civil claims grow, only 18% are allocating more funds to forthcoming litigation costs and settlements. Similarly, while 35% expect the number of regulatory investigations they are involved in to grow, only 18% are allocating more funds towards regulatory fines. This in part reflects a view that, given levels were very high to start with, the overall value of fines and settlements can only go down. This can already be seen with PPI settlements, where FCA-reported payouts to customers were down to £300.5m in August, the lowest monthly figure since September 2011. Now that the FCA has announced a deadline of 2018 for PPI settlements, the end is quite literally in sight.

‘I would be surprised if the FCA’s total fines for 2016 are as high as the totals for 2015 or 2014,’ says Robert Turner, head of Simmons & Simmons’ international financial markets litigation group. ‘There may be a higher number of fines, but without something dramatic in the market place, it seems unlikely these numbers will be as high. We’d probably all know about it by now if there was going to be something on the same scale.’

‘A rapport’

The internal legal and regulatory infrastructure that the banks and financial institutions have is also considerably larger and more sophisticated than only a few years ago (see ‘Banking on trouble’ above). Thirty-one per cent of respondents’ in-house teams have grown in the last two years, while 50% are unchanged. That financial institutions have seriously invested in these areas has gone some way to improving their relationship with the regulators.

| Annual PPI refunds and compensation | |

|---|---|

| Year | Refunds and compensation |

| 2015 (to August) | £3.02bn |

| 2014 | £4.474bn |

| 2013 | £5.259bn |

| 2012 | £6.281bn |

| 2011 | £2.134bn |

| TOTAL | £21.168bn |

| Source: FCA | |

| Ten years of FCA and FSA fines | |

|---|---|

| Year | Total fines |

| 2015 (to date) | £826.9m |

| 2014 | £1,471.4m |

| 2013 | £474.3m |

| 2012 | £311.6m |

| 2011 | £66.1m |

| 2010 | £89.2m |

| 2009 | £35m |

| 2008 | £22.7m |

| 2007 | £5.3m |

| 2006 | £13.3m |

| Source: FCA | |

‘A lot of the banks are very sophisticated about how they deal with internal issues now and their infrastructure for dealing with things, and the FCA’s confidence in them dealing with things is probably higher than it used to be,’ says Marc Thorley, a financial markets litigation partner at Simmons. ‘A number of the banks have become efficient in doing their own internal investigations.’

‘We have a very well-defined and well-understood escalation process within the organisation,’ says Joanna Day, director of legal services at Santander UK. ‘We really believe in being transparent and upfront with the regulator, and if we didn’t, we would be in breach of regulatory principles.’

‘The key challenge in terms of our relationship with the regulators is to keep a relationship based on trust and clarity,’ says Dominique Bourrinet, group GC at Société Générale. ‘We really put a lot of emphasis on making that relationship as streamlined as possible. For that purpose, we have built up a team dedicated to co-ordinating with our main regulators, so that we can answer their queries on a timely basis and really feel it is a working relationship.’

The greater investment in staff that the FCA has made into its supervision department has also helped. ‘Its teams have racked up considerably, so they are now able to deal with the volume of work they have got on their plate,’ says one GC. ‘There is more consistency among the individuals, so you do have a rapport. Let’s not underestimate the importance of that. We now feel as though we’re being given a fair hearing and I get the sense that there is a lot more co-operation on each side.’

Held to account

The rhetoric coming from the Treasury and the regulators is also softening. In a recent speech at Mansion House, the FCA’s acting chief executive Tracey McDermott said: ‘The intensity and volume of regulatory activity over recent years is not sustainable, for regulators or for the industry. We are often told that boards are now spending the majority of their time on regulatory matters. This cannot be in anyone’s interests.’

Compared with claim volumes over the last two years, the number of disputes your institution is involved in is:

Compared with last year, is your institution allocating more funds to meet forthcoming litigation costs and settlements?

Compared with volumes over the last two years, the number of regulatory investigations your institution is involved in is:

Compared with last year, is your institution allocating more funds to meet regulatory fines?

The most dramatic example of this softer approach was the recent watering down of the Senior Managers Regime (SMR), which is hitting banks in March 2016 to increase the individual accountability of senior managers. Initially the SMR had a ‘presumption of responsibility’, where senior bankers had to prove that they took such steps as a person in their position could reasonably be expected to take to prevent regulatory breaches. This reverse burden of proof has now been dropped and the regulator will now have to prove that the senior bankers failed to ‘prevent regulatory breaches in the areas of the firm for which they are responsible’.

