KINANIS LLC > Nicosia, Cyprus > Firm Profile

KINANIS LLC Offices

12 EGYPT STREET

1097 NICOSIA

Cyprus

- Go to...

- Rankings

- Firm Profile

- Main Contacts

- Lawyer Profiles

- Press Releases

- Legal Developments

- Comparative Guides

KINANIS LLC > The Legal 500 Rankings

Cyprus > Tax Tier 1

The ‘exceptionally responsive’ team at KINANIS LLC garners praise for its ‘profound expertise’ in tax law. The group’s expertise spans transfer pricing, VAT, international tax planning, personal taxation matters and corporate tax, with noted strength in advising on the IP Box Regime. Under the leadership of Charalambos Meivatzis, Marios Palesis and Demetra Constantinou, the department is able to act for prominent international law firms, large accounting entities and other consulting firms. The group is also frequently engaged by clients in the technology, IP, real estate and financial services sectors. Yiota Michael is a name to note.Practice head(s):

Charalambos Meivatzis; Marios Palesis; Demetra Constantinou

Other key lawyers:

Testimonials

‘Key strengths include deep knowledge of local and international tax laws. Most importantly top quality services are offered in a professional manner in all cases, and you get a sense of a great team spirit. Stand out individuals are Charalambos Meivatzis, Marios Palesis and Yiota Michael.’

‘Marios Palesis stands out prominently. His extensive knowledge in the transfer pricing field is truly impressive, and his readiness to assist and answer any questions raised by clients is unmatched.’

‘Marios Palesis, Demetra Constantinou and Charalambos Meivatzis are reachable and willing to help.’

‘Charalambos Meivatzis, Marios Palesis, and Demetra Constantinou have a strong understanding of tax laws, regulations, and codes. They stay updated on changes in tax laws and are knowledgeable about various tax strategies. They always provide honest and ethical guidance.’

‘Yiota Michael is always there for us to answer even the most complex queries, and gives comprehensive advice for the benefit of our business. Her level of expertise and knowledge is and always has been of great value to us.’

‘Demetra Constantinou builds excellent relationships, and is always ready to find solutions. Responsive, welcoming, and efficient.’

‘Kinanis’ tax team has always been insightful and practical. I appreciate their efficiency and pragmatic approach. Charalambos Meivatzis and Marios Palesis always bring value to meetings and provide helpful recommendations.’

‘Great group of professionals: deep knowledge, responsive and friendly.’

Key clients

Xomonel Enterprises Ltd

Farsonex Investments Ltd

Megatren Investments Ltd

Halman Consultants (Overseas Ltd)

Audax Consulting

Chenor AG

Torwell Holdings

Lenhill

Elsavco Audit Tax Ltd

Istos Global Ltd

VATastic AG

Twiti Investments Ltd

Strikos Group

Tenet Group

Solicia Enterprises Ltd

CEA audit Ltd

Cobalt legal

Estron Corporation Limited

Cyprana Limited

Stalworth Pro Limited

N. Voskarides Audit Limited

Sephora (Cyprus) Ltd

Rubylight Ltd

Cyprus > Commercial, corporate and M&A Tier 3

The ‘experienced’ and ‘very responsive’ team at KINANIS LLC is led by Andrea Ioakim. The practice's expertise includes advising on the establishment of a company, day-to-day corporate management and governance, local and cross-border mergers, restructurings, liquidations and re-organisations. The department is also developing considerable strength in emerging areas such as nanotechnology. The client base includes entities from the real estate and aviation sectors.Practice head(s):

Andrea Ioakim

Other key lawyers:

Maria Pavlou; Valando Kavazi; Yiolanda Rotsides

Testimonials

‘Kinanis LLC is a solid practice that one can rely on. They deliver timely, good quality results that are tailored to the needs of the companies of our group. Friendliness, knowledge, experience and personalised approach.’

‘Their key capabilities are many, including quick turn-around, round-the-clock availability and compared to other law firms we work with, their advice is delivered in a thorough and clear manner. The team’s structure ensures the commercial advice provided is more rounded.’

‘Prompt in delivering legal advice, and highlighting potential risks. Andrea Ioakim in particular has excellent client management skills.’

‘It is great working with Andrea Ioakim. She is always available for us, and constantly up-to-date with all aspects of the work henceforth delivering thorough legal advice.’

‘We have worked predominantly with Maria Pavlou. She is well organised, diligent and ready to adjust to the client’s needs which is very much appreciated.’

‘Everyone at Kinanis LLC is professional, knowledgeable and kind. They take a pragmatic approach.’

‘Valando Kavazi and Yiolanda Rotsides are our principal contacts and we are happy to work with them.’

‘Andrea Ioakim is very experienced in the field of Cyprus corporate law. She is definitely a competent lawyer who can formulate a legal issue, assess risks and offer effective solutions in complex situations. Her legal opinions are always accurate, complete and require no further clarification.’

Key clients

VONPENDE HOLDINGS P.L.C.

TWITI INVESTMENTS LIMITED

Cyprus > Banking and finance Tier 4

The ‘accessible and practical’ team at KINANIS LLC is co-led by Christos Kinanis and Andri Michael. The practice is sought after by alternative investment funds, and is also instructed by international lenders, credit institutions, borrowers and shareholders in banking and finance matters. The group also garners praise for its experience in blockchain technology, and is adept at advising on the payment services regulatory framework in Cyprus.

Practice head(s):

Christos Kinanis; Andri Michael

Other key lawyers:

Savvina Miltiadou

Testimonials

‘First and foremost the team consists of very professional individuals. Over the years the team has built a strong network with numerous financial institutions and they provide prompt and accurate banking solutions as well as mediation services.’

‘Kinanis LLC’s Banking team is outstanding. Their dedication and skill in dealing with banking institutions results in swift and problem free banking operations for our group. Always proactive and solution orientated.’

‘The banking department of KLLC is outstanding, mostly due to the very capable people who are always very eager to assist us, as their knowledge and expertise in the banking sector is exceptional’.

‘Their detail-oriented approach is proof of their professionalism and excellence, always delivering in a timely manner.’

‘The Kinanis LLC team is assiduous, innovative and forward-looking. We are very pleased with our ongoing collaboration. The team’s keen interest and knowledge on emergent tech in general and blockchain technologies in particular, constitutes a competitive advantage over other law firms in Cyprus.’

‘Our overall experience with the team has been stellar. Their expert opinion is succinct and underpinned by extensive legal knowledge.’

‘Their accommodating and proactive approach makes one feel comfortable to engage them on matters related to regulatory compliance of financial services.’

‘Personal and direct access to partners and junior lawyers and other team members, straightforward advice and quick implementation.’

Key clients

EOS Multi-Strategy Fund AIFLNP V.C.I.C. Ltd

EpendiCY RAIF V.C.I.C. PLC

Vonpende Holdings PLC

Athena Capital Partners

Chenor AG

Aude FM Limited

ZoidPay (ZCN ZOID LTD)

Energy Transition Tech Fund RAIF V.C.I.C. Ltd

FinHub Cyprus

Cyprus > Dispute resolution Tier 5

Christos Kinanis and Costas Apokides jointly head up the practice at KINANIS LLC. The group’s core strength lies in advising on disputes concerning shareholder rights and corporate governance issues, and is also noted for handling contentious matters concerning administrative and competition law issues. The client base includes banks and investment funds, as well as healthcare, real estate and technology consulting companies.

Practice head(s):

Christos Kinanis; Costas Apokides

Testimonials

‘Very happy with the team, their experience and approach; very professional, whilst at the same time retaining some personal touch.’

‘Very happy with the associate handling my case; easily accessible, good knowledge; easy to communicate.’

