Korean tax authorities impose KRW 300 billion of withholding taxes on software license fees, looking

Bae, Kim & Lee LLC | View firm profile

- Deeming Oracle US the beneficial owner, the Tax Tribunal upheld

assessments against Oracle Korea on license fees paid to Ireland affiliate

going back to 2008. - Tax judgment is now on appeal by Oracle to the administrative

law court.

The Korean Tax Tribunal has affirmed National Tax Service (NTS) assessments

totaling some KRW 300 billion (approx. USD 260 million) against Oracle Korea,

as withholding taxes on software license fees paid to an Ireland affiliate

(Oracle Ireland), on the basis that beneficial ownership was with Oracle

Corporation (Oracle US). The NTS, in 2011 and 2015, imposed the withholding

taxes based on the Korea-US tax treaty, which calls for a 15% withholding rate

as opposed to no withholding under the Korea-Ireland tax treaty. The Tax

Tribunal has upheld the NTS assessments, citing among other things Oracle US’s

ownership of the software and control over the income, as contrasted with the

minor role of Oracle Ireland.

The Tax Tribunal ruling,

which issued in late 2016 (becoming public only this month), is now on appeal

by Oracle Korea to the Seoul Administrative Court. In the meantime it serves as

a stark caution for treaty-based tax planning among multinationals doing

business in Korea, particularly in sectors such as technology and media that often

utilize haven-incorporated licensing entities.

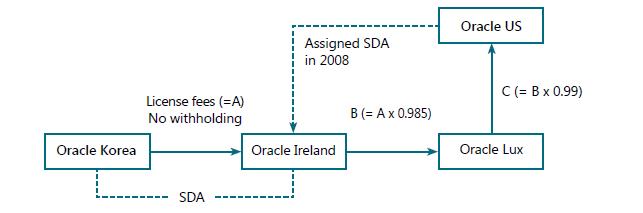

In the Oracle structure, which was

adopted in early 2008, Oracle Korea (direct subsidiary of Oracle US) licenses

the software from Oracle Ireland under a software distribution agreement (SDA);

the software is owned by Oracle US, and almost all of the fees go eventually to

Oracle US: Oracle Ireland passes 98.5%

to a Luxembourg affiliate (Oracle Lux), which passes 99% to Oracle US. Oracle

Korea applied no withholding to payments of the license fees, based on the

Korea-Ireland tax treaty. So the structure is this:

A noteworthy part of the background was that, until 2008, it had been a

straightforward arrangement of Oracle US licensing the software directly to

Oracle Korea, which withheld 15% pursuant to the Korea-US tax treaty. That is,

originally the SDA was between Oracle US and Oracle Korea, but in 2008 it was

assigned by Oracle US to Oracle Ireland.

Reviewing

the current structure in 2011 and 2015, the NTS decided it was Oracle US, not

Oracle Ireland, that was the beneficial owner of the SDA license fees. The NTS

reasoning, ratified by the Tax Tribunal, was that, in addition to owning the

software, Oracle US largely retained control of the licensing arrangement,

ending up with nearly all the fees. Oracle Ireland’s role was merely to convey

the fees to Oracle Lux, for on-payment to Oracle US.

The

result, while under review by the administrative law court, marks a significant

moment in Korean tax policy. The NTS has long leaned to an aggressive stance on

“treaty shopping”, and there have been high profile cases against financial

investment groups, for example. However, the Oracle ruling represents by far

the most striking tax levy to date in the licensing context, or against a

technology sector multinational. Facts will vary – for instance, Oracle US’s

ownership of the software is in contrast to the many arrangements where assets

are transferred to a haven vehicle. But the ruling calls broadly into question

the approach, widespread in sectors including internet and media, of

interposing licensing-purposed or administrative vehicles in jurisdictions such

as Ireland and the Netherlands.

The

ruling casts further doubt, for example, on structuring known as “double Irish

with a Dutch sandwich”, adopted by several leading US-headquartered technology

firms, which involves fees going from Korea to a set of three intermediate

entities – Irish, Dutch, Irish. (In contrast to Oracle, the assets there are

usually held by one of those entities.) Already noted and criticized in the

Korean media, the structure would face a stiff test, to say the least, under

NTS scrutiny as seen in the Oracle case. Much is at stake when the Seoul

Administrative Court arrives at its judgment, which should be within this year.

The Korean government

has gone along with the OECD’s BEPS (Base Erosion and Profit Shifting) Action

Plan to curb global tax avoidance strategies, and signaled it will pursue

review and revision of tax treaties. Meanwhile, the Oracle case serves to

epitomize the potential risk, for tax structuring, of beneficial ownership

analysis by the NTS.

* This bulletin is intended as a summary

news report only, for general information. This bulletin does not represent,

and should not be construed as, legal opinions or advice of Bae, Kim & Lee

LLC. Information contained in this bulletin is not represented to be accurate

or up-to-date. For legal advice, please inquire with Bae, Kim & Lee LLC or

other qualified counsel.

Tae Kyoon KIM

T. 82.2.3404.0574

Hakrae CHO

T. 82.2.3404.0580

Joon Yong PARK

T. 82.2.3404.0693