‘I would describe it as a major u-turn by the government,’ says Richard Sims, a contentious regulatory partner at Simmons, who previously worked for three years in the enforcement division of the FSA. ‘That is obviously very welcome news to the sector and more widely.’

While the SMR has been pulled back slightly, its introduction to UK banks next year, and the wider UK financial services market in 2018, demonstrates a long-heralded shift towards greater personal accountability. This hasn’t gone unnoticed at the banks, where 96% of respondents felt that the regulatory focus on an individual’s accountability has increased.

‘A MESSAGE HAS BEEN SENT’: RECENT KEY BANKING CASES

PLEVIN V PARAGON PERSONAL FINANCE

According to one bank’s head of litigation, this was a case that ‘nobody saw coming’. Despite humble origins, its precedent-setting verdict could result in banks facing a flood of additional payment protection insurance (PPI) claims.

The claimant was Susan Plevin, who took out a £34,000 loan in 2006 from Paragon. She also took out £5,780 in PPI coverage, not knowing that 71.8% of the premium went towards commissions to Paragon and LL Processing (LLP), a credit broker that arranged the loan from Paragon.

In January 2009, Plevin brought proceedings against LLP and Paragon. The claim against LLP was settled in 2010 for £3,000. The claim against Paragon went to the Supreme Court, which in November 2014 ruled that Paragon’s relationship with Plevin was unfair because the lender had not disclosed the commission. The banking industry is currently awaiting guidance from a Financial Conduct Authority (FCA) consultation on the Plevin judgment. In the worst-case scenario, it could open the floodgates for further PPI claims focusing on similar ‘unfair relationships’ and undeclared PPI commissions.

For Plevin: Miller Gardner Solicitors; Hodge Malek QC and James Strachan QC (39 Essex Chambers); and John Campbell SC (4-5 Gray’s Inn Square).

For Paragon: Irwin Mitchell; Jonathan Crow QC (4 Stone Buildings); and Ian Wilson and Sandy Phipps (3 Verulam Buildings).

R V TOM HAYES

The 14-year prison sentence – with a minimum of seven years’ prison time – given to former UBS and Citigroup derivatives trader Tom Hayes in August, for manipulating Libor rates, certainly caught the City’s attention.

In his sentencing remarks, Mr Justice Cooke said: ‘There is no separate standard of dishonesty for any group of society… a message has been sent out to the world of banking accordingly [that] probity and honesty are essential.’

Hayes was the first person to be convicted over the rate-rigging scandal, though another trial alleging fraud against a further six ex-brokers started in October in Southwark Crown Court, as have separate trials against traders in the US. Coupled with the imminent introduction of the FCA’s Senior Managers Regime, Hayes’ sentence marks a new era of personal accountability for banking staff.

For the Serious Fraud Office: Mukul Chawla QC (9-12 Bell Yard); Andrew Onslow QC (3 Verulam Buildings); and Max Baines and Gillian Jones (Red Lion Chambers).

For Tom Hayes: Cartwright King Solicitors; Neil Hawes QC (Charter Chambers); and Christopher Convey and Catherine Collins (33 Chancery Lane).

INTEREST RATE SWAP AND LIBOR CIVIL CLAIMS

The scandal surrounding the manipulation of Libor and the alleged mis-selling of interest rate swaps has resulted in a slew of claims and test cases. One of the largest was Graiseley Properties & ors v Barclays Bank & ors, a dispute that was settled on the eve of trial in 2014.

But Graiseley owner Gary Hartland remains a thorn in the banking industry’s side. Another of his companies, Wingate & Associates Realtors, is pursuing a claim against Lloyds Bank attempting to overturn a previous settlement made with the bank in 2011, following the revelation that Lloyds was involved in Libor rigging. Should the claim succeed, it would likely lead to other settlements being reopened. Similarly, an Indian property company Unitech was allowed to amend its mis-selling claim against Deutsche Bank to factor in Libor manipulation.

Another major case is Property Alliance Group v The Royal Bank of Scotland, set for trial in June 2016. Here, The Royal Bank of Scotland (RBS) has already suffered a pre-trial setback after being ordered to turn over confidential regulatory reports concerning its alleged manipulation of Libor.