Key clients

Parsimony Ltd

Electi Consulting Limited

Constantinos Christodoulou

ARK36 AIFLNP V.C.I.C. LTD

Mikkel Morch

Anto Paroian

KINANIS LLC > Firm Profile

The firm: Kinanis LLC, a law and consulting firm, is one of the leading business law firms in Cyprus and advises international investors and private clients on all aspects of law, tax and accounting. Kinanis LLC’s involvement and participation in international transactions over the years has established the firm as one of the key players in the field.

Areas of practice

Corporate/M&A and securities: the firm has extensive experience in advisory, procedural and transactional matters for JV transactions, M&A, reorganisation and restructuring, due diligence and legal opinions, pre-IPO compliance, as well as IPO and listings in stock exchanges both locally and internationally.

Taxation: the firm provides consulting on all aspects of Cyprus tax law, to both corporate and private clients, and assists clients in international tax planning, creating tax efficient corporate structures as well as providing ancillary services.

Banking and finance: the firm provides advice on banking and finance transactions consisting of drafting, reviewing and structuring finance projects, including advising on securities, guarantees, pledges and other encumbrances.

Incorporations and management of companies: the experienced corporate team advises clients on company matters such as incorporation, re-domiciliation, administration and management of Cyprus and overseas companies. It provides management services and may assist in the introduction of executive directors. Part of its consulting services include office facilities, IT support and HR consulting. Its specialist foreign desks can assist clients in the incorporation and management of companies of various jurisdictions (EU and Offshore).

Trusts, estate planning and succession: the firm has extensive experience in wills and probate, the establishment and administration of Cyprus international trusts, as well as local and foreign trusts and foundations, including acting as trustee and protector.

Financial services and funds: the team is ready to provide appropriate solutions and may assist with the establishment, registration and licensing of AIFs, CIFs, UCITS, FOREX, BINARY OPTION and insurance companies.

Accounting and VAT: maintaining proper books and records and management reporting under IFRS. The team of accountants provides VAT advice, compliance and payroll, as well as liaising with external auditors.

IP: the firm advises on IP tax structuring as well as on registration and protection of IP rights locally, internationally (CTM)/(WIPO) or EU-wide, as well as handling relevant oppositions at the corresponding fora.

Immovable property: the firm advises on commercial and residential legal issues regarding dealings with real estate, as well as providing ancillary services regarding management of real estate.

Litigation: the highly specialised litigation team represents clients in all aspects of corporate or commercial disputes, injunctions and interim relief, recognition and enforcement of foreign judgments or arbitral awards, representations in arbitration proceedings and pre-court negotiations.

Corporate liquidation: provides advice on the procedure of corporate liquidation and dissolution of companies locally and internationally.

Immigration and migration: the firm advises and assists individuals on making the best choice of citizenship or residency schemes based on their relocation needs. It obtains permanent residence permits, and also handles applications for citizenship by naturalisation or by exemption for Cyprus and Malta, Schengen Visa applications for Malta and other related ancillary services.

Energy: the firm advises on all aspects and activities related to energy operations, including advising on oil and gas finance transactions, advising on renewable energy and environmental law and regulations, and assisting with application/tenders on all types of energy projects etc.

Aviation and shipping: the firm provides advice on all legal, tax and VAT aspects of the acquisition, registration, financing, operation and disposal of vessels and aircrafts.

Main Contacts

| Department | Name | Telephone | |

|---|---|---|---|

| Corporate, M&A and securities | Christos P Kinanis | ||

| Litigation | Christos P Kinanis | ||

| Trusts, Estate Planning and Succession | Christos P Kinanis | ||

| Taxation | Charalambos Meivatzis | ||

| Accounting and VAT | Charalambos Meivatzis | ||

| Corporate liquidation | Natalie Petrides | ||

| Immigration | Natalie Petrides | ||

| Real Estate, Immovable Property | Natalie Petrides | ||

| Financial services & Funds | Andri Michael | ||

| Blockchain Consulting | Andri Michael | ||

| Capital Markets & Listings | Andri Michael | ||

| Banking & Finance | Andri Michael | ||

| Banking & Finance | Andrea Ioakim | ||

| Corporate, M&A and securities | Andrea Ioakim | ||

| Data Protection & Privacy | Andrea Ioakim | ||

| Accounting and VAT | Demetra Constantinou | ||

| Taxation | Marios Palesis | ||

| Intellectual property | Yiolanda Rotsides | ||

| Litigation | Costas Apokides |

Lawyer Profiles

| Photo | Name | Position | Profile |

|---|---|---|---|

|

Mr Archimidis Andreou | Associate Lawyer | View Profile |

|

Mr Costas Apokides | Counsel | View Profile |

|

Ms Theodora Charalambous | Senior Advisor | View Profile |

|

Ms Dona Constantinou | Senior Associate Lawyer | View Profile |

|

Mrs Andrea Ioakim | Partner | View Profile |

|

Ms Valando Kavazi | Senior Associate Lawyer | View Profile |

|

Mr Christos Kinanis | Managing Partner | View Profile |

|

Mr Charalambos Meivatzis | Partner | View Profile |

|

Mrs Andri Michael | Partner | View Profile |

|

Ms Savvina Miltiadou | Senior Associate Lawyer | View Profile |

|

Mrs Syma Parthenidou | Associate Lawyer | View Profile |

|

Ms Maria Pavlou | Senior Associate Lawyer | View Profile |

|

Mrs Natalie Petrides | Partner | View Profile |

|

Mrs Yiolanda Rotsides | Counsel | View Profile |

|

Ms Chrysanthi Siantani | Associate Lawyer | View Profile |

|

Mr Andreas Siapanis | Partner | View Profile |

|

Ms Nikoletta Vanezou | Senior Associate Lawyer | View Profile |

Staff Figures

Number of lawyers : 17Languages

Greek English French Hungarian Romanian Russian German UkrainianMemberships

Cyprus Bar Association International Bar Association (IBA) International Tax Planning Association (ITPA) Society of Trust and Estate Practitioners (STEP) Cambridge Commonwealth Trust Cyprus Investment Funds Association (CIFA) International Trademark Association (INTA) Commercial Law Group (CLG) Cyprus Chamber of Commerce & Industry US-Ukraine Business Council (USUBC) International Fiscal Association C.B.T. Cyprus Blockchain Technologies Great Britain - Cyprus Business Association CGBA - Cyprus German Business AssociationOther

Contact : Christos P KinanisPress Releases

The Digital Value Group

12th April 2024 It is with great pleasure that Kinanis LLC, a forward-looking law firm, and VFTee, a boutique technology firm, introduce The Digital Value Group (TDVG) Ltd. TDVG is a dynamic new entity offering tailored IT advisory, technology solutions and application development services.Legal Developments

Immigration permit for Investors The Cyprus Permanent Residency Permit

28th March 2024 HISTORY Due to the fact that Cyprus is part of the EU and is very strategically located at the crossroads of 3 continents,The Management and Control Test Taxation of Cyprus and Foreign Companies

27th March 2024I. INTRODUCTION

In this publication, we shall examine the notion of “management and control” οf companies as this is applicable in Cyprus and how it affects the taxation of Cyprus and Overseas companies.II. THE LAW

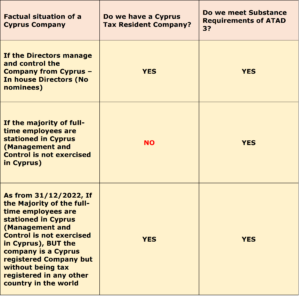

Basis of Taxation A company or an individual are taxed in Cyprus, if they are residents of Cyprus, subject to specific exceptions[1]. The residency requirement as the basis of taxation, is provided in article 5(1) of the Income Tax Law, No. 118(I) of 2002 as amended, hereinafter referred to as the “Income Tax Law”. Article 5(1) of the Income Tax Law provides the following: “Subject to the provisions of this law, in the case of a person who is resident in the Republic, tax shall be charged at the rate or rates specified hereinafter for each year of an assessment upon the income accruing or arising from sources both within and outside the Republic, in respect of: …” Meaning of Resident in the Republic The meaning of “Resident in the Republic” is defined in the Income Tax Law article 2 which provides the following: “Resident in the Republic, when applied to an individual, means an individual who stays in the Republic for a period or periods exceeding in aggregate 183 days in the year of assessment and when applied to a company, means a company whose management and control is exercised in the Republic and “non-resident or resident outside the Republic” shall be construed accordingly and non-resident or resident outside the Republic shall be interpreted accordingly”. Pursuant to this provision, a company is considered to be resident of Cyprus, and in effect subject to Cyprus taxation, when its “management and control” is exercised in Cyprus. In addition to the above meaning of Resident in the Republic as to companies, as from 31.12.2022, a company, which is established or registered pursuant to any law in force in Cyprus, will by default be considered as Resident in the Republic, provided it is not tax resident in any other country. In article 2 of the Income Tax Law, the proviso of the definition of the meaning of “Resident in the Republic”, provides the following: “It is provided that, a company which has been established or registered pursuant to any law in force in the Republic, of which its management and control is exercised outside the Republic, it is considered that it is resident in the Republic, unless the said company is tax resident in any other country”. This provision is applicable as from 31.12.2022, identified as the incorporation rule for taxation purposes. Meaning of Company The Income Tax Law, in article 2, identifies the notion of company to be “any legal body registered either in Cyprus or abroad”. Taxation of Companies All companies, anywhere registered, being residents of Cyprus are taxed on their worldwide income, accrued or arising from sources in Cyprus and/or abroad. As per the above provisions of the Income Tax Law, a company:- If it is incorporated in Cyprus, it is resident of Cyprus, the incorporation rule applies and it is subject to Cyprus taxation;

- If it is incorporated in Cyprus with management and control outside Cyprus, as from 3.12.2022, it is resident of Cyprus, unless it is tax resident in any other country[2];

- If it is incorporated outside Cyprus but its management and control is in Cyprus, then it is resident of Cyprus, subject to Cyprus taxation.

III. DEFINITION OF MANAGEMENT AND CONTROL IN CYPRUS – LACK OF STATUTORY OR JUDICIARY INTERPRETATION

There is no definition in the Income Tax Law or in any other enactment as to the meaning of the notion of “management and control” which will identify whether a company is resident of Cyprus or not. There is no definition in the law, stating who exercises management and control and how it should be exercised. There is also, no definition in the law as to what particular acts substantiate the management and control. Having in mind this interpretation gap as to the meaning of management and control in the Cyprus legislation, we should request assistance from any court judgements in place interpreting this notion. Unfortunately, though there are no Cyprus court cases interpreting the notion of management and control. The only one court case which touched the notion not directly but indirectly, without giving any interpretation, is, Lanitis Bros Ltd., v. The Central Bank of Cyprus 27/06/1974 – case No. 74/74 which is a recourse case and adopted the notion of management and control as this was adopted in the most known UK court case on the subject, namely, De Beers Consolidated Mines Ltd. v. Howe (1906) A.C., 455. In the Lanitis court case above, J. Loizou, confirmed the following: “…….. a company's residence is where it really keeps house and does its business, ... where the central management and control is exercised, as laid down in the De Beers Consolidated Mines Ltd. v. Howe (1906) A.C., 455”. Article 29 (1) (c) of the Courts of Justice Law no. 14/60 By operation of article 29 (1) (c) of the Courts of Justice Law no. 14/60 as amended, Common Law[3] and the Principles of Equity[4], are among the sources of the Cyprus legal system, provided they do not come in conflict with local statutes. In this respect, since among the sources of the Cyprus legal system are the Common Law and the Principles of Equity, we may refer to English court cases, in the absence of Cyprus court cases, in order to interpret the meaning of management and control. IV. INTERPRETATION OF MANAGEMENT AND CONTROL NOTION BASED ON UK COURT JUDGEMENTS The management and control test to identify the residency of a company was applicable in the UK until 1988 for UK registered companies. In 1988, it was replaced by relevant statutory provision, (Finance Act 1988), and now all UK registered companies are by default treated as residents of UK, taxable in UK, irrespectively of their place of management, unless they can show that their place of effective management is in a country with which UK has relevant double tax treaty[5]. In such a case, where possible dual residency of companies may be in place, the so called “Tie – breaker” article of the OECD model treaty as to effective management, usually included in all double tax treaties signed among the countries, apply and controls the residency of a company. The management and control test, which is the Common Law test of corporate residence, irrespectively of the above statutory provision which applies by default to all UK companies, is according to the UK law, applicable to non-UK companies i.e., foreign registered companies. Under these Common Law provisions, a foreign company i.e., Cyprus, BVI etc., might be taxable in the UK if their management and control is exercised in the UK. This corporate residency test is a fundamental concept of international corporate taxation and is the tool of income tax authorities to impose taxation on foreign companies for their activities undertaken abroad BUT managed and controlled onshore. In view of the provisions of the UK law as above indicated, there is a considerable number of court decisions which deal with the interpretation of the management and control test and from which we are getting guidance as to how this test will be applicable in Cyprus, if a case arise and interpretation of this term will be required by the Cyprus authorities and courts. In this respect, since among the sources of the Cyprus legal system are the Common Law and the Principles of Equity, our courts and the Commissioner of Income Tax, is expected to follow the principles laid down by UK court cases in interpreting the notion of management and control, which court cases, will give the guidance to Cyprus authorities in the interpretation of this notion.V. TO WHAT THE MANAGEMENT AND CONTROL OF A COMPANY REFERS TO?

The management and control notion refers to the management and control of the strategic decisions related to the business of the company. Management and control is not:- The exercise of powers vested in the shareholders in general meeting (for example, the appointment of directors, the amendment of the Articles, the winding up of the company or the increase or reduction of the share capital);

- The day-to-day administration of a company’s business (since this is the implementation of the policy and decisions of those who ultimately manage and control the company) – this generally has a more administrative flavour; or

- The management and control notion was first used as the main factor in determining a company’s residence in the cases of Calcutta Jute Mills Co Ltd v Nicholson andCesena Sulphur Co Ltd v Nicholson (1876) LR 1 Exch D 428, which were heard and decided together by the Court of Exchequer.

- The ‘control’ test was affirmed by the House of Lords in De Beers Consolidated Mines Ltd v Howe[1906] AC 455, 5 TC 198. There the company was incorporated in South Africa and the whole of its profits were made from mining and disposal of diamonds. The head office of the company was at Kimberley in the Cape of Good Hope, where general meetings were held.

- The place at which a company’s management and control is exercised, and therefore its residence, is to be determined by reference to the facts as they exist, rather than according to any requirement of the law or of the company’s regulations.

- Further, the residence of those directors will not necessarily determine the residence of the company; the directors of a company may all be UK resident but if they exercise central management and control of a company outside of the UK, the company will not be UK resident (Laerstate BV v R & C Commrs [2009] TC 00162).

VI. THE CORE ELEMENTS OF THE MANAGEMENT AND CONTROL NOTION

In the following chapters we shall deal with the interpretation of the notion of management and control and we shall try to identify its core elements. In this respect we shall examine:- Who exercises the management and control of the business of the company?

- In which place a company is considered as resident according to the management and control test?

- Which are the substance requirements that connect the exercise of the management and control with a particular place?

- How the management and control must be exercised in order for a company to be considered as resident in the place where the management and control is exercised?