However, it hasn’t all gone against the banks: the first mis-selling trial in 2013 saw RBS defeat a claim brought by property developers John Green and Paul Rowley, who were subsequently refused leave to appeal. More recently, in Crestsign v National Westminster Bank & anor, the defendant banks avoided liability for negligent advice because of their contractual terms and conditions. Crestsign has, however, been granted an appeal, which will be heard in 2016.

PROPERTY ALLIANCE GROUP V THE ROYAL BANK OF SCOTLAND

For Property Alliance Group: Cooke Young & Keidan; Tim Lord QC and Kyle Lawson (Brick Court Chambers); and Adam Cloherty (XXIV Old Buildings).

For RBS: Dentons; David Railton QC and Adam Sher (Fountain Court Chambers).

WINGATE ASSOCIATES V LLOYDS BANK

For Wingate Associates: Hausfeld; Stephen Auld QC (One Essex Court); and Farhaz Khan and Miranda de Savorgnani (Outer Temple Chambers).

For Lloyds Bank: Hogan Lovells; and Richard Handyside QC (Fountain Court).

DEUTSCHE BANK & ORS V UNITECH GLOBAL & ORS

For Deutsche Bank: Freshfields Bruckhaus Deringer and Allen & Overy (A&O); Mark Hapgood QC (Brick Court); Timothy Howe QC, Richard Handyside QC, Adam Zellick and Adam Sher (Fountain Court).

For Unitech: Stephenson Harwood; Thomas Sharpe QC and Michael d’Arcy (One Essex Court); and John Brisby QC and Alastair Tomson (4 Stone Buildings).

CRESTSIGN V NATIONAL WESTMINSTER BANK & ANOR

For Crestsign: Slater and Gordon; Richard Edwards (3 Verulam Buildings).

For RBS and NatWest: DLA Piper; Andrew Mitchell QC (Fountain Court); and Laura John (3 Verulam Buildings).

RBS RIGHTS ISSUE LITIGATION

Set for trial in December 2016, the £4bn+ shareholder claim against RBS and its former directors is undoubtedly one of the largest to ever hit the UK courts. The claim concerns the bank’s £12bn rights issue in April 2008 where shares were sold at £2 each. The claimants argue that the prospectus was defective and contained material misstatements and omissions. Unsurprisingly, RBS’s legal fees are racking up, with Herbert Smith Freehills’ costs for the initial trial anticipated to be around £90m. The case is seen by many as setting a precedent for US-style group actions in the UK, and a similar claim has since been made by shareholders against Lloyds Bank and its directors concerning its 2008 takeover of HBOS.

For RBS: Herbert Smith Freehills; David Railton QC and James McClelland (Fountain Court), David Blayney QC and Simon Hattan (Serle Court); and Sonia Tolaney QC (3 Verulam Buildings).

For the claimants:

- For RBS Shareholders Action Group – Signature Litigation; and Jonathan Nash QC, Peter de Verneuil Smith and Ian Higgins (3 Verulam Buildings).

- For a group of over 70 institutional investors – Stewarts Law; and Andrew Onslow QC, Adam Kramer and Scott Ralston (3 Verulam Buildings).

- For RBS Rights Issue Action Group – Leon Kaye Solicitors; and Michael Lazarus (3 Verulam Buildings).

- For major institutional investors: Aviva, Legal & General Group, Prudential, Standard Life, and Universities Superannuation Scheme – Quinn Emanuel Urquhart & Sullivan; Laurence Rabinowitz QC and Maximilian Schlote (One Essex Court); and Alex Barden (Erskine Chambers).

- For nine pension investment subsidiaries of Lloyds Banking Group, including Scottish Widows and Halifax Life – Mishcon de Reya.

US CLASS ACTIONS

The second half of 2015 saw US-based banks make several multibillion-dollar settlements following investor class actions. In September, Quinn Emanuel helped one group of investors reach a $1.87bn settlement with 12 major banks, as well as the data provider Markit and the International Swaps and Derivatives Association (ISDA). The investors alleged that the defendants conspired to manipulate swap rates and blocked competitors from entering the credit default swap market.

US litigation specialist Scott + Scott also led a class action accusing 16 banks of widespread Forex manipulation. In October, a settlement was reached with five banks, including Barclays, HSBC and RBS, which respectively paid out $384m, $285m and $255m. Scott + Scott is in the process of opening a UK office. While the firm awaits its licence to practise, it has instructed Daniel Jowell QC of Brick Court Chambers to prepare a UK action against several banks for Forex manipulation.