VII. ANALYSIS OF THE CORE ELEMENTS OF THE MANAGEMENT AND CONTROL NOTION

A. Who exercises the management and control of the business of the company?

The question in effect is, which company body has been entrusted with the power to decide the fundamental policies and the key strategic decisions as to the business of the company? The board of Directors? The shareholders? Third persons? Who? The distribution of powers between the general meeting of shareholders and the board of directors as per the Companies’ Law Cap 113, is left to the Articles of Association which in practice confer extensive powers on the directors. The Articles of Association generally follow Table A of the Companies’ Law Cap 113 as to the distribution of powers. Table A, in section 80, provides that the business of the company shall be managed by the directors, subject to any special provisions of the Articles of Association of the company or the law. Section 80 provides the following: Powers and Duties of Directors- The business of the company shall be managed by the directors, who may pay all expenses incurred in promoting and registering the company, and may exercise all such powers of the company as are not, by the Law or by these regulations, required to be exercised by the company in general meeting, subject, nevertheless, to any of these regulations, to the provisions of the Law and to such regulations, being not inconsistent with the aforesaid regulations or provisions, as may be prescribed by the company in general meeting but no regulation made by the company in general meeting shall invalidate any prior act of the directors which would have been valid if that regulation had not been made.

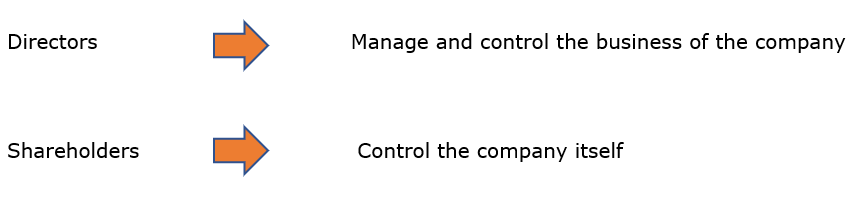

As already discussed, the control that we are discussing in this publication, is that which relates to the highest level of management of the company’s business related to its strategic decisions and must not be confused with the control which vests in the company’s shareholders.

In this respect, the management and control of the business of the company, by default is exercised by the directors, (section 80 of Table A) and not by the shareholders who control the company itself.

Superiority of decisions taken by the board of directors

The distribution of powers among the board of directors and the shareholders is such that any decision taken by the board of directors in respect of management matters as to the business of the company cannot be overruled by the shareholders in general meeting.

A case illustrating the significance of the Articles of Association as regards the division of powers between the board of directors and the general meeting of shareholders is that of Automatic Self – Cleansing Filter Syndicate Company v Cunninghame [1906] 2 Ch. 34, where the court of Appeal supported and upheld the directors’ refusal to carry out a sale of corporate property in defiance of simple resolution passed in general meeting which purported to authorise the sale. Such power was reserved by the Articles to the directors and the shareholders could not intervene.

In effect, the powers delegated to the board of directors cannot be exercised by the shareholders in General meeting.

Additional relevant authority supporting this separation of powers is Breckland Group Holdings v London Suffolk Properties [1989] BCLC 100, where the 51% shareholders instructed their lawyers to file a court case on behalf of the company. The court held that such power was left with the board of directors as per the Articles and the majority shareholders were effectively precluded from initiating such an action on behalf of the company. In this respect, the company was not obliged to pay the lawyers’ fees.

Also, in the case John Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113, the board of directors decided to institute court proceedings for a debt owed to the company. Subsequently, the shareholders by a relevant resolution purported to discontinue the case. It was held that the decision of the board of directors it could not be overruled by the shareholders’ resolution which was invalid.

In the case Stanley v Gramophone and Typewriter Ltd (1908) 5 TC 358 the general position that the directors are not the servants or agents of the shareholders to obey their orders was emphatically stated.

The facts

The appellant company (resident in England) held all of the shares in a German company. The appellant company was assessed on the monies retained by the German company, and the case depended on whether the unremitted funds considered as the gains of a business ‘carried on’ by the English company as opposed to a separate entity.

The Issue

Whether the appellant company was liable under the Income Tax Act, 1853?

Held

The Court of Appeal held that the fact that the appellant company owned shares in a German company was not enough to make the business of that German company the business of the appellant company (resident in England). Thus, the appellant company did not bear liability under the Income Tax Act, 1853. The court further held that the directors are not the servants of the shareholders. They shall not obey shareholders’ directions. They are not the agents of shareholders.

In this case it was accepted that the management and control of the business of the company, was exercised by its own directors from the place where they met and decided the matters of the company, and not by the board of directors of its parent company.

The fact that the shareholders through their voting rights can remove the directors from their office does not affect the above principle. The business of the company will still be managed and controlled by its board of directors.

It is clear from the cases so far that the shareholders cannot interfere with the directors’ discretion and cannot instruct the directors how to exercise their discretionary functions.

Pawers of shareholders

The Companies’ Law, Cap 113, reserves certain powers to the general meeting of shareholders such as the alteration/amendment of the Memorandum and Articles of Association, an increase or reduction of the share capital, the removal of the directors from their office and the voluntary winding up of the company, actions which are relate to the control of the Company but not related to the decision making process as to the business of the company and do not affect the management and control notion related to the business of the company.

Important note as to articles of association

Despite the above general principle, there are though in some cases, specifically drafted Articles of Associations which deprive the directors of the management and control of the business of the company or give them limited authorities subject to the approval of the shareholders. This is a serious qualification moving the central management and control of the business from the directors to the shareholders and each case must be carefully examined.

If such serious step is taken, the company might be considered as resident at the place of meetings and decision-making process of the shareholders as the management and control of the business is exercised by them.

Shadow Directors

In addition, once the appointed directors follow blindly the instructions of third persons, such as auditors or lawyers or other consultants, again, it might be considered that the management and control of the business of the company is exercised by these third persons and not by the appointed directors. Again, there might be a serious risk the residency of the company to move to the place of the residence of the instructing person. In such a case the shadow director notion comes into play as this is provided in art. 192(9) of the Companies’ law, Cap 113. The instructing persons are considered as shadow directors and are the actual persons who manage and control the business of the company.

In conclusion, the answer to the question, who exercises the management and control of the business of the company by default, pursuant to section 80 of Table A of Companies, Law Cap 113, this is the board of directors, subject to any specific provisions of the Articles of Association or the presence of any shadow directors.

As already discussed, the control that we are discussing in this publication, is that which relates to the highest level of management of the company’s business related to its strategic decisions and must not be confused with the control which vests in the company’s shareholders.

In this respect, the management and control of the business of the company, by default is exercised by the directors, (section 80 of Table A) and not by the shareholders who control the company itself.

Superiority of decisions taken by the board of directors

The distribution of powers among the board of directors and the shareholders is such that any decision taken by the board of directors in respect of management matters as to the business of the company cannot be overruled by the shareholders in general meeting.

A case illustrating the significance of the Articles of Association as regards the division of powers between the board of directors and the general meeting of shareholders is that of Automatic Self – Cleansing Filter Syndicate Company v Cunninghame [1906] 2 Ch. 34, where the court of Appeal supported and upheld the directors’ refusal to carry out a sale of corporate property in defiance of simple resolution passed in general meeting which purported to authorise the sale. Such power was reserved by the Articles to the directors and the shareholders could not intervene.

In effect, the powers delegated to the board of directors cannot be exercised by the shareholders in General meeting.

Additional relevant authority supporting this separation of powers is Breckland Group Holdings v London Suffolk Properties [1989] BCLC 100, where the 51% shareholders instructed their lawyers to file a court case on behalf of the company. The court held that such power was left with the board of directors as per the Articles and the majority shareholders were effectively precluded from initiating such an action on behalf of the company. In this respect, the company was not obliged to pay the lawyers’ fees.

Also, in the case John Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113, the board of directors decided to institute court proceedings for a debt owed to the company. Subsequently, the shareholders by a relevant resolution purported to discontinue the case. It was held that the decision of the board of directors it could not be overruled by the shareholders’ resolution which was invalid.

In the case Stanley v Gramophone and Typewriter Ltd (1908) 5 TC 358 the general position that the directors are not the servants or agents of the shareholders to obey their orders was emphatically stated.