CREDIT DERIVATIVES CLAIM

For the investors: Quinn Emanuel

For the defendants: Bank of America – Davis Polk & Wardwell; Morgan Stanley – Cravath, Swaine & Moore; JPMorgan Chase – Skadden, Arps, Slate, Meagher & Flom; Goldman Sachs – Sullivan & Cromwell and Winston & Strawn; Citibank – Sidley Austin; Deutsche Bank – Jones Day; Credit Suisse – Hogan Lovells; BNP Paribas – A&O; RBS – Cadwalader, Wickersham & Taft; HSBC – Mayer Brown; Barclays – Cahill Gordon & Reindel; ISDA – Simpson Thacher & Bartlett; Markit – Proskauer Rose.

US FOREX CLAIM

For the investors: Scott + Scott

For the banks: Barclays – Sullivan & Cromwell; HSBC – Locke Lord; RBS – Davis Polk & Wardwell; BNP Paribas – A&O; Goldman Sachs – Cleary Gottlieb Steen & Hamilton.

‘The FCA has talked for years about holding senior individuals to account,’ says Sims. ‘It has expressed its frustration over not being able to take effective enforcement action against individuals as a result of the financial crisis and some of the banking failures around that. It’s only now that it is starting to feel it has the right tools in place to hold individuals to account.’

The increase in personal accountability gives the FCA a far bigger stick with which to achieve its main goal of getting banks to improve their culture.

‘There isn’t any instant fix, there has to be a cultural shift in thinking,’ says one in-house litigator. ‘It’s quite simple: bankers just need to learn and appreciate that the customer must come first. If you look at the behaviours that have driven where the banks have gotten themselves into with the loans, a lot of it is due to financial reward. The incentivisation has been wrong. If the bankers stop being selfish, and learn and appreciate that the customer should come first, that would certainly help. Cultural shift is the bottom line.’

Many in-house counsel believe the challenge is as much a behavioural issue as a legal one.

‘It’s not a legal thing, it’s not a compliance thing,’ says Day. ‘If that was your grandmother that you were selling that product to, would you be happy about recommending it to her? That kind of approach has made people aware that dealing with the regulator isn’t just something for compliance, or legal and regulatory affairs.’

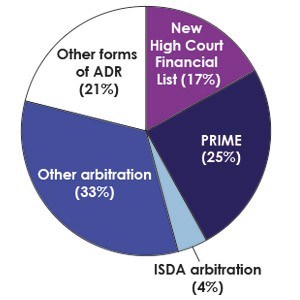

Do you plan to use any of the following in the near future?

Has your institution’s in-house litigation team grown in the last two years?

What is the biggest disincentive to litigation?

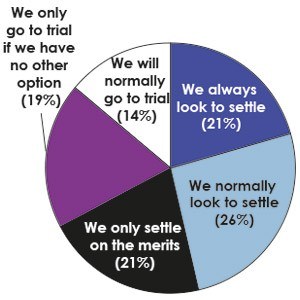

What describes your institution’s approach to litigation?

‘It is clear that the more efficient our corporate culture, procedures and controls are, the better the perception that the regulators will have of our own institution,’ says Bourrinet. ‘As a general rule, it is pretty obvious that there is a big expectation from regulators that we bring the compliance into the DNA of the bank – that everybody understands how important it is to comply with the regulations.’

Keeping it civil

When it comes to the growth in civil claims aimed at the industry, much of this stems from the time it has spent under the regulatory spotlight. This is evident with the asset managers and hedge funds, where 46% and 67% of respondents respectively expect to see their claim volumes grow.

‘As regulatory enforcement attention moves to asset managers, and as regulators notch up expectations with MiFID II [Markets in Financial Instruments Directive II], the reasons for asset managers getting involved in more litigation are not hard to see,’ says Turner. ‘You can see the trend with the banks, with next year’s litigation following this year’s regulatory findings, and I would expect to see the same with the asset managers.’

‘I would be surprised if the FCA’s total fines for 2016 are as high as the totals for 2015 or 2014.’

‘I would be surprised if the FCA’s total fines for 2016 are as high as the totals for 2015 or 2014.’

Robert Turner, Simmons & Simmons

For the banks, the full fallout from their Libor and FX rigging issues has yet to properly play out in the UK courts. Forty-three percent of respondents felt that benchmark manipulation and mis-selling issues will increase the volume of claims made against them. Whether these claims will succeed and what form they will take is another matter. When it comes to FX-related mis-selling claims, while there have been major group actions and settlements in the US, the success of this approach in the UK is still unknown. US claimant law firms such as Scott + Scott and Hausfeld have established themselves in the UK and made it clear that they plan to pursue FX group actions. Unsurprisingly, 67% of banks surveyed see class actions and group litigation as being a growing issue.

‘The issue is whether that is going to take off here,’ says Turner. ‘If FX-related claims, or investor claims against Volkswagen take off and are seen to succeed, then you can see that once the infrastructure is there, once the claimant bar is there and once the litigation funders are there, then self-fulfilling momentum becomes quite likely.’

The manipulation of Libor has also given extra life to interest rate swap mis-selling claims brought against the banks, such as Deutsche Bank and others v Unitech Global, which was adapted to allow for Libor rigging (see ‘A message has been sent’, pages 58-59). It remains to be seen, however, whether such cases will make it to a full-blown trial or simply settle out of court.

‘The only swaps mis-selling cases so far that have gone to trial and have got a judgment have ultimately gone in favour of the banks,’ says Richard Bunce, a banking litigation partner at Simmons. ‘There have been some bumps on the road and in interlocutory hearings recently there have been some decisions by the courts that seem claimant-friendly, allowing amendments to allow certain causes of action. Until someone is brave enough to take one of those cases all the way to trial, we’re not going to know.’

In the survey, 19% of respondents said they would only go to trial if they had no other option, while a further 47% would typically look to settle. For 42% of respondents, costs are the biggest disincentive to litigation. Only 7% see the risk of losing as a disincentive.

In the past, banks may have been inclined to settle, even when they had a good case. The reality now is that banks are forced to and willing to litigate the right cases.

Hit list

One factor that favours litigation is the high esteem in which most hold the UK court system, with 88% of respondents agreeing that the courts usually get it right. The cost and duration of such cases are, however, a disincentive and it is hoped that recent initiatives such as the October launch of the Financial List, will help address this. The List is dedicated to complex banking disputes valued at over £50m, and offers an even mix of ten specialist Chancery and Commercial Court judges all highly experienced in major financial disputes.

‘The only swaps mis-selling cases so far that have gone to trial and have got a judgment have ultimately gone in favour of the banks.’

‘The only swaps mis-selling cases so far that have gone to trial and have got a judgment have ultimately gone in favour of the banks.’

Richard Bunce, Simmons & Simmons

‘Financial disputes work is probably one of the busiest areas in current times and that seems likely to continue. The Financial List was a recognition of that position and the specialist nature of many of the disputes,’ says Sonia Tolaney QC of 3 Verulam Buildings, who led the List’s consultation process on behalf of the Commercial Bar.

Another important driver for the List, which at press time already had five cases on it, was the fact that ‘previously users were forced to choose to issue a case in either the Chancery Division or the Commercial Court, when in fact financial cases often straddle the two’, says Vannina Ettori, legal adviser and private secretary to the Chancellor of the High Court. ‘With the Financial List, the procedures are common and the judges who sit in the list can reliably be expected to have the right expertise for the case.’

One significant attraction is its Financial Markets Test Case Scheme, which will allow parties to resolve uncertain points of law with a hypothetical set of facts.

‘They are going to use it to resolve market issues in what they describe as “a friendly way”,’ says Craig Berry, head of litigation, commercial & private banking and capital resolution at The Royal Bank of Scotland. ‘There will be no adverse costs. It will simply be so that an issue can be put direct to the courts in a factual scenario, so that they can decide it and give the market guidance. It could be brilliant, if indeed it picks out the right issues.’

How much do you expect your institution to spend on settling conduct and litigation charges over the next two years?

A significant by-product of the List was the simultaneous launch of the Shorter and Flexible Trial Procedures pilot scheme, which is open to less complex commercial claims, where there is no need for extensive disputes over facts and less need for extensive disclosure. As with the Financial List, a key component will be the presence of a docketed judge for the entirety of the dispute.