The facts

The appellant company (resident in England) held all of the shares in a German company. The appellant company was assessed on the monies retained by the German company, and the case depended on whether the unremitted funds considered as the gains of a business ‘carried on’ by the English company as opposed to a separate entity.

The Issue

Whether the appellant company was liable under the Income Tax Act, 1853?

Held

The Court of Appeal held that the fact that the appellant company owned shares in a German company was not enough to make the business of that German company the business of the appellant company (resident in England). Thus, the appellant company did not bear liability under the Income Tax Act, 1853. The court further held that the directors are not the servants of the shareholders. They shall not obey shareholders’ directions. They are not the agents of shareholders.

In this case it was accepted that the management and control of the business of the company, was exercised by its own directors from the place where they met and decided the matters of the company, and not by the board of directors of its parent company.

The fact that the shareholders through their voting rights can remove the directors from their office does not affect the above principle. The business of the company will still be managed and controlled by its board of directors.

It is clear from the cases so far that the shareholders cannot interfere with the directors’ discretion and cannot instruct the directors how to exercise their discretionary functions.

Pawers of shareholders

The Companies’ Law, Cap 113, reserves certain powers to the general meeting of shareholders such as the alteration/amendment of the Memorandum and Articles of Association, an increase or reduction of the share capital, the removal of the directors from their office and the voluntary winding up of the company, actions which are relate to the control of the Company but not related to the decision making process as to the business of the company and do not affect the management and control notion related to the business of the company.

Important note as to articles of association

Despite the above general principle, there are though in some cases, specifically drafted Articles of Associations which deprive the directors of the management and control of the business of the company or give them limited authorities subject to the approval of the shareholders. This is a serious qualification moving the central management and control of the business from the directors to the shareholders and each case must be carefully examined.

If such serious step is taken, the company might be considered as resident at the place of meetings and decision-making process of the shareholders as the management and control of the business is exercised by them.

Shadow Directors

In addition, once the appointed directors follow blindly the instructions of third persons, such as auditors or lawyers or other consultants, again, it might be considered that the management and control of the business of the company is exercised by these third persons and not by the appointed directors. Again, there might be a serious risk the residency of the company to move to the place of the residence of the instructing person. In such a case the shadow director notion comes into play as this is provided in art. 192(9) of the Companies’ law, Cap 113. The instructing persons are considered as shadow directors and are the actual persons who manage and control the business of the company.

In conclusion, the answer to the question, who exercises the management and control of the business of the company by default, pursuant to section 80 of Table A of Companies, Law Cap 113, this is the board of directors, subject to any specific provisions of the Articles of Association or the presence of any shadow directors.

B. In which place a company is considered as resident according to the management and control test?

Place of management and control- The leading case on company residency is De Beers Consolidated Mines Ltd v Howe [1906] AC 455, 5 TC 198. In this case it was established that a company resides, there where its real business is carried out. In the same case it was decided that the real business of a company is carried out, not there where the trading operations are taking place, but where the central management and control of its business actually takes place, as said in the judgement, “there where the central management and control actually abides”.

- Loizou, confirmed the following:

- Important is also the Court of Appeal case in Bullock v Unit Construction Co Ltd (1959) 38 TC 712 at 729 – 730 also at, [1960] AC 351.

- The same principle has been reconfirmed in R v Dimsey (1999) STC 846, where the court emphasised that the central management and control test is a composite test designed to identify where the decisions of fundamental policy are made as opposed to the place where the day - to - day profit earning activities are undertaken.

- In addition, inTrevor Smallwood Trust v HMRC [2010] EWCA Civ 778, the Court of Appeal confirmed that a Mauritian trust that has been arranged and orchestrated in the UK was ultimately controlled and managed in the UK.

C. Which are the substance requirements that connect the exercise of the central management and control with a particular place?

The question as to which are the substance requirements that connect the exercise of the central management and control with a particular place is a question of fact. We need to identify the facts that connect the exercise of the central management and control with a particular place. Indicatively these are: Location of Board meetings It has been decided and stressed repeatedly in court cases that, the place where the directors meet in order to reach their strategic decisions on company’s policy, finance and related matters, subject to various qualifications which will be discussed further below, will be the place of central management and control of the company’s business. If the intention is to have a Cyprus resident company, avoiding any possible allegations that the company is resident abroad, then all board meetings should be held in Cyprus. It is best practice therefore, to avoid a moving / transit board, since that makes it harder to demonstrate clear residence in any one location and might create issues of multiple residencies. In effect, the place where the directors meet for their board meetings, deciding on strategic company’s issues such as its policy, finance and related fundamental matters, is the location of the central management and control of the company’s business and consequently once the other factors are in place, the company is resident at that location. Art. 191A of the Companies Law Cap 113 As to this issue, it is worth noting the provisions of Art. 191A of the Companies Law Cap 113, which provides the following: “Participation in the directors meeting by electronic means 191A. Unless expressly provided for in the company's articles of association, a meeting of the directors may be held by telephone or by any other means by which persons participating in it can simultaneously listen and be heard by all the other persons participating in it and the persons participating by in this way, for the purposes of establishing a quorum and for any other purpose, and the people participating in this way are counted as present at the board meeting: Provided that, in the above case, the meeting of the directors is considered to have taken place where the person who kept the minutes of the relevant meeting of the directors is located”. In effect, in case the board meetings are held through electronic means such as the Zoom platform, once the directors are located in various jurisdictions, the place of the meeting is considered to be the place of the person who kept the minutes of the relevant meeting of the directors. In such a case the decision is considered as taken in the place where the minutes are kept. Directors’ permanent residence The residence of the directors is closely connected to the place where the board meetings are held. If the intention is to have a Cyprus tax resident company, the directors or at least the majority of them must be permanent residents of Cyprus. In this way, it is easily proved that the board meetings are taking place in Cyprus and the management and control is exercised in Cyprus. Appointment of directors residing outside Cyprus If a Cyprus company resident is desired, the appointment of directors residing outside Cyprus, although possible, must be avoided. In case it is impossible to avoid such appointment, then the law of the country of residence of the foreign director to be appointed, must be very carefully examined to avoid adverse possible tax effects. There are countries which apply the management and control test in a similar manner that Cyprus does, i.e., UK, and in implementing this test, they might consider that, if a foreign company (i.e., Cyprus) is managed by a director who resides in their jurisdiction, becomes their tax resident of UK and impose or claim taxation from the company concerned. The fact that as from 31.12.2022 such a Cyprus company, from Cyprus law perspective, will be considered resident of Cyprus unless it is tax resident in another country, does not save the situation. The foreign country might claim that the company is resident in its jurisdiction and impose taxation, despite the implication of the Cyprus law. In such a case we may have dual residency issues which will be explained further below under chapter, “IX. Double Tax Treaties – Their impact on the residency issue of Cyprus Companies”. Appointing directors residing in countries in which the management and control test for foreign companies is applicable, such as the UK as explained above, must be avoided. There are considerable risks which need not be taken. Appointment of directors residing in the place where the income of the company is generated It is also advisable to avoid appointing directors who reside in the foreign country where the income of the Cyprus resident company is expected to arise or in which country tax issues might be raised as to the taxation of the Cyprus company or as to the taxation of its beneficial shareholder. If for example, the activities of the company are in Romania and the income is generated in or from Romania, it seems not proper to appoint as directors of the Cyprus resident company, persons residing, living and working in Romania. In case of such appointments, one leaves room for arguments, that the company or its real beneficial shareholder are taxable in Romania, as the effective management of the company is situated in Romania. Also, an argument which can be put forward is that the company is not resident of Cyprus as its management and control might be alleged not to be exercised in Cyprus. Again, in such cases, there is possibility for dual residency issues as discussed in chapter “IX. Double Tax Treaties – Their impact on the residency issue of Cyprus Companies of this brochure”. We would like to clarify though, that the crucial issue is not the nationality of the director but his / her residency, where he / she permanently resides. A foreign national permanently residing in Cyprus, being a resident of Cyprus, will be a suitable director. Appointment of directors residing in Cyprus, as directors in foreign / overseas companies The same factors that will strengthen the position of a Cyprus company to be considered as managed and controlled in Cyprus, will be also considered to examine whether a foreign / overseas registered company is managed and controlled from Cyprus. In this respect, it is not advisable to appoint directors residing in Cyprus as directors in companies registered in tax haven countries like BVI, Panama, Bahamas, Nevis, Cayman Islands, etc. In such a case, there might be a real risk that these companies may be considered to be managed and controlled in Cyprus, and consequently taxable in Cyprus, as a consequence of the applicability of the management and control test. If such a claim is put forward by the Inland Revenue, BVI, Panama, Bahamas, Nevis, Cayman Islands, etc., companies, in order to avoid taxation in Cyprus, will need to prove that the Cypriot director acts only on instructions of the real owners or other advisors situated abroad transferring the management and control abroad, there where the shareholders or other advisors, reside. In effect, the director who follows blindly the instructions of the shareholders, or other advisors, is a mere cipher, simply stamping documents and doing what he is told, not managing and controlling the company. Relevant evidence and confidential information will need to be disclosed to the Inland Revenue to prove the director’s symbolic status. Risk of permanent settlement in Cyprus What must be noted in this case is that the director appointed to the foreign company, being resident of Cyprus, does not have authorization to enter into contracts in the name of the company, because this company can be considered to have a permanent establishment in Cyprus in relation to any activities that this person undertakes for the business with the result that these activities are also taxable in Cyprus. There is no need though to be engaged in such complications since the possibility can easily be avoided with the appointment of directors not residing in a country which applies the management and control principle. Frequency of Board meetings Board meetings should be sufficiently frequent to enable the directors to exercise control over the strategic affairs of the company. Depending on the level of activity in the company, a minimum of six board meetings in each year with each board meeting taking no more than two months after the last one. Administrative Office A fully fletched office must be established in Cyprus where the actual management and control of the company’s business will be exercised. In this office, the fundamental policy and management decisions must take place, and the properly recorded board minutes must be kept. The company secretary should be resident of Cyprus and accounting records, corporate records and other significant original documents should be maintained. Employees Employees must be employed and paid reasonable salaries according to market levels. Stationery Stationery must be printed with the letterheads of the company and its office address and other contact details such as telephone, fax numbers, email address and website. Bank accounts Bank accounts must be opened also in Cyprus and managed by the local directors or employees. Accounting records Maintenance of accounting records should be in Cyprus. In conclusion, as to the factors which will support the argument that the management and control is exercised in Cyprus in order to have a resident company in a particular place, the directors must meet, manage and control the affairs of the company in Cyprus, proper board meetings with minutes must be taken place in Cyprus, all or at least the majority of the directors to be permanent residents of Cyprus and the positive surrounding factual circumstances to be present in Cyprus and avoid the negative surrounding factual circumstances as explained above. The provisions of Art. 191A discussed above must be born in mind. Any appointments in a Cyprus company of directors not residents of Cyprus, raise serious risks as the company might be considered as resident in another jurisdiction with adverse tax consequences. The provision of the law that such company without being officially tax resident in another jurisdiction, as from 31.12.2022 will be considered as tax resident of Cyprus, does not save the situation. The foreign jurisdiction where the directors reside and decide, might claim the residency for such company and claim to impose taxation for its activities. The appointment of Cypriot resident directors in foreign companies, should be avoided because the company may be considered to be managed and controlled from Cyprus and in effect resident in Cyprus with adverse tax consequences.D. How the management and control must be exercised in order for a company to be considered as resident in the place where the management and control is exercised?

This is the most crucial and most important criterion in order for a company to be considered as resident in the place where the management and control is exercised.- Real exercise of management and control by the board of directors - Decision process – effective consideration and knowledge of the facts

-

- The acquisition or disposal of assets;

- Capital expenditure;

- Budgets approval;

- Operational decisions;

- Financial decisions such as granting or receiving loans;

- Decisions on the engagement or dismissal of directors and other senior personnel;

- Concluding and execution of contracts;

- Mergers and acquisitions;

- Expanding or changing the line of business;

- Appointment of consultants; and,

- Nominating accountants and auditors.

-

- The time and place of the meeting and who was present;

- What was resolved and the reasons for such resolution should be recorded in as much detail as possible. Discussions in board meetings should be recorded in detail. Any views or debates or agreements or disagreements are important to be recorded in detail as these are important evidence that the directors applied their minds to the relevant questions. Establishing a pattern of decision making is also important. The key point is that these minutes are likely to be more comprehensive than is perhaps the norm.

-

- The provisions of Art. 191A discussed above must be born always in mind.

- Wood v Holden, 2005 BTC 253 - High Court 18.4.2005

- Laerstate BV v HMRC [2009] UKFTT 209

- HMRC v Development Securities plc and others [2020] EWCA Civ 1705

-

- Decisions by subsidiaries should be taken at proper board meetings and that,

- Such board meetings properly consider the merits of any decisions to be taken as well as the legality of those steps. Particular care should be taken that, in implementing proposals given by a parent company, directors do not treat such proposals as instructions and that they consider carefully the commercial context for the decision.

VIII. TAX RESIDENCY OF CYPRUS COMPANIES AND SUBSTANCE REQUIREMENTS UNDER THE PROPOSED THIRD ANTI-TAX AVOIDANCE DIRECTIVE, KNOWN AS “ATAD 3”

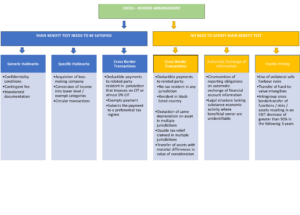

The European Commission on the 22nd of December 2021 published a legislative proposal for a Directive to be issued, named, the Third Anti-Tax Avoidance Directive, known as “ATAD 3”, which sets forth rules to prevent the misuse of shell companies for tax purposes. The Proposed Directive should have been adopted early 2022 by the European Union Council and be implemented by the Member States by the 30th of June 2023 at the latest. The provisions should subsequently be effective in all Member States as from the 1st of January 2024. The Directive lays down a uniform test that will help Member States to identify undertakings that are engaged in an economic activity, but which do not have minimal substance and are misused for the purpose of obtaining tax advantages. Once these minimum substance requirements are not met, the undertaking will be classified as “shell entity” and will sustain certain adverse tax consequences. In order to examine if an entity meets the minimum substance requirements, so that not to be characterised as “shell entity”, the following information must be provided:-

- Whether the entity has an office space, (owned or rented), through which it exercises its activities;

- Whether the entity has an active EU bank account; and

- Whether at least one of its directors is an in-house director properly qualified to handle the business of the undertaking or the majority of its full - time employees reside in the same country as the undertaking.

- the principle of management and control which will identify whether a company is resident of Cyprus, being a principle related to the directors’ and third persons powers to decide the policy issues and business of the company, and

- the substance requirements as per ATAD 3 which substance requirements will identify whether the company is a shell one or not.

IX. DOUBLE TAX TREATIES – THEIR IMPACT ON THE RESIDENCY ISSUE OF CYPRUS COMPANIES

Cyprus has signed a considerable number of Double Tax Treaties which regulate taxation on various matters between the contracting states. In order for a company to take advantage of the provisions of the Double Tax Treaties, it must be resident of one of the two contracting states. In our case, the Cyprus company, must be resident of Cyprus for tax purposes. A definition of what a “resident of a Contracting State” means, is given in article 4.1 of the Organisation for Economic Co-operation and Development - OECD, model treaty which provides the following: “RESIDENT For the purposes of this Convention, the term "resident of a Contracting State" means any person who, under the laws of that State, is liable to tax therein by reason of his domicile, residence, place of management or any other criterion of a similar nature, and also includes that State and any political subdivision or local authority thereof. This term, however, does not include any person who is liable to tax in that State in respect only of income from sources in that State or capital situated therein”. Further, according to the Commentary to the OECD Model Tax Convention: “The place of effective management is the place where the key management and commercial decisions that are necessary for the conduct of the entity's business are in substance made. To determine the tax residency of a company, tax authorities would be expected to take into account various factors, including among others where the chief executive officer and other senior executives usually carry on their activities and where the senior day-to-day management of the person is carried on.” Place of effective management as per relevant article in Double Tax Treaties. Tie – breaker article Article 4.3 of the OECD model treaty, provides the following: “Where by reason of the provisions of paragraph 4.1, cited above, a person other than an individual is a resident of both Contracting States then it shall be deemed to be a resident only of the State in which its place of effective management is situated”. The above crucial provision, known as the “Tie – breaker article”, which provides the solution to a possible problem of dual residency, is included nearly in all treaties that Cyprus has signed. Definitions of the terms in the Double Tax Treaties There is no definition of the terms, place of management, effective management, head office, registered office, place of registration, headquarters, place of incorporation, or other similar criteria which are used in the Double Tax Treaties. Applicability of local laws as to residency The lack of any definition of the above terms used in respect of all legal bodies in the Double Tax Treaties, leads to the consideration of the laws of contracting States, Cyprus law in our case, in order to establish the residency of a Cyprus company, under such law, for tax purposes and consequently for treaty purposes as well. In effect, the treaties point to the local laws of the contracting States, in order to identify, under which conditions a company registered in their jurisdiction, or not registered there, will be considered as their tax resident. Local tax law provisions will need to be examined in order for a company to be considered as tax resident under the provisions of the Double Tax Treaties. In considering whether a Cyprus company is a resident of Cyprus, and consequently being benefited from the provisions of the Double Tax Treaties, the analysis provided in the previous chapters of this brochure as to the management and control test, applies. Dual residency There might be a situation where a company is a resident of more than one country. This might be the case when the management and control of the affairs of the company is not centred in one country but is divided or distributed among one, two or more countries. Such situations might appear when the directors of the company, which form the highest level of management of the company, are resident in various countries and execute their management duties from their place of residence and not from only one country. Also, such situations might appear when the advisors or the shareholders of the company reside in different countries than where the board meets and from their place of residence direct the decisions of the board. If such factual situations exist, then the allegation and possibility of dual residency of a company can be raised by Inland Revenues with drastic tax effects. It is for this reason that we are of the opinion that if a Cyprus tax resident company is needed, the appointment of directors with effective management, residing outside Cyprus must be avoided, as dual residency issues may arise. The above possibilities as to the dual residency of a company have been considered in many court cases[8]. The authorities clarify and confirm that there where there is a fragmentation of the management and control of the business of the company exercised in effect from two or more countries, there can be dual residency for the company with further tax issues to be considered. Allegation of dual residency by a treaty country If dual residency exists or if such allegation is raised by any one of the treaty States, e.g., that a Cyprus company is also resident in that other State which claims taxation, then the solution is provided by the “tie – breaker” article of the Double Tax Treaties, article 4.3 discussed above. According to article 4.3, if dual residency exists, the company is deemed to be resident where its effective management is exercised. The answer to the question, where the effective management is exercised, identifies the tax residency of the company and in effect the country of its taxation. As to the effective management test and its conditions, the analysis provided in the previous chapters of this brochure relating to the management and control test, apply accordingly. In the court case, Wensleydale’s Settlement Trustees v IRC [1996] STC (SCD) 241, a Special Commissioner considered that the place of effective management is there where the shots are called, implying realistic positive management. In effect, the analysis of the management and control test provided above applies for this issue too. Case study Suppose that the Russian or the UK tax authorities or the Inland Revenue of any other treaty country, allege that a resident Cyprus company, for matters of management, domicile or other similar issues, is also resident of Russia or UK or in that other country and not only in Cyprus. Because of this conclusion, they seek to impose taxation on the Cyprus resident company for a particular operation. In case of such a dual residency problem, (Cyprus also alleges that the company is a resident of Cyprus liable to taxation in Cyprus) article 4.3 of the Double Taxation Treaty signed between Cyprus and Russia, and the relevant article of the UK treaty or as the case might be with the other treaty countries, applies and gives the solution. This tie – breaker article, as being a provision of an international treaty, supersedes any local laws and directs that the residency of the company is deemed to be there where the effective management of the company is exercised. If the effective management is exercised in Cyprus, taxation cannot be imposed in Russia or in the UK or in the other contracting State by operation of the Double Taxation Treaty. In view of this provision which provides a solution, special attention must be paid to what has been said above in order to establish and to secure that the management and control of the company’s affairs is exercised in Cyprus. Similar arguments can be put forward in all other cases where Double Tax Treaties have been signed with the above provision in place. The judgement in Wood v Holden mentioned above, handles also the issue as to the effective management test, due to the fact that a relevant provision is in the Double Taxation Treaty between UK and Holland and the case was decided on this principle. It was decided that the effective management was situated in Holland and not in the UK. In more recent court cases though, it was decided that the effective management was situated in UK and not overseas where the companies were registered and the board of directors was situated. See, HMRC v Development Securities plc and others [2020] EWCA Civ 1705 and Laerstate BV v HMRC [2009] UKFTT 209 and Laerstate BV v HMRC [2009] UKFTT 209, discussed above.X. THE CYPRUS INLAND REVENUE APPROACH IN IMPLEMENTING THE NOTION OF MANAGEMENT AND CONTROL

The Cyprus Inland Revenue has not yet issued any practice guidelines as to how it will deal with the management and control test, its interpretation and implementation.- Cyprus companies under investigation by Cyprus Inland Revenue

- Foreign registered Companies under investigation by Cyprus Inland Revenue

-

- The directors of that foreign company exercise management and control in Cyprus; or

- Someone other than the appointed directors, such as consultants, shareholders, or third parties, acting in effect as shadow directors, exercise management and control from within Cyprus over the business of the foreign company; or

- It has a permanent establishment in Cyprus.

- Cyprus companies under investigation by foreign Inland Revenue departments

XI. THE MANAGEMENT AND CONTROL TEST IN ONE PAGE

What has been discussed in this publication is summarized below in the following diagram:| Cyprus Registered Company | Irrespective of place of Management and Control as from 31/12/2022 | Resident of Cyprus |

| Cyprus Company | Management and Control outside Cyprus – Tax resident in another country | NOT Tax Resident of Cyprus | ||

| Overseas Company | Management and Control outside Cyprus | NOT Resident of Cyprus |

| Overseas Company | Management and Control in Cyprus | Resident of Cyprus |

| Cyprus Company or Overseas Company | Management and Control not centred in one country. Dual Residency DTT-Double Tax Treaty in place | Resident there where the effective management is exercised - “tie-breaker” provision of DTT |

| Cyprus Company or Overseas Company | Management and Control not centred in one country. Dual Residency. NO Double Tax Treaty in place | Resident as per local laws of each country the management and control is exercised |

- If it is incorporated in Cyprus, it is resident of Cyprus, the incorporation rule applies, and it is subject to Cyprus taxation;

- If it is incorporated in Cyprus with management and control outside Cyprus, it is still resident of Cyprus unless it is tax resident in any other country;

- If it is incorporated outside Cyprus but its management and control is in Cyprus, then it is resident of Cyprus, subject to Cyprus taxation.

- The management and control is exercised in Cyprus, if the board of directors resides or at least the majority resides in Cyprus and genuinely holds board meetings in Cyprus having in mind all the positive and negative factors explained above;

- The directors, at the board meetings held in Cyprus, give genuine consideration as to the affairs and business of the company and decide its policy, structural and main issues without simply following the instructions of the owners or their advisors. The directors must apply their mind, think and decide autonomously on all issues of the company and in its best interests; Knowledge of the business of the company and the business factual situation is of paramount importance.

- Any instructions and decisions relating to the business, management matters of the company, must be generated and given solely by the board of directors.

- Dual residency issues might be raised in case of fragmentation of power, namely, the management and control of the company’s business is exercised by the directors / shareholders / advisors, in various countries. In such a case, if there is a Double Tax Treaty in place, the effective management rule “tie-breaker” article applies and identifies the residency of the company. If there is not any Double Tax Treaty in place, local laws will apply and give the solution.

XIII. DISCLAIMER

This publication has been prepared as a general guide and for information purposes only. It is not a substitution for professional advice. One must not rely on it without receiving independent advice based on the particular facts of his/her own case. No responsibility can be accepted by the authors or the publishers for any loss occasioned by acting or refraining from acting on the basis of this publication.Author: Christos Kinanis

Footnotes [1] See further below under the heading,” Taxation of Companies” at page 5, what is provided as to the taxation of non-resident companies of Cyprus. [2] The law provides … of being tax resident in any other country. There is no condition that the taxation laws of that other country impose any taxation on the income earned. So, any country, where the Cyprus company is tax resident, meets the requirement. [3] “Common Law” is the body of legal rules, based upon court decisions and not on statutory law made by a parliament, embodied in reports of decided cases, that has been administered by the common-law courts of England since the Middle Ages. Common laws vary depending on the jurisdiction, but in general, the ruling of a judge is often used as a basis for deciding future similar cases. [4] “Principles of Equity” are set of rules which rectify injustice done by the rigid application of court precedents and statutory law. It is the rectification of legal justice. [5] FA 1994 s.249. [6] The shadow director principle is also provided in Cyprus companies’ Law Cap 113, in section 192(9). [7] Re Little Olympian Each Ways Ltd [ 1994] 4 All ER 561; Untelrab Ltd v McGregor [1996] STC (SCD) 1; R v Crown Court at Kingston [2001] STC 1615; Esquire Nominees Ltd v Commissioner of Taxation [1971] 129 CLR 177; New Zealand Forest Products NV v Commissioner of Inland Revenue [1995] 17 NZTC 12,073}; Wood v Holden, 2005 BTC 253 - High Court 18.4.2005; Laerstate BV v HMRC [2009] UKFTT 209; and, HMRC v Development Securities plc and others [2020] EWCA Civ 1705. [8] Swedish Central Rly Co Ltd v. Thomson [1925] 9 TC 342; Union Corp Ltd v IRC [1952] 34 TC 207; Koitaki Para Rubber Estates Ltd v Federal Comr of Taxation [1940] 64 CLR 15; R v Holdon, High Court 18.4.2005.

LISTING ON THE CYPRUS EMERGING COMPANIES MARKET: AN UNDERESTIMATED POTENTIAL?

19th March 2024 The Emerging Companies Market (“ECM”) is a recognised unregulated market of the Cyprus Stock Exchange (“CSE”), offering the opportunity to Cyprus and international companies to list their shares or bonds.RESIDENCY OF CYPRUS COMPANIES APPLICABILITY OF THE INCORPORATION RULE AS FROM 31/12/2022

12th January 2023 As from 31/12/2022, an important development applies as to the residency of Cyprus companies and in effect their taxation under Cyprus tax laws.HEADQUARTERING AND BUSINESS RELOCATION TO CYPRUS

21st March 2022INTRODUCTION

By now everybody knows that Cyprus belongs to the EU, about our unrivalled sunny days and our strategic location. This is old news. Why bring Cyprus back on the Headquartering map? Does Cyprus have something new to offer to businesses and individuals that wish to relocate their businesses to Cyprus?The Third Anti-Tax Avoidance Directive (ATAD 3) The tombstone of shell entities

15th March 2022A. INTRODUCTION

The European Commission on the 22nd of December 2021 published a legislative proposal for a Directive to be issued, the Third Anti-Tax Avoidance Directive, known as “ATAD 3”, which sets forth rules to prevent the misuse of shell companies for tax purposes. The Directive should be adopted early 2022 by the Council and be implemented by Member States by 30 June 2023 at the latest. The provisions should subsequently be effective in all Member States from 1 January 2024. The Directive lays down a uniform test that will help Member States to identify undertakings that are engaged in an economic activity, but which do not have minimal substance and are misused for the purpose of obtaining tax advantages. Once these minimum substance requirements are not met, the undertaking will be classified as “shell entity” and will sustain certain adverse tax consequences. The methodology followed by the proposed Directive to identify shell entities There are 7 steps to be followed:- Identification of undertakings being at risk to be classified as shell companies;

- Substance reporting requirements;

- Exempted undertakings from reporting;

- Presumption of being classified as a shell entity or not, for tax purposes;

- Rebuttal of the presumption of being classified as shell entity - Exemption;

- Tax Consequences of not meeting the substance requirements;

- Exchange of information, tax audits and Penalties.

B. SUMMARY OF THE PROVISIONS OF THE PROPOSED DIRECTIVE

The proposed Directive will be applied following the above identified methodology, step by step. At first, undertakings, tax residents of member states which are engaged in economic activity, will be examined whether they meet cumulatively the following three conditions:- Whether the undertaking has passive income more than 75% of its revenues, such as interest, dividends and royalties; and

- Whether it is engaged in cross border activity; and

- Whether it outsources its management and administration to third parties.

- Whether the undertaking has an office space, (owned or rented), through which it exercises its activities;

- Whether the undertaking has an active EU bank account; and

- Whether at least one of its directors is an in-house director properly qualified to handle the business of the undertaking or the majority of its full - time employees reside in the same country as the undertaking.

THE PROVISIONS OF THE PROPOSED DIRECTIVE IN DETAIL

Definitions - Interpretation For the purposes of this Directive the following definitions shall apply: “Undertaking” means any entity engaged in an economic activity, regardless of its legal form, that is a tax resident in a Member State1; “Member State of the undertaking” means the Member State where the undertaking is resident for tax purposes2; In effect, any type of a legal body engaged in economic activity, being tax resident in a Member State, is subject to the provisions of the Directive. Cyprus Local or International Trusts, not being a legal person, and not liable as such to taxation in Cyprus, do not fall within the provisions of the Directive. Their subsidiary companies being tax residents of Cyprus might be caught by the provisions of the Directive unless exempted. “Relevant income” shall mean income falling under any of the following categories:- interest or any other income generated from financial assets, including crypto assets,

- royalties or any other income generated from intellectual or intangible property or tradable permits;

- dividends and income from the disposal of shares;

- income from financial leasing;

- income from immovable property;

- income from movable property, other than cash, shares or securities, held for private purposes and with a book value of more than one million euro;

- income from insurance, banking and other financial activities;

- income from services which the undertaking has outsourced to other associated enterprises3.

- more than 75% of the revenues accruing to the undertaking in the preceding two tax years is relevant income as relevant income is above identified;

- the undertaking is engaged in cross-border activity on any of the following grounds:

- more than 60% of the book value of the undertaking’s assets that fall within the scope of points (e) and (f) above, was located outside the Member State of the undertaking in the preceding two tax years;

- at least 60% of the undertaking’s relevant income is earned or paid out via cross-border transactions;

- in the preceding two tax years, the undertaking outsourced the administration of day-to-day operations and the decision-making on significant functions4.

- the undertaking has own premises in the Member State, or premises for its exclusive use;

- the undertaking has at least one own and active bank account in the Union;

- the undertaking meets one of the following two indicators:

- One or more directors of the undertaking:

- are resident for tax purposes in the Member State of the undertaking, or at no greater distance from that Member State insofar as such distance is compatible with the proper performance of their duties; and,