‘The idea is that because you have a docketed trial judge managing the case from day one through to the trial, the judge is able both to review and police each procedural step taken and, as a consequence, assess the resulting legal costs on a summary basis, having given judgment,’ says Ed Crosse, a financial disputes partner at Simmons who was the solicitors’ representative on the shorter and flexible trials committee.

The pilot schemes were partly influenced by a successful fast-track procedure in the Australian commercial courts, as well as a similarly successful initiative in the UK’s Intellectual Property Enterprise Court (IPEC), which helped speed up intellectual property claims. Mr Justice Birss, who was a key driver behind the success of IPEC, is currently chair of the shorter and flexible trials committee.

‘There are significant similarities to IPEC,’ says Birss J. ‘What that court has been doing in the past five years is taking cases that you’d expect to be tried in one or two weeks and dealing with them in a day or two. Instead of coming on in a year and a half, you could get them so that they’re ready in six months. That is a critical lesson that it can be done.’

For the flexible trials scheme, lessons have also been learnt from arbitration. While the courts can’t compete with arbitral tribunals when it comes to confidentiality, the view is that the pilot scheme will prove that when parties agree, the courts can adopt the more flexible case management procedures used in arbitration.

‘If you consider arbitration, major commercial disputes are resolved in a way that can be quicker and more efficient than is sometimes the case in court,’ says Birss J. ‘In the right case I do not see why you cannot adopt similar techniques in court. It does not require parties to be any more imaginative than to think: “We can do this in arbitration, so why not in court?”’

| Significant litigation involving major financial institutions: Claims issued 2008-15 | |

|---|---|

| Year | Number of claims |

| 2015 (to date) | 100 |

| 2014 | 192 |

| 2013 | 246 |

| 2012 | 152 |

| 2011 | 144 |

| 2010 | 89 |

| 2009 | 110 |

| 2008 | 95 |

| Statistics based on information obtained from public sources by Bloomberg’s court service. Pleadings not yet available for all cases. Statistics therefore include cases identified on basis of parties’ names only.

Source: Simmons & Simmons |

|

Arbitration is one of the more popular forms of dispute resolution, with 30% planning to use it in the future, as are other more specialised forums such as PRIME Finance, a Dutch-based arbitration system set up to resolve complex derivatives and finance disputes. Mediation is also popular and Day says Santander uses it extensively for disputed commercial contracts.

Whichever route financial institutions take, demand on all of these forums will remain high. The crippling penalties might be waning, at least for those with decent internal measures in place, but new regulations will open financial institutions up to new sources of disputes. These won’t just come in the form of traditional stumbling blocks, such as fraud and mis-selling, but in new areas such as data protection and competition, which for UK-based financial institutions has come under the auspices of the FCA and its concurrent powers with the Competition and Markets Authority. And then there could be a black swan that catches everyone by surprise.

The hope is, however, that if another surprise does come, the investment into capable legal and regulatory functions will at least keep the punitive costs to a minimum.

SIMMONS & SIMMONS: OUR THOUGHTS

COLLECTIVE REDRESS

The survey results indicate that a majority of respondents see actions seeking collective redress as a growing (or rapidly growing) issue.

This reflects Simmons & Simmons’ recent experience. We have seen a significant growth in the number of enquiries related to such actions, particularly from amongst our asset management clients who are keen to understand what obligations they have to consider participation in such actions on behalf of their investors (if any) and the internal policies and procedures required to manage that process. It is difficult to predict whether collective redress procedures will take off in the UK in the same way as they have in other jurisdictions and, if so, how they will ultimately affect our clients. However, it is clear that actions seeking collective redress are already becoming more commonplace, and a significant success in any of the current high profile collective actions in the UK, coupled with the continued establishment of a strong claimant bar and credible litigation funding options, could well precipitate their rise.

SENIOR MANAGERS REGIME

The FCA has long expressed the desire to hold senior individuals to account. However, only now does it seems to feel that it may be beginning to have the tools to achieve that. The fact that a significant majority of survey respondents noted an increased (or much increased) regulatory focus on the accountability of individuals suggests that the message is getting through and it reflects what we have been seeing in practice.

The Senior Managers Regime (SMR) is clearly designed to complete the toolbox, with more clearly defined duties, statements of responsibility and responsibility maps all designed to lay trails for the regulator to follow. The reversal of the burden of proof would have made breaches easier to prove but the Government’s decision at the last minute to do away with that does not make it less likely that the FCA and PRA will press ahead where the consider it appropriate to do